![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 8801

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 8801

for the current year.

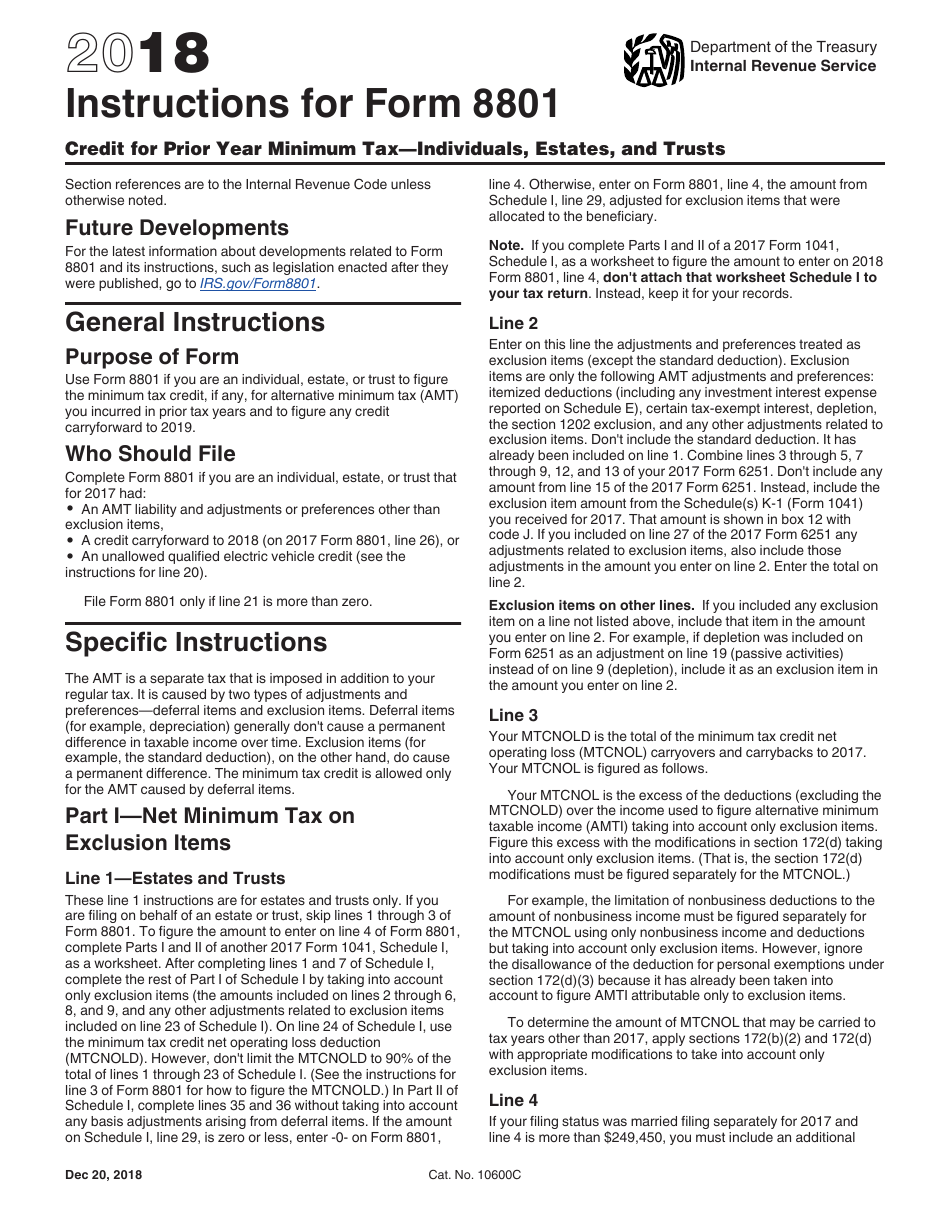

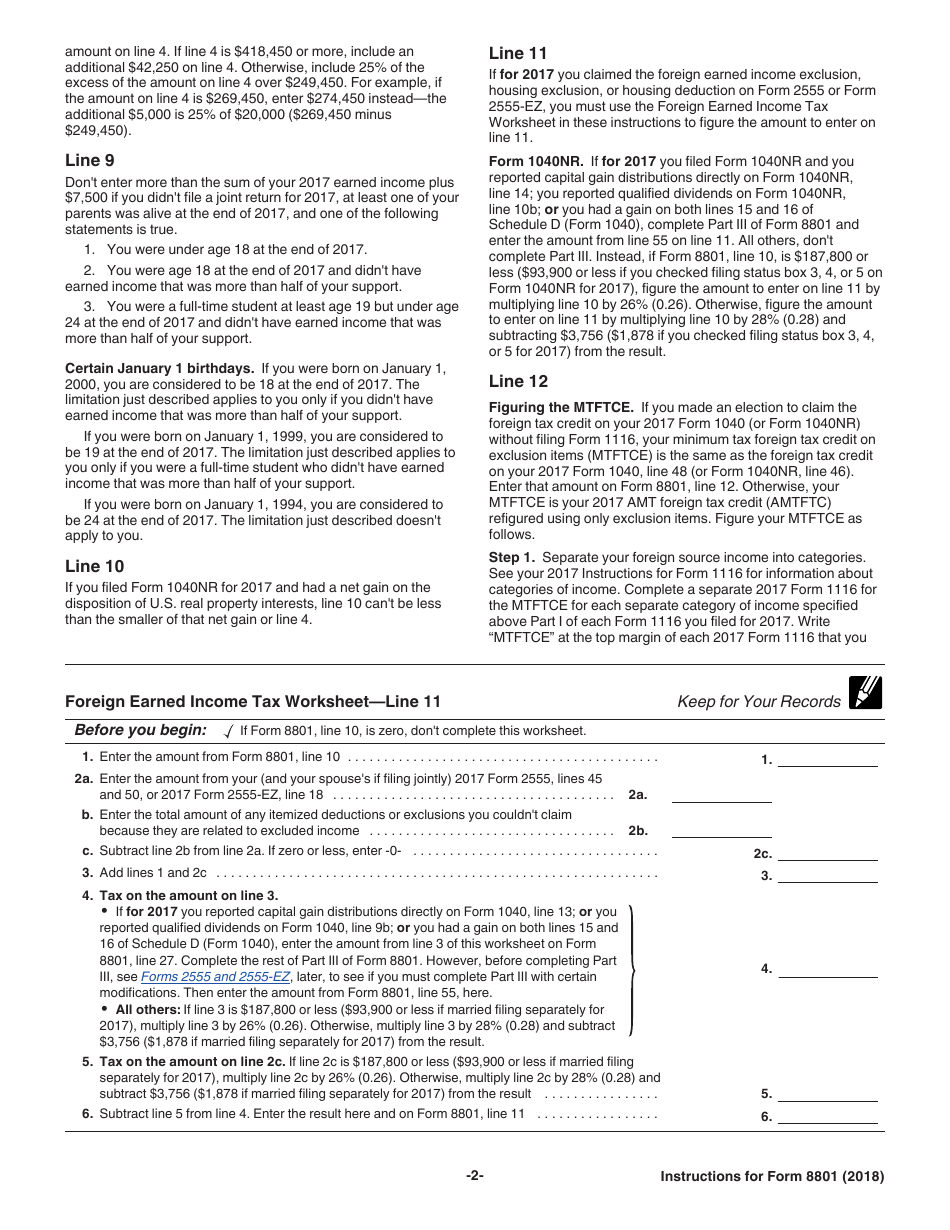

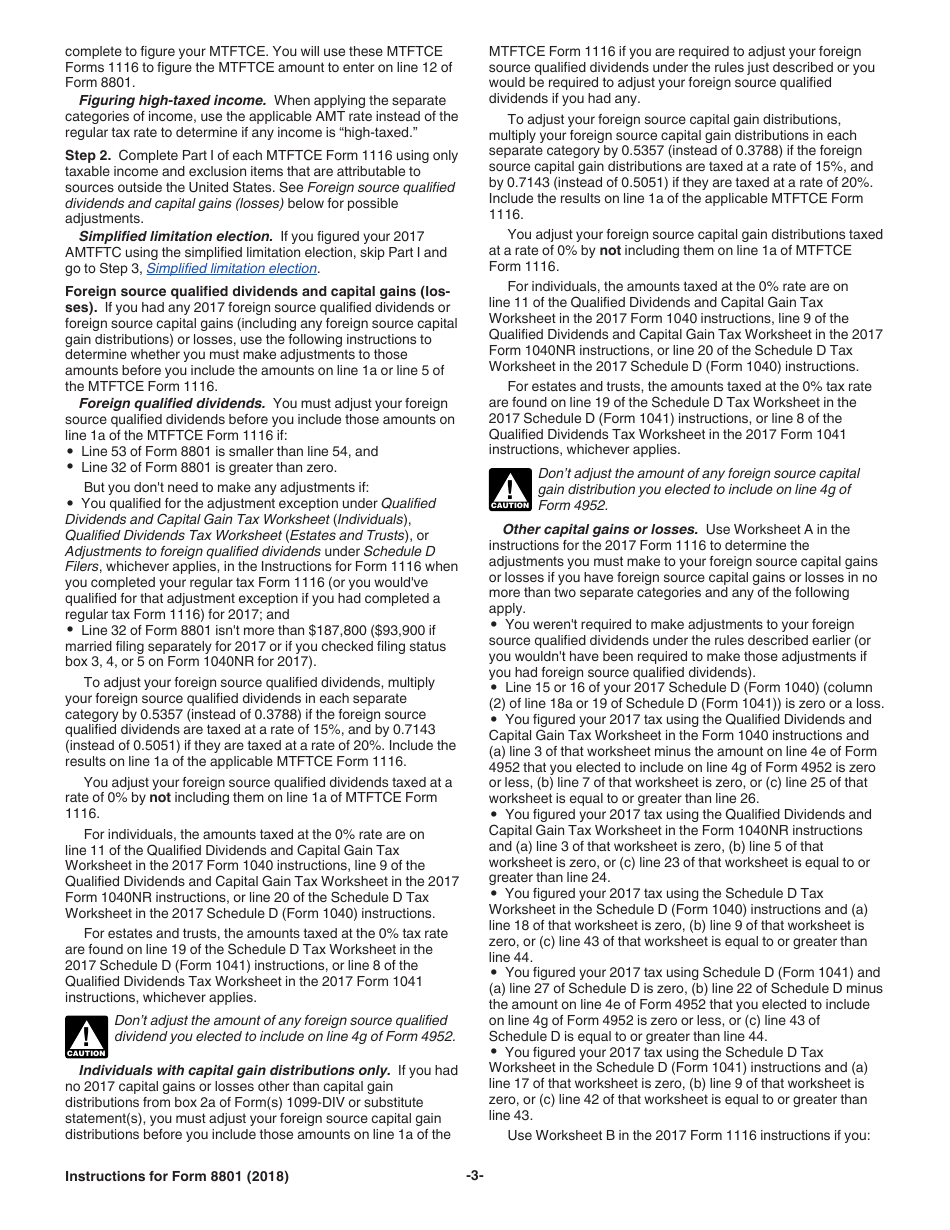

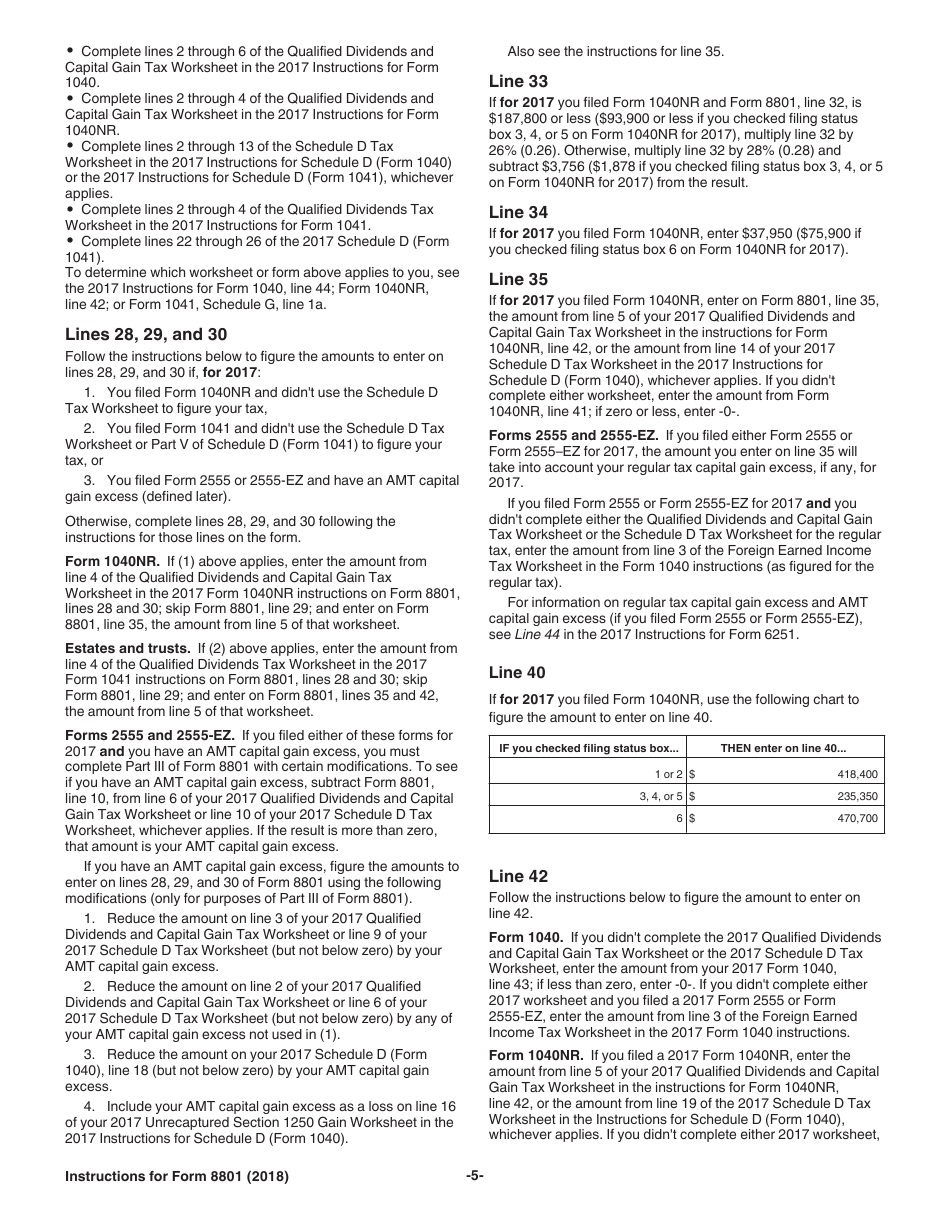

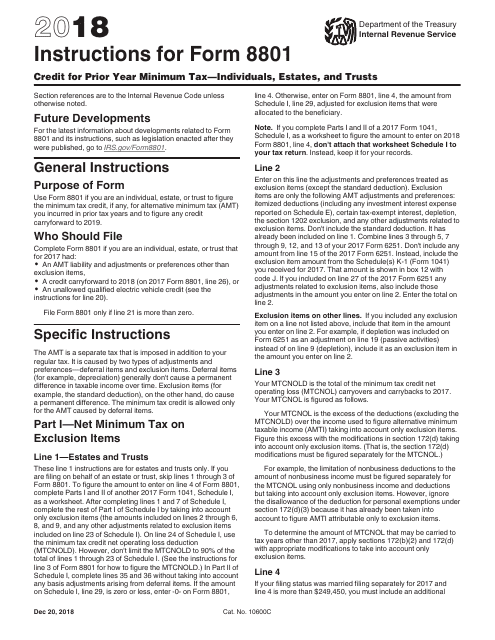

Instructions for IRS Form 8801 Credit for Prior Year Minimum Tax - Individuals, Estates, and Trusts

This document contains official instructions for IRS Form 8801 , Credit for Minimum Tax - Individuals, Estates, and Trusts - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 8801 is available for download through this link.

FAQ

Q: What is IRS Form 8801?

A: IRS Form 8801, Credit for Prior Year Minimum Tax - Individuals, Estates, and Trusts, is a tax form used to calculate and claim the credit for prior year minimum tax.

Q: Who needs to file IRS Form 8801?

A: Individuals, estates, and trusts who have paid alternative minimum tax in a previous year may need to file IRS Form 8801.

Q: What is the purpose of IRS Form 8801?

A: The purpose of IRS Form 8801 is to determine the amount of credit for prior year minimum tax that can be applied to reduce current year regular tax liability.

Q: How do I fill out IRS Form 8801?

A: To fill out IRS Form 8801, you will need to provide information about your alternative minimum tax liability and calculate the available credit for prior year minimum tax.

Q: When is the deadline to file IRS Form 8801?

A: The deadline to file IRS Form 8801 is usually the same as the deadline to file your annual income tax return, which is April 15th of the following year.

Q: What happens if I don't file IRS Form 8801?

A: If you are eligible for the credit for prior year minimum tax and do not file IRS Form 8801, you may miss out on reducing your current year tax liability and potentially overpaying your taxes.

Q: Is there a fee to file IRS Form 8801?

A: No, there is no fee to file IRS Form 8801.

Q: Can I e-file IRS Form 8801?

A: As of now, IRS Form 8801 cannot be e-filed and must be filed by mail.

Instruction Details:

- This 6-page document is available for download in PDF;

- Not applicable for the current tax year. Choose a more recent version to file this year's taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

Download Instructions for IRS Form 8801 Credit for Prior Year Minimum Tax - Individuals, Estates, and Trusts

1

2

3

4

5

6