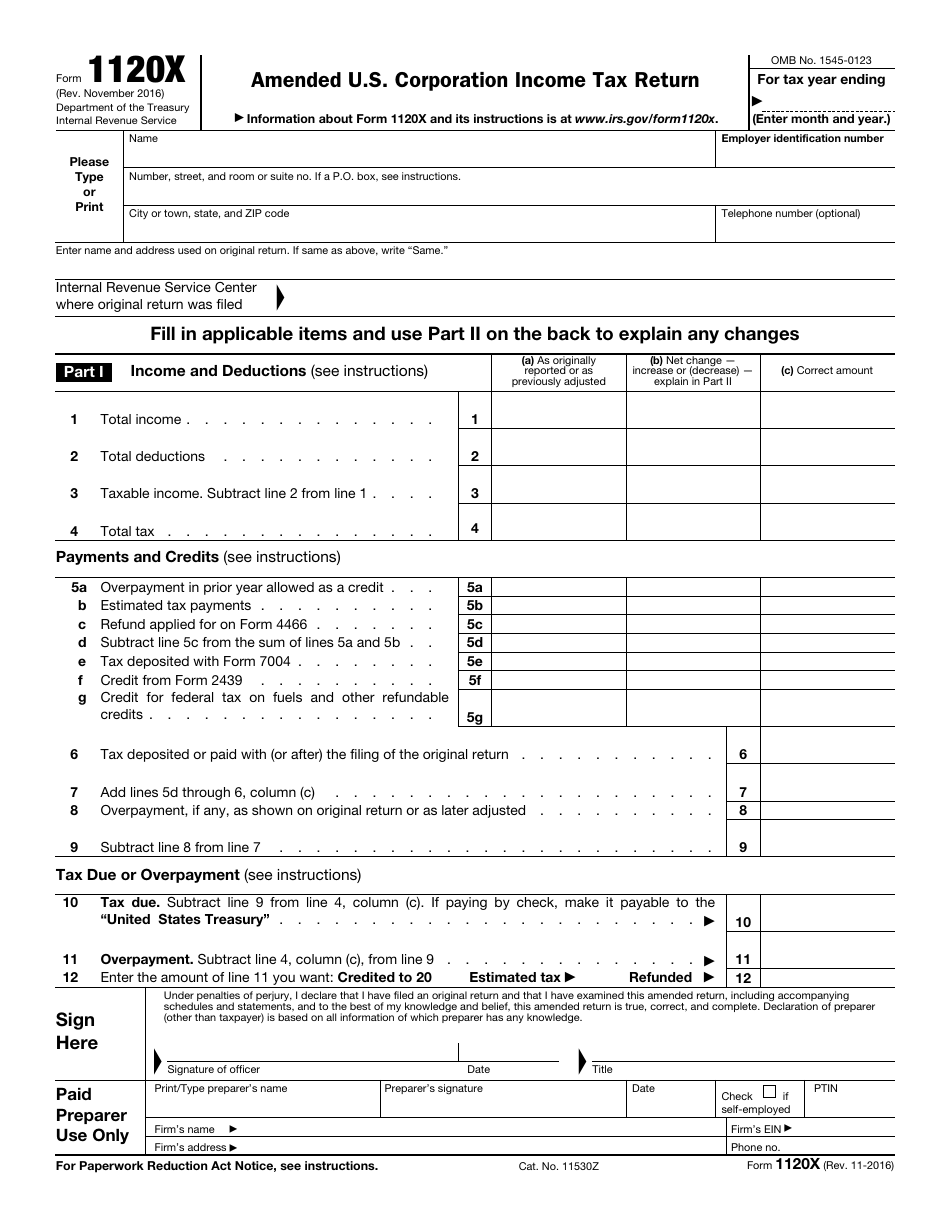

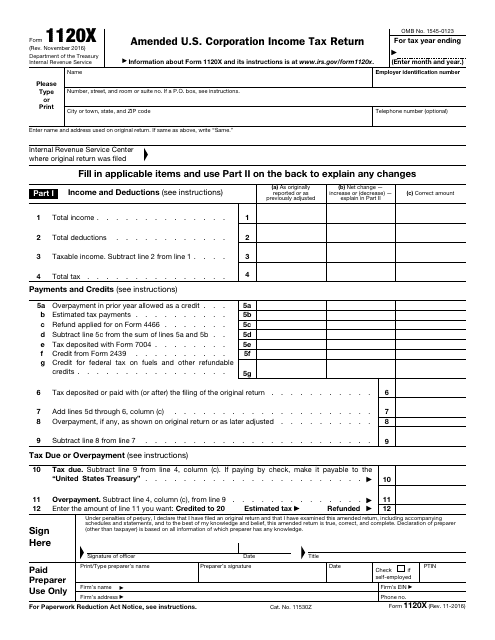

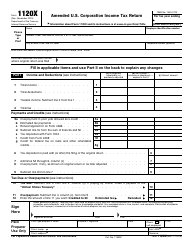

IRS Form 1120-X Amended U.S. Corporation Income Tax Return

What Is IRS Form 1120X?

IRS Form 1120X, Amended U.S. Corporation Income Tax Return - also known as the Amended Corporate Tax Return - is a form filed with the Internal Revenue Service (IRS) by corporations in order to correct mistakes made on Form 1120 (or Form 1120-A*), a claim for refund, or an examination, and also, to make certain elections after the prescribed deadline. Form 1120X was issued by the IRS and last revised on November 1, 2016 .

Form 1120X fillable version is available for download through the link below.

Where to Mail IRS Form 1120X?

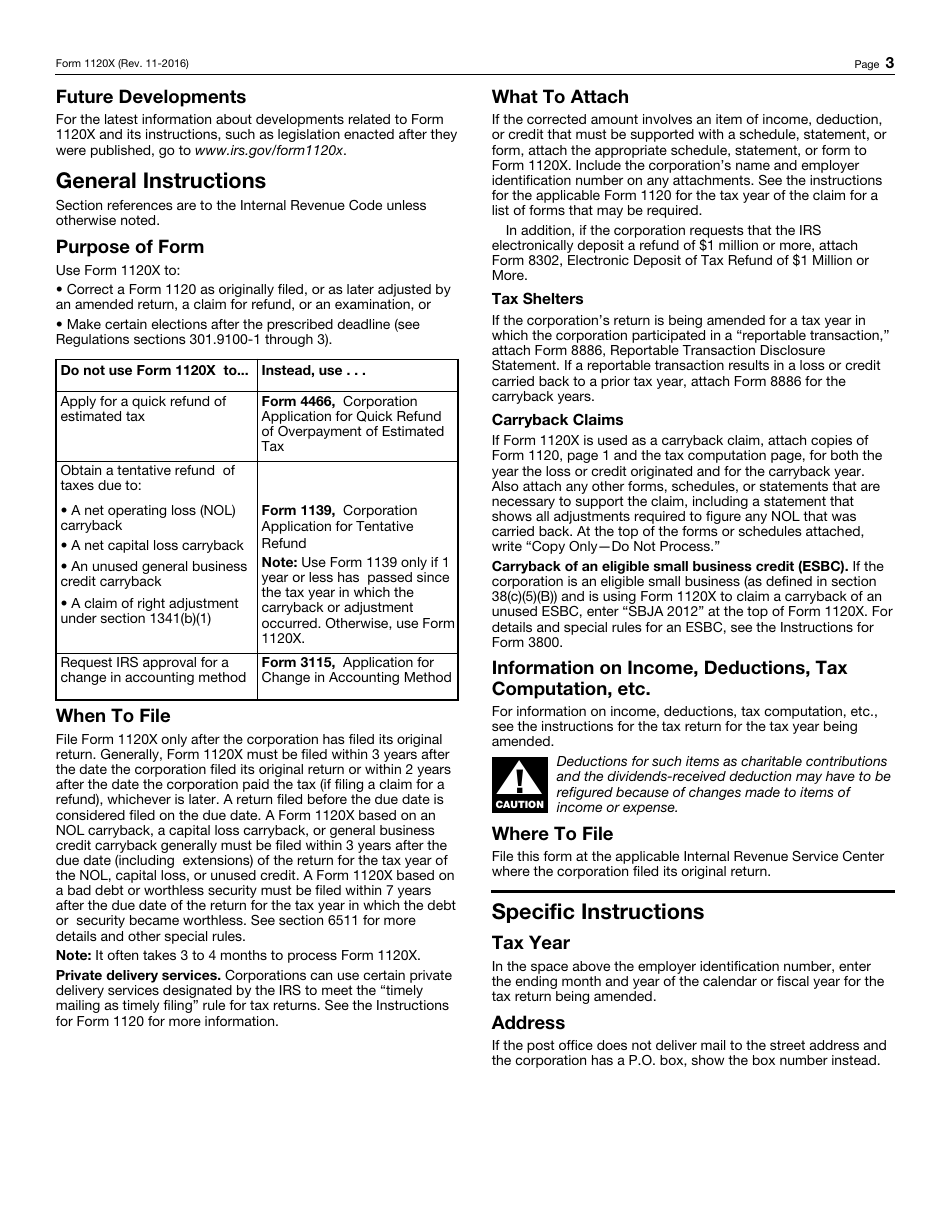

File this form at the applicable IRS Center where the corporation filed its original return.

*IRS Form 1120-A was the short version of the 1120 and was discontinued after the 2006 tax year.

What to Include with the 1120X?

If the corrected amounts on IRS 1120X Form must be supported with a schedule, statement, or a form, the corporation must attach these documents as required. The corporation's name and employer identification number (EIN) must be included in every attachment. In addition, Form 8302, Electronic Deposit of Tax Refund of $1 Million or More, must be attached if the corporation is requesting an electronic refund of over a $1 million.

In case the amendment is made for a tax year when the corporation conducted a "reportable transaction" Form 8886, Reportable Transaction Disclosure Statement must be attached.

If Form 1120X is filed as a carryback claim, the corporation is required to attach copies of the first page of Form 1120, as well as the tax computation page, for both the tax year when the loss or credit occurred and for the carryback year. The copies should include a note stating "Copy Only-Do Not Process."

IRS Form 1120X Instructions

Corporations may file this form only after having filed its original return. Generally, the due date for filing this document is 3 years after the date of the original return or 2 years after the date when the tax was paid by the corporation (if filing a claim for a refund), whichever is later.

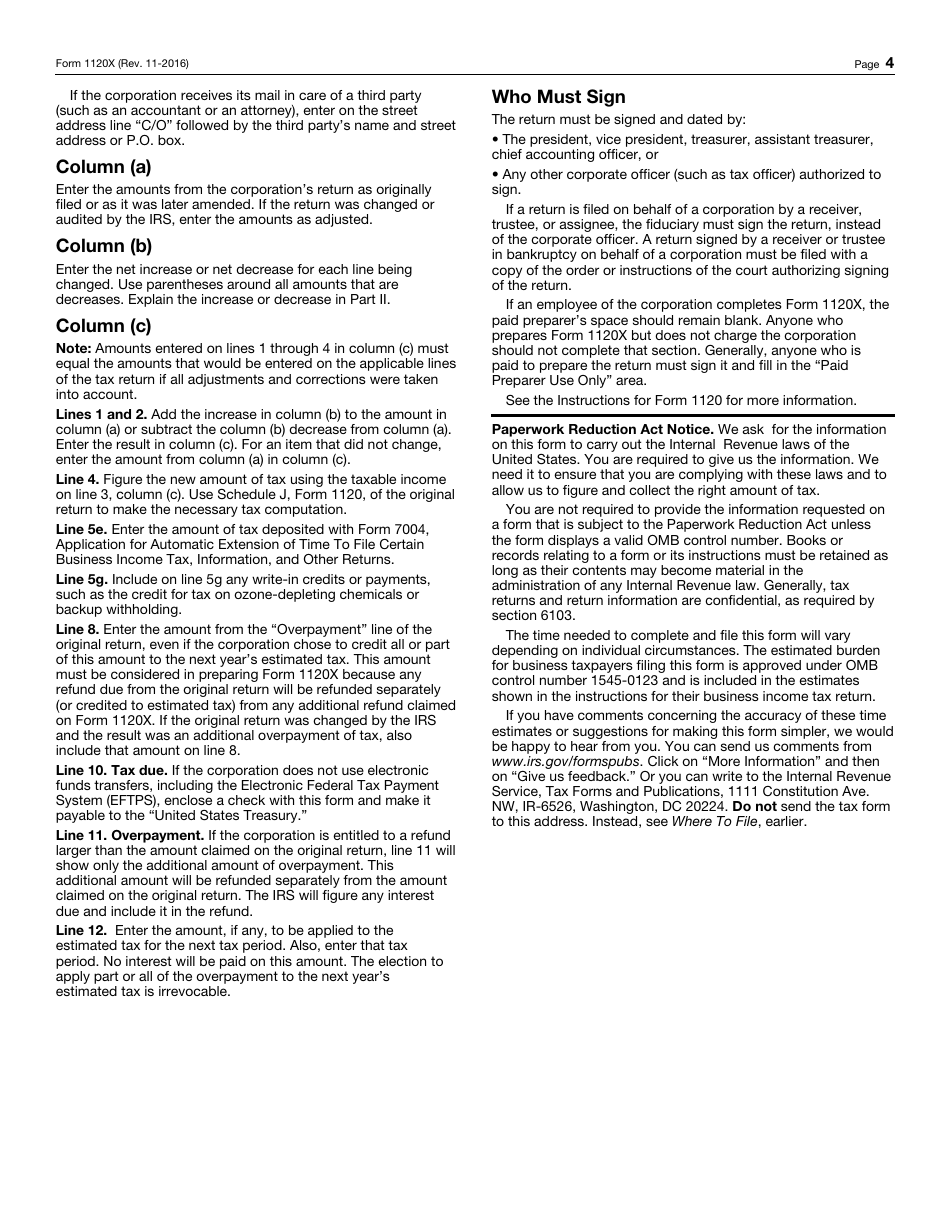

The 1120X Form must be signed and dated by the corporation's president, vice president, chief accounting officer, treasurer, assistant treasurer, or any corporate officer authorized to sign. A return that is filed by a receiver, trustee, or an assignee on behalf of a corporation must be signed by the fiduciary. Generally, anyone who gets paid to prepare the return is required to sign it and fill in the "Paid Preparer Use Only" section. If the person who prepares Form 1120X does not charge the corporation, the section mentioned above should remain blank.

IRS 1120-X Related Forms

- 1120, U.S. Corporation Income Tax Return. Domestic corporations must file and submit Form 1120 to calculate their income tax liability and report losses, gains, deductions, income, and credits to the IRS.

- 1120-C, U.S. Income Tax Return for Cooperative Associations. This form is used by corporations that operate on a cooperative basis to report their income, gains, losses, deductions, and credits, as well as to figure their income tax liability.

- 1120-F, U.S. Income Tax Return of a Foreign Corporation. Foreign corporations file this form to report their income, gains, losses, deductions, and credits, and to figure their U.S. income tax liability.

- 1120-H, U.S. Income Tax Return for Homeowners Associations. Homeowners associations use this form to exclude the exempt function income from its gross income.

- 1120-L, U.S. Life Insurance Company Income Tax Return. Life insurance companies file this form to report income, gains, losses, deductions, and credits, and to figure their income tax liability.

- 1120-S, U.S. Income Tax Return for an S Corporation. This is a form used for reporting the income, gains, losses, deductions, and credits of a domestic corporation or any other entity for any tax year covered by an election to be an S corporation.

- 1120-FSC, U.S. Income Tax Return of a Foreign Sales Corporation. Foreign Sales Corporation (FSC) or small FSC use this form to report their income, deductions, losses, gains, credits, and income tax liability.

- 1120-IC-DISC, Interest Charge Domestic International Sales Corporation Return. This is a form filed by interest charge domestic international sales corporations (IC-DISCs), former DISCs, and former IC-DISCs.

- 1120-POL, U.S. Income Tax Return for Certain Political Organizations. This form is used by political organizations and certain exempt organizations to report their political organization taxable income and income tax liability section 527.

- 1120-ND, Return for Nuclear Decommissioning Funds and Certain Related Persons. Nuclear decommissioning funds use this form to report income earned, contributions received, the administrative expenses of fund operation, the tax on modified gross income, and the section 4951 initial taxes.

- 1120-PC, U.S. Property and Casualty Insurance Company Income Tax Return. This form is filed with the IRS to report the income, gains, losses, deductions, and credits, and to figure the income tax liability of insurance companies, apart from life insurance companies.

- 1120-REIT, U.S. Income Tax Return for Real Estate Investment Trusts. Corporations, trusts, and associations electing to be treated as Real Estate Investment Trusts use this form to report their income, deductions, credits, gains, losses, certain penalties, and income tax liability.

- 1120-RIC, U.S. Income Tax Return for Regulated Investment Companies. Regulated investment companies (RIC) file this form with the IRS to report their income, deductions, gains, losses, credits, and to calculate their income tax liability.

- 1120-SF, U.S. Income Tax Return for Settlement Funds (Under Section 468B). Qualified settlement funds file this form with the IRS to report transfers received, income earned, deductions claimed, distributions made, and a designated or qualified settlement fund income tax liability.

- 1120-W, Estimated Tax for Corporations. Corporations file this form to estimate their tax liability and to figure the amount of their estimated tax payments.

Download IRS Form 1120-X Amended U.S. Corporation Income Tax Return

1

2

3

4