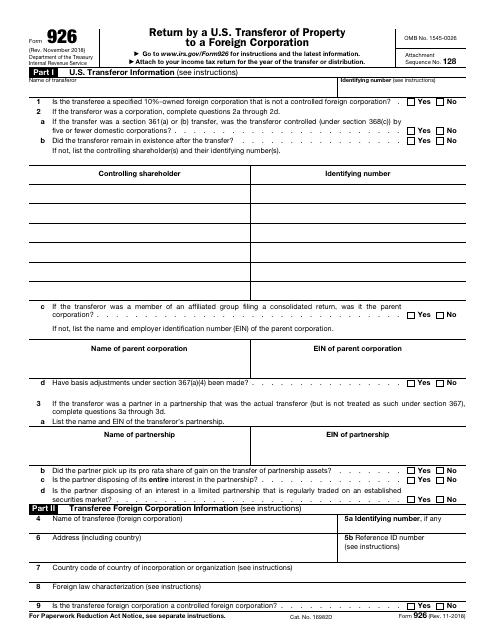

IRS Form 926 Return by a U.S. Transferor of Property to a Foreign Corporation

What Is Form 926?

IRS Form 926, Return by a U.S. Transferor of Property to a Foreign Corporation , is a document developed for U.S. citizens and residents, domestic corporations, domestic estate or trusts, who must report certain transfers of property to a foreign corporation.

The document was issued by the Internal Revenue Service (IRS) - a subdivision of the U.S. Department of the Treasury on November 1, 2018 . Download a fillable version of IRS Form 926 through the link below or browse more documents in our library of IRS Forms.

IRS Form 926 Instructions

According to the Form 926 filing requirements, individuals must file the application to report any exchanges or transfer of property to foreign corporations. The transferor must file the document with their income tax return for the tax year that includes the date of transfer.

The application consists of four parts that are presented on three pages:

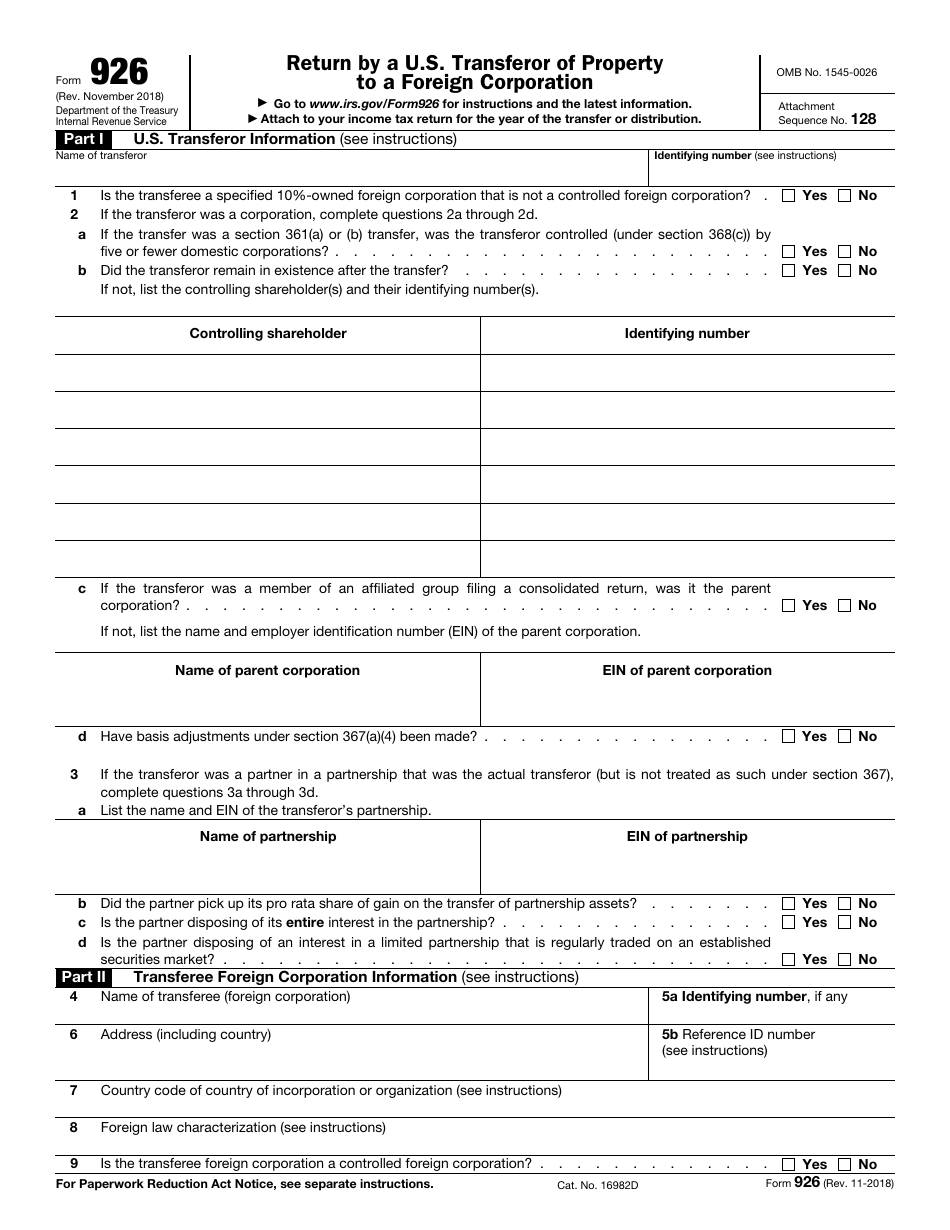

- Part I. U.S. Transferor Information. Here, the applicant must enter their full name and identifying number. According to the instructions, an individual's identifying number is their social security number, the identifying number of other types of applicants is their employer identification number. If a transferor is a corporation, then they must designate additional information which includes information about their shareholders, name of the parent corporation (if applicable), information about a partnership if a transferor was a partner there.

- Part II. Transferee Foreign Corporation Information. Applicants use this part of the document to designate information about the transferee, such as a transferee's name, address, country of an organization, foreign law characterization, identifying number (if any), etc. In the "foreign law characterization" line, the applicant must designate the entity classification of the foreign corporation (which is a transferee) under the laws of the country of the organization.

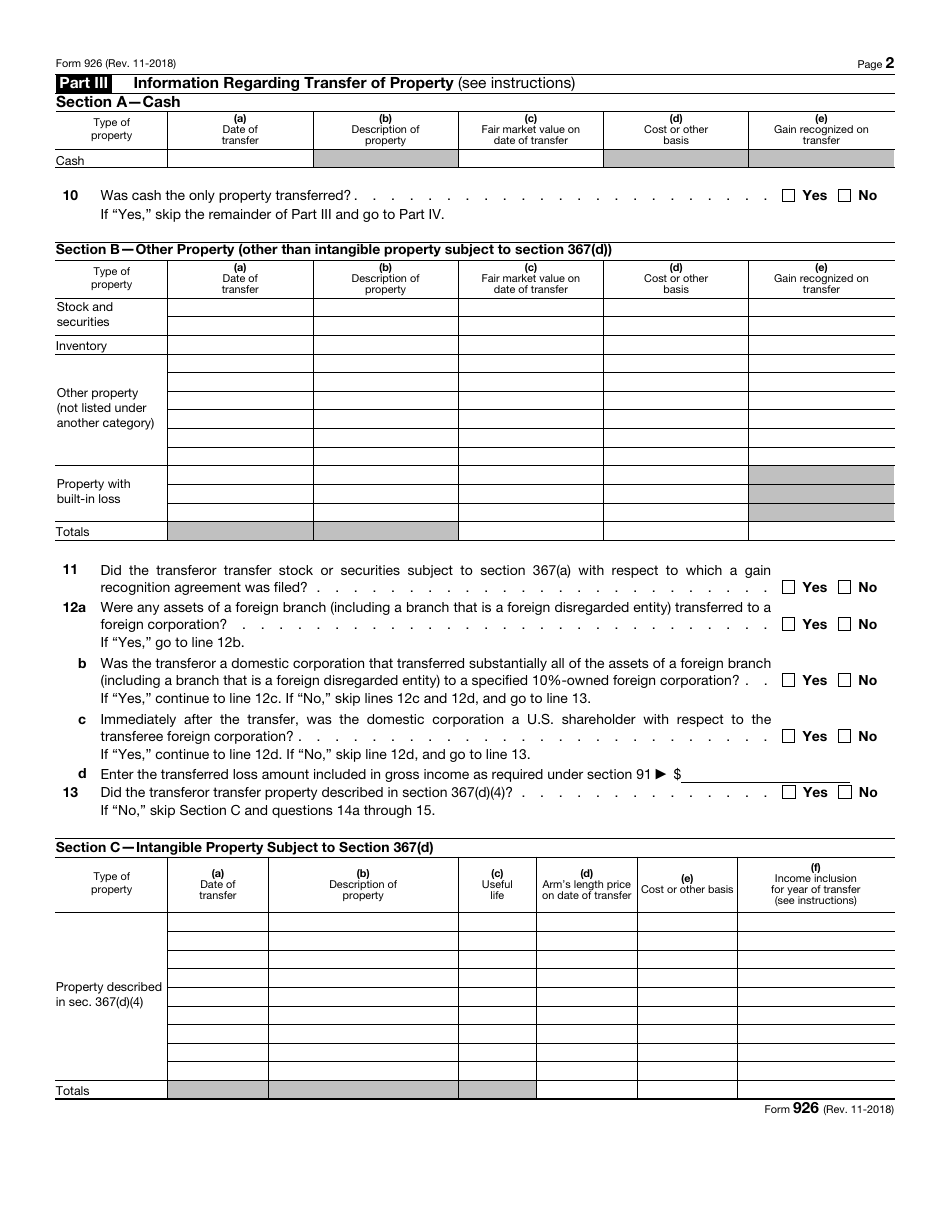

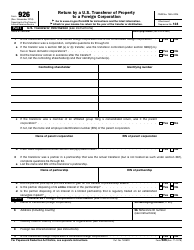

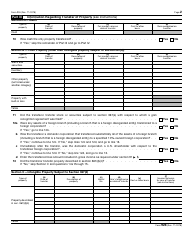

- Part III. Information Regarding Transfer of Property. This part of the document is divided into three sections: cash, other property, and intangible property subject. In every section, the applicant must fill in the gaps: typer of the property transferred, date of the transfer, description of the property, cost of the property or other basis, gain recognized on the transfer, etc.

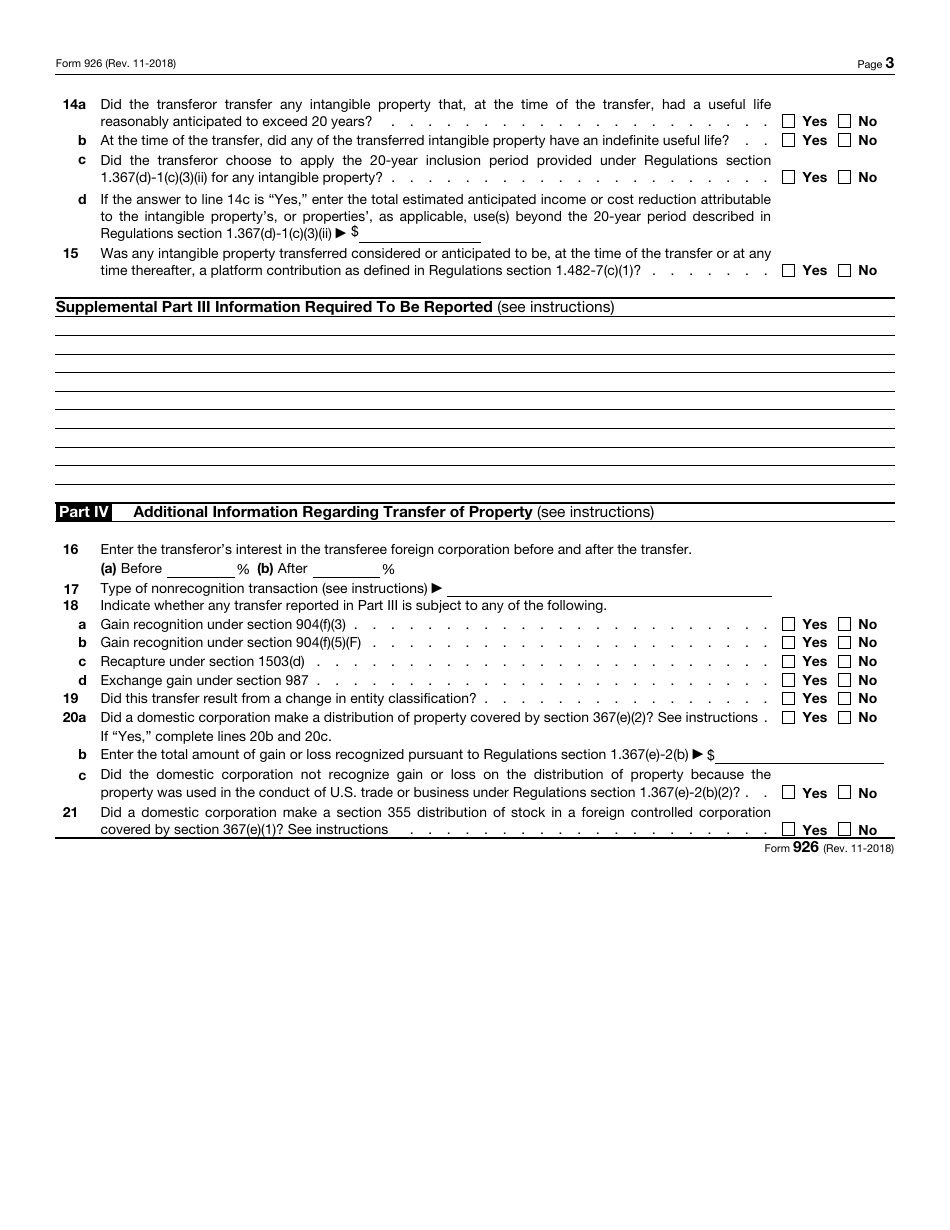

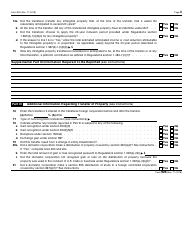

- Part III. Additional Information Regarding Transfer of Property. In the last part of the application, filers must state certain types of information, which include the type of nonrecognition transaction, the transferor's interest, the total amount of the recognized gain and loss, etc.

The applicant can use the official instructions for Form 926 which were developed by the IRS to make this process easier. They provide more detailed information on how tofill out each line, as well as useful definitions and samples. For example, according to the instructions, intangible property subjects include:

- Copyright, literary, musical, or artistic composition;

- Trademark, trade name, or brand name;

- Franchise, license, or contract;

- Patent, invention, formula, process, design, pattern, or know-how;

- Method, program, system, procedure, campaign, survey, study, forecast, estimate, customer list, or technical data;

- Any other item the value or potential value of which is not attributable to tangible property or the services of any individual.

Download IRS Form 926 Return by a U.S. Transferor of Property to a Foreign Corporation

1

2

3