![]() This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 1065X

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 1065X

for the current year.

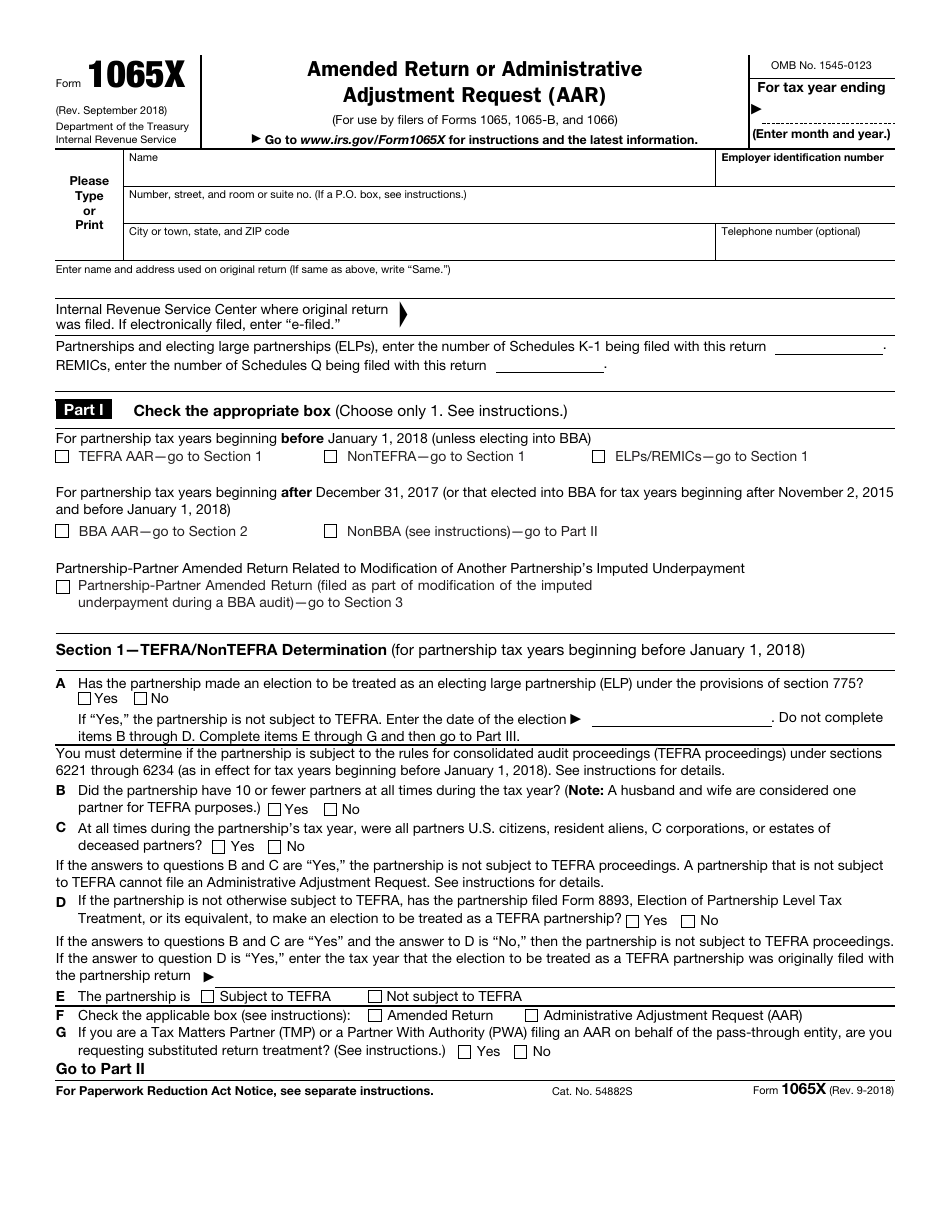

IRS Form 1065X Amended Return or Administrative Adjustment Request (AAR)

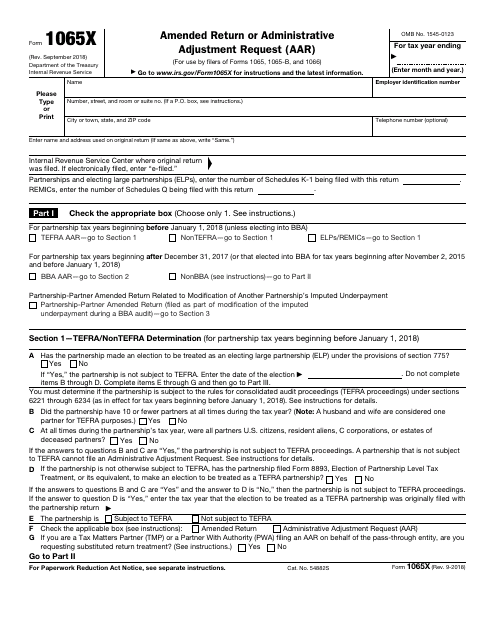

What Is Form 1065X?

IRS Form 1065X, Amended Return or Administrative Adjustment Request (AAR) is an Internal Revenue Service (IRS) form used to:

-

Correct items on the previously filed forms:

- IRS Form 1065, U.S. Return of Partnership Income (a document used by the IRS to obtain information on income, credits, deductions, gains, losses, and other data fully describing the operation of the partnership)

- IRS Form 1065-B, U.S. Return of Income for Electing Large Partnerships (a document used to submit the gains and losses, income, deductions, and other data outlining the performance of the electing large partnership)

- IRS Form 1066, U.S. Real Estate Mortgage Investment Conduit (REMIC) Income Tax Return (a document used to report the gains, losses, deductions, and income from the operation of a REMIC - an entity that functions to provide investment in mortgage obligations and receives favorable tax treatment).

-

Make an AAR for the previously filed forms - any partner is allowed to change the reporting of the items relating to the partnership;

-

File an amended return by a partnership-partner of a Bipartisan Budget Act of 2015 (BBA) partnership.

The latest version of the form was released by the Internal Revenue Service (IRS) on September 1, 2018 , with all previous editions obsolete. A fillable 1065X Form is available for download below.

Form 1065X Instructions

The IRS provides a set of official instructions for filing the form. They provide specific details on how tofill out the form.

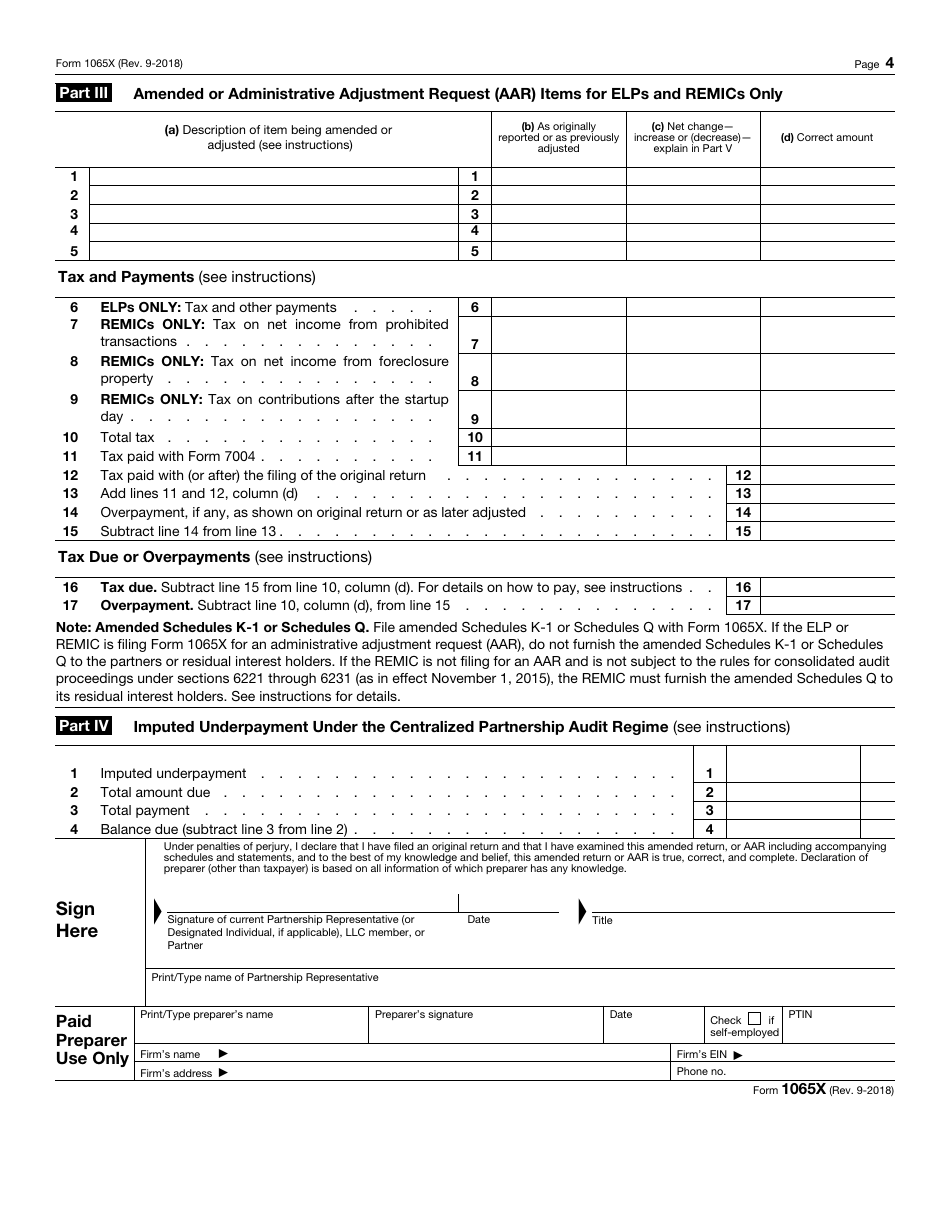

- The 1065X Form must be mailed to the service center where you have filed the original return within three years after the date on which the partnership return is filed or the last day for filing the partnership return for the year;

- Attach the appropriate form, statement, or schedule if the corrected item must be supported with it. If you include documents from previous-year tax returns, make sure you label them "do not process";

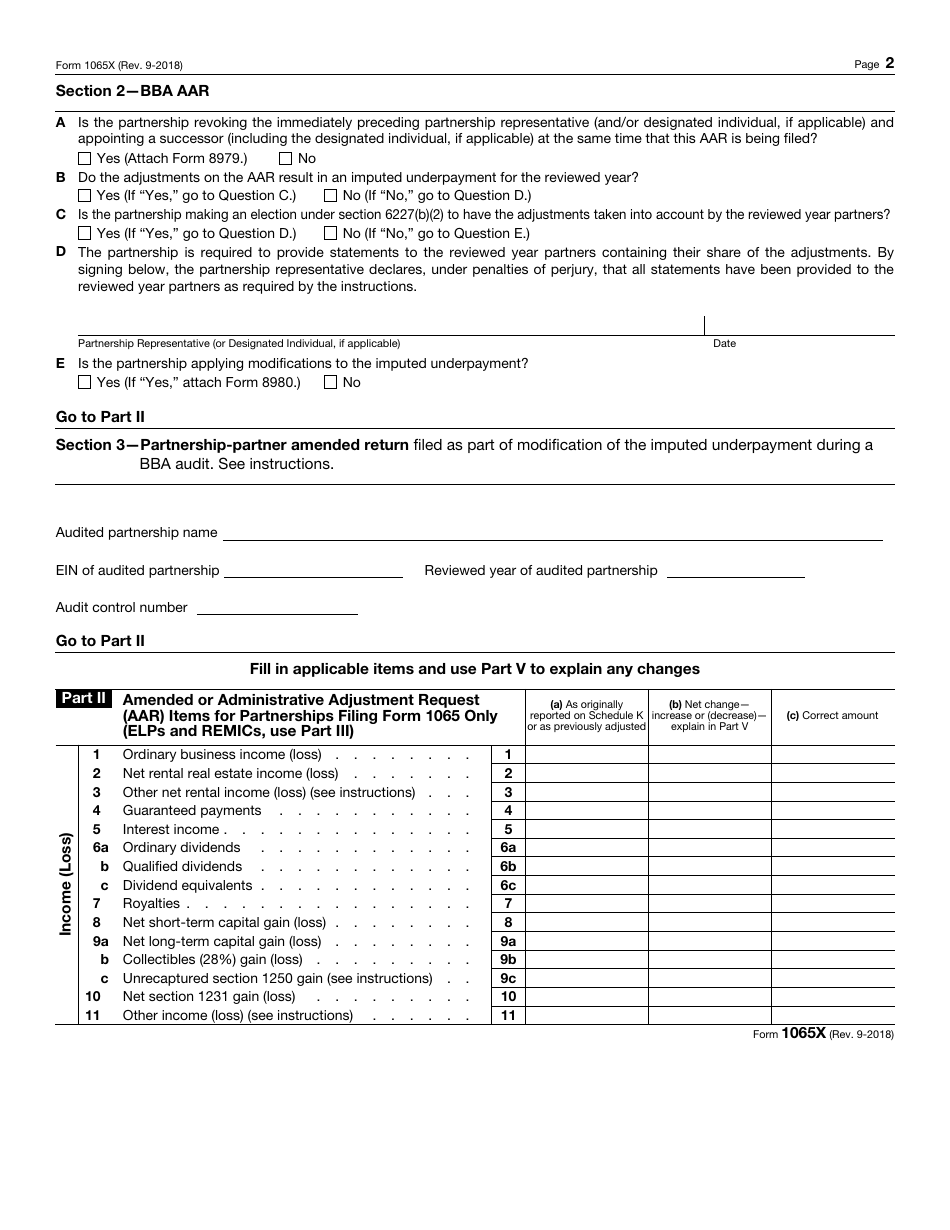

- You can use the form to report an imputed underpayment and any related penalties and interest;

- If the AAR or amended return must be filed electronically or you choose to file it electronically, you need to use IRS Form 8082, Notice of Inconsistent Treatment or Administrative Adjustment Request (AAR).

Download IRS Form 1065X Amended Return or Administrative Adjustment Request (AAR)

1

2

3

4

5