![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 990, 990-EZ Schedule G

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 990, 990-EZ Schedule G

for the current year.

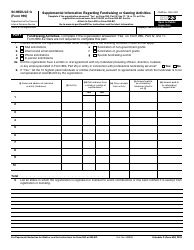

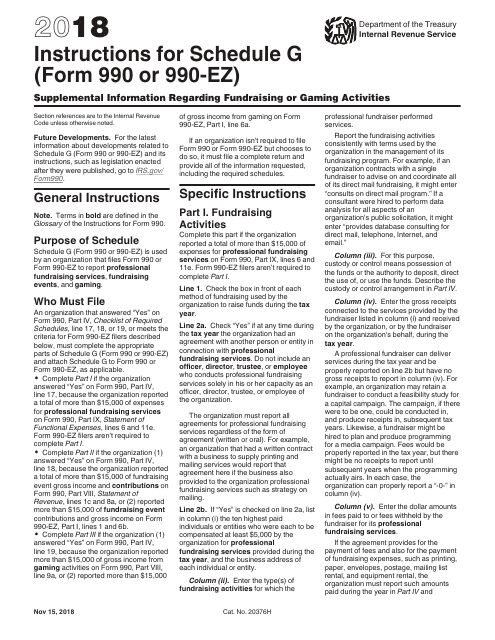

Instructions for IRS Form 990, 990-EZ Schedule G Supplemental Information Regarding Fundraising or Gaming Activities

This document contains official instructions for IRS Form 990 Schedule G and IRS Form 990-EZ Schedule G . Both forms are released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 990 (990-EZ) Schedule G is available for download through this link.

FAQ

Q: What is the IRS Form 990?

A: The IRS Form 990 is a tax return form that tax-exempt organizations in the United States must file each year.

Q: What is the purpose of Schedule G?

A: Schedule G is used to provide supplemental information regarding fundraising or gaming activities conducted by the organization.

Q: Which organizations need to file Schedule G?

A: Organizations that engage in fundraising or gaming activities must file Schedule G along with their Form 990 or 990-EZ.

Q: What information is required on Schedule G?

A: Schedule G requires information about specific fundraising or gaming activities, such as revenue, expenses, and the use of gaming facilities.

Q: Are there any specific instructions for completing Schedule G?

A: Yes, the instructions for Schedule G provide detailed guidance on how to complete the form, including examples and definitions of key terms.

Q: When is Schedule G due?

A: Schedule G is due along with the organization's Form 990 or 990-EZ, which is typically due on the 15th day of the 5th month after the end of the organization's fiscal year.

Q: Is Schedule G required for all tax-exempt organizations?

A: No, Schedule G is only required for organizations that engage in fundraising or gaming activities.

Instruction Details:

- This 4-page document is available for download in PDF;

- Not applicable for the current tax year. Choose a more recent version to file this year's taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

Download Instructions for IRS Form 990, 990-EZ Schedule G Supplemental Information Regarding Fundraising or Gaming Activities

1

2

3

4