![]() This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 5405

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 5405

for the current year.

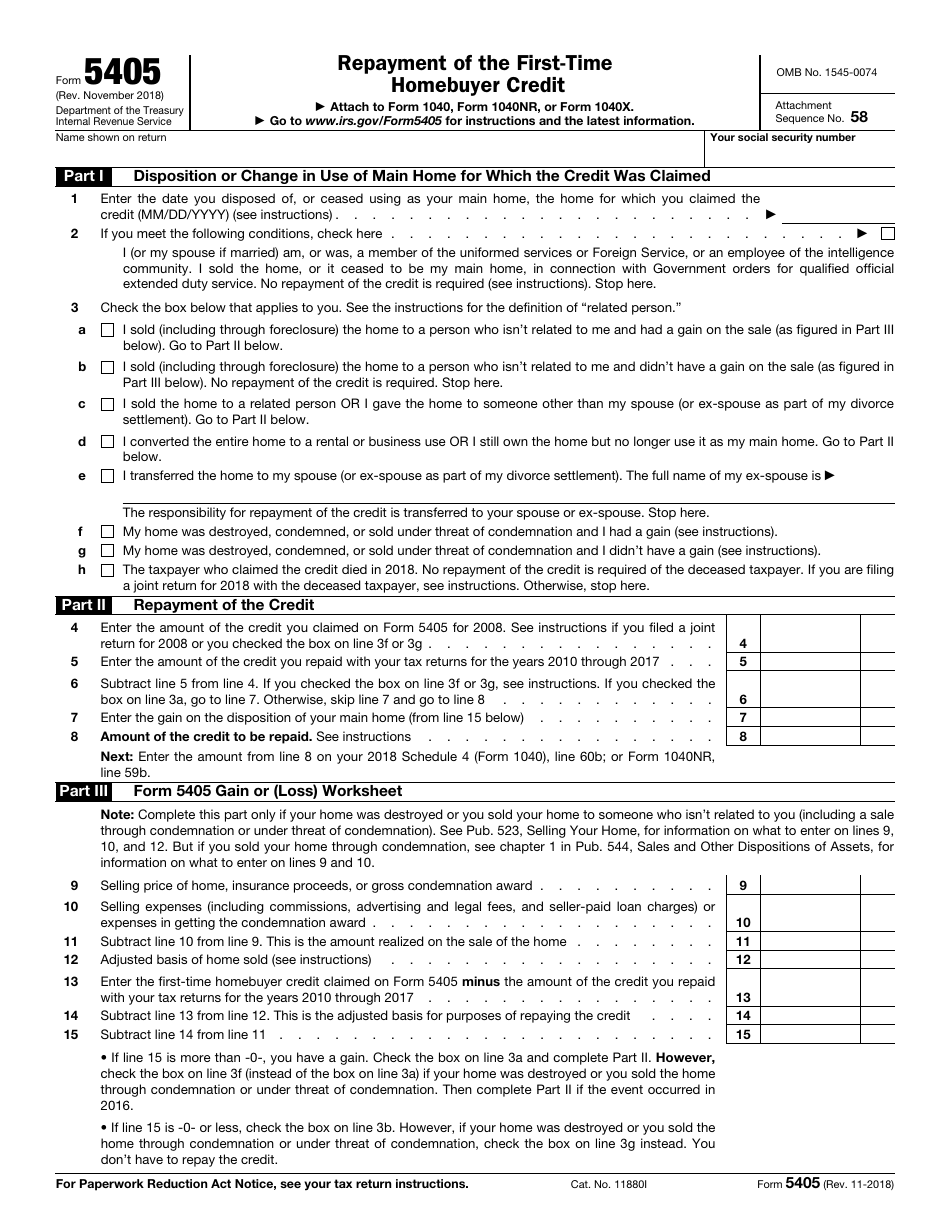

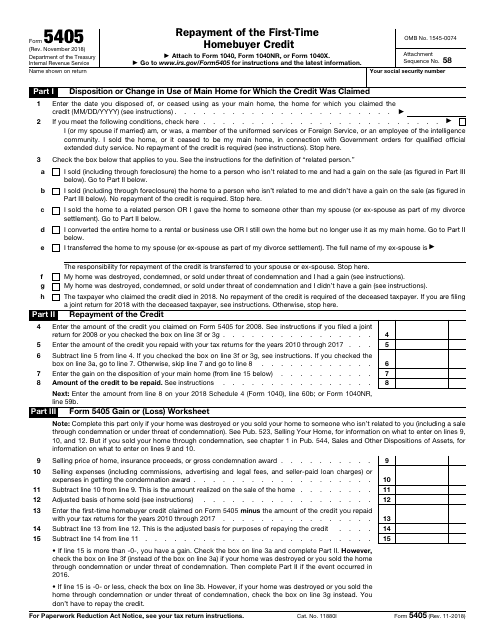

IRS Form 5405 Repayment of the First-Time Homebuyer Credit

What Is IRS Form 5405?

IRS Form 5405, Repayment of the First-Time Homebuyer Credit , is a document used to inform the Internal Revenue Service (IRS) that the home you bought and for which you claimed the credit is not your main home anymore. You can calculate the amount you need to repay with your tax return on this form as well. Find more details in the official filing instructions issued by the IRS.

Alternate Name:

- First-Time Homebuyer Form.

The form was issued by the IRS and last revised on November 1, 2018 . An up-to-date fillable Form 5405 is available for download below.

IRS Form 5405 Instructions

You are required to fill out and submit this form if you purchased a home in 2008 with the IRS homebuyer credit and if:

- You disposed of it during the tax year;

- This home is not your primary residence anymore;

- In all other cases, specify your repayment on Schedule 4 (Form 1040) or Form 1040NR, as applicable. If you claimed the credit on the tax return jointly with your spouse, the IRS considers that each of you is allowed half of the credit for repaying purposes. Each spouse who meets the requirements must complete a separate IRS 5405.

The repayment rule has several exceptions:

- If you had to sell your home to anyone who is not related to you due to condemnation or a condemnation threat and you do not obtain a new home within two years, the repayment you owe is limited to the gain on your disposition. The gain can be figured out in Part III of this form. If the credit amount is higher than the gain you receive, you do not have to repay it. The same applies if your form was destroyed;

- If you hand over the home to your spouse or ex-spouse, the receiving spouse becomes responsible for repaying the credit;

- If the individual who claimed the credit died, the repayment of the remaining amount is not required. However, if the spouses claimed the credit on the joint return, the surviving individual must repay his or her part of the credit.

Submit the completed form along with your tax return when applying for tax deductions.

How to Complete IRS Form 5405?

IRS 5405 is a one-page document divided into three parts. Most lines you need to fill out are self-explanatory. Read through the step-by-step guide below before filing:

- Enter only your name and Social Security number on the top of the form, even if you claimed this credit on the joint return;

- Part I. Disposition or Change in Use of Main Home for Which the Credit Was Claimed. Fill out this part if you claimed the first-time homebuyer credit, and this home is not your main residence anymore, including the situations when you sold the home, abandoned it, converted it to business or rental property, your home was destroyed or condemned, or the individual who claimed the credit died;

- Line 2. If you or your spouse are or were an employee of the intelligence community, or a member of the Foreign Service or uniformed services and must serve on qualified official extended duty due to Government orders, you do not have to repay the credit. Check this line, and skip the rest of the form;

- Part II. Repayment of the Credit. Use this part to determine the amount you have to repay. Do not fill out this part if any of the abovementioned exceptions applies to you;

- Part III. Form 5405 Gain or (Loss) Worksheet. Fill out this part to calculate your gain or loss if your home was destroyed or if you sold it to someone not related to you.

The term "not related" includes not just your spouse, ancestors, or lineal descendants, but also a corporation or partnership in which you own more than 50% in value of the outstanding stocks or of the capital interest.