IRS 990 Forms, Schedules and Instructions

What Are the Different 990 Forms?

The IRS 990 Forms are a series of documents filled out by certain tax-exempt organizations in order to provide the Internal Revenue Service (IRS) with their financial information. The information provided via these forms is usually available for the public and often serves as the primary source of information about a specific organization.

The main documents included in the series include:

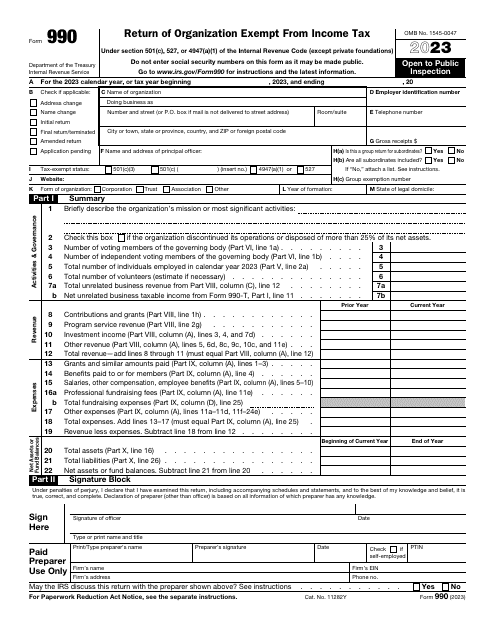

- IRS Form 990, Return of Organization Exempt from Income Tax. This form is filled out by tax-exempt organizations, section 527 political organizations, and nonexempt charitable trusts to report to the IRS gross income, disbursements, receipts, and other information required by section 6033;

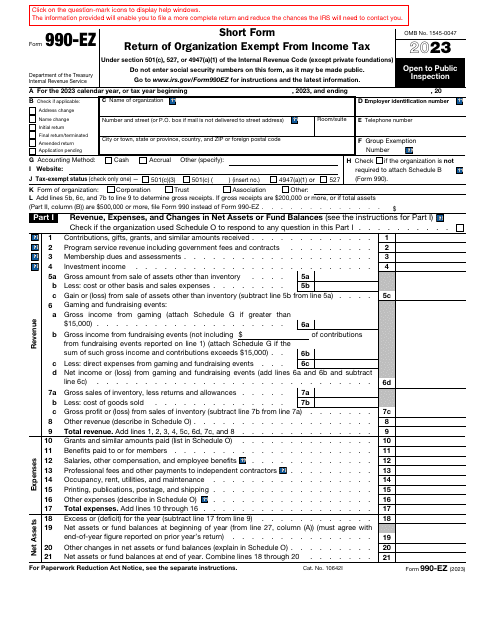

- IRS Form 990-EZ, Short Form Return of Organization Exempt from Income Tax. This is a short version of the previous form used to provide the IRS with the financial information of Section 527 political organizations, tax-exempt organizations, and nonexempt charitable trusts. Only organizations with gross receipts less than $200,000 and total assets less than $500,000 are allowed to fill out this version of the form;

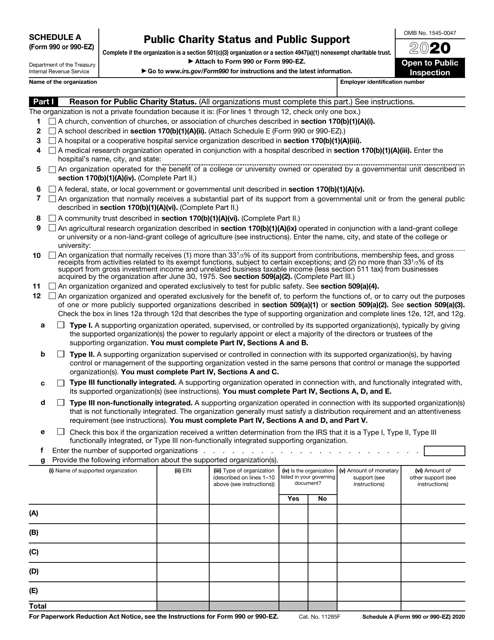

- IRS Form 990-N, Electronic Notice (e-Postcard). This form has an electronic version only. This form can be filed by small tax-exempt organizations whose annual gross receipt is $50,000 or less;

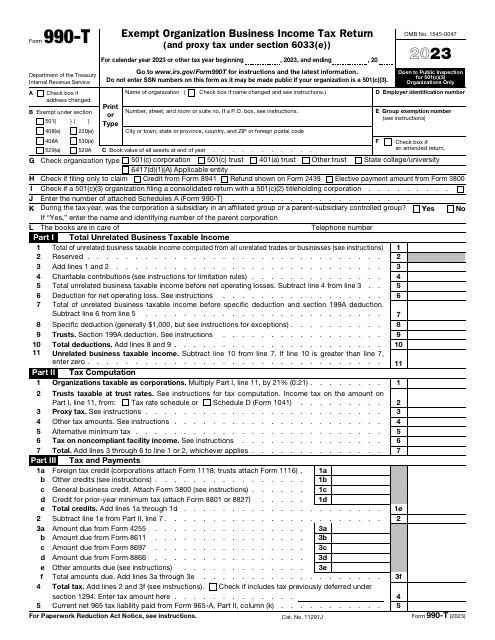

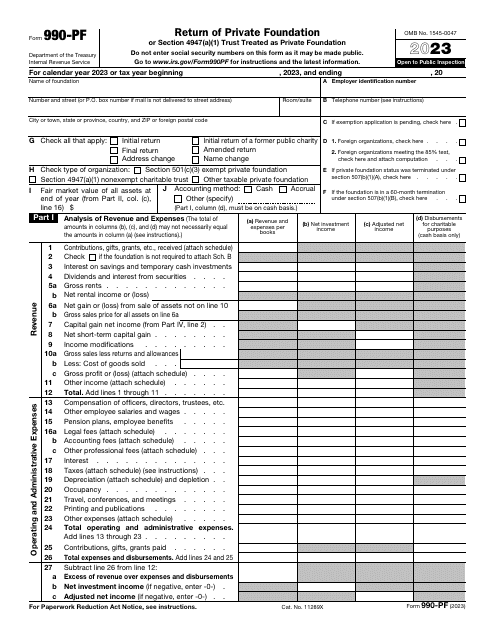

- IRS Form 990-PF, Return of Private Foundation or Section 4947(a)(1) Nonexempt Charitable Trust Treated as a Private Foundation. Fill out this form to report charitable distributions and activities, as well as to calculate the tax based on an investment income.

There are 16 schedules used with the IRS 990 Forms:

- Schedule A, Public Charity Status and Public Support;

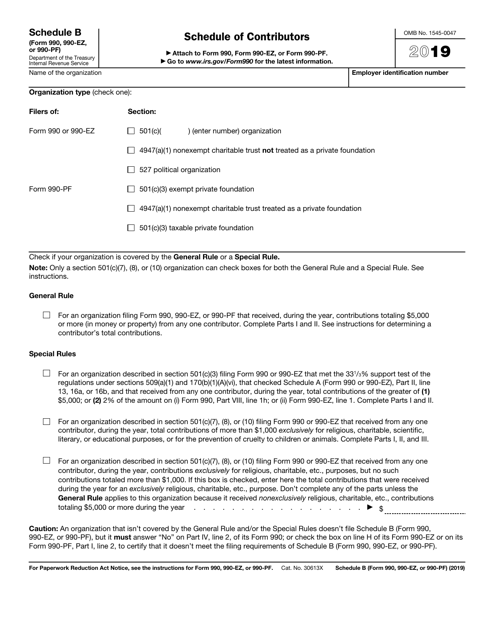

- Schedule B, Schedule of Contributors;

- Schedule C, Political Campaign and Lobbying Activities;

- Schedule D, Supplemental Financial Statements;

- Schedule E, Schools;

- Schedule F, Statement of Activities Outside the United States;

- Schedule G, Supplemental Information Regarding Fundraising or Gaming Activities;

- Schedule H, Hospitals;

- Schedule I, Supplemental Information on Grants and Other Assistance to Organizations, Governments, and Individuals in the United States;

- Schedule J, Compensation Information;

- Schedule K, Supplemental Information on Tax-Exempt Bonds;

- Schedule L, Transactions with Interested Persons;

- Schedule M, Non-Cash Contributions;

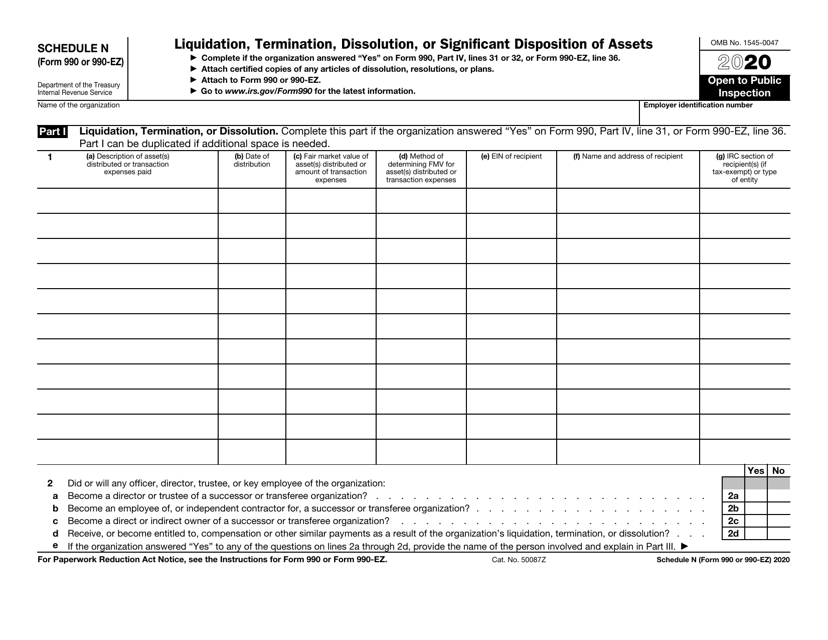

- Schedule N, Liquidation, Termination, Dissolution, or Significant Disposition of Assets;

- Schedule O, Supplemental Information to Form 990;

- Schedule R, Related Organizations and Unrelated Partnerships.

Use these schedules to provide additional information or to specify the information provided on the main forms, if applicable.

When Are 990 Forms Due?

The IRS 990 Forms’ due date is the 15th day of the 5th month after the end of the organization’s accounting period, e.g., if you use the calendar year for accounting, the filing deadline for your organization will fall on May 15. If the due date falls on a Saturday, Sunday, or a legal holiday, file the form by the next business day. Use IRS Form 8868, Application for Automatic Extension of Time to File an Exempt Organization Return, to request an extension to file your forms. If you failed to file the forms by the due date anyway, enclose a separate attachment with your explanations.

If you do not file the forms timely and completely, you must pay $20 penalty for each day your form is late. If your organization is considered as a large one, i.e. the annual gross receipt of your organization exceeds $1,046,500, you will have to pay $100 for each day the failure continues. The maximum penalty for each return form will not exceed $10,000 ($52,000 for large organizations) or 5% of the organization’s gross receipts for the year, whichever is less.

Documents:

40

This is a fiscal form used by tax-exempt organizations required to inform tax organizations about their earnings, expenses, and achievements over the course of the year.

This form, also known as the private foundation tax return, can also substitute Form 1041, if a trust has no taxable income. Use this form to calculate the tax on the income from an investment and to report charitable activities and distributions.

This form is used to supply the Internal Revenue Service (IRS) with information regarding receipts, gross income, disbursements, and other data used by tax-exempt organizations to summarize their work during the tax year.

This is a fiscal document used by nonprofit organizations to report the main specifics of their operations to tax authorities.