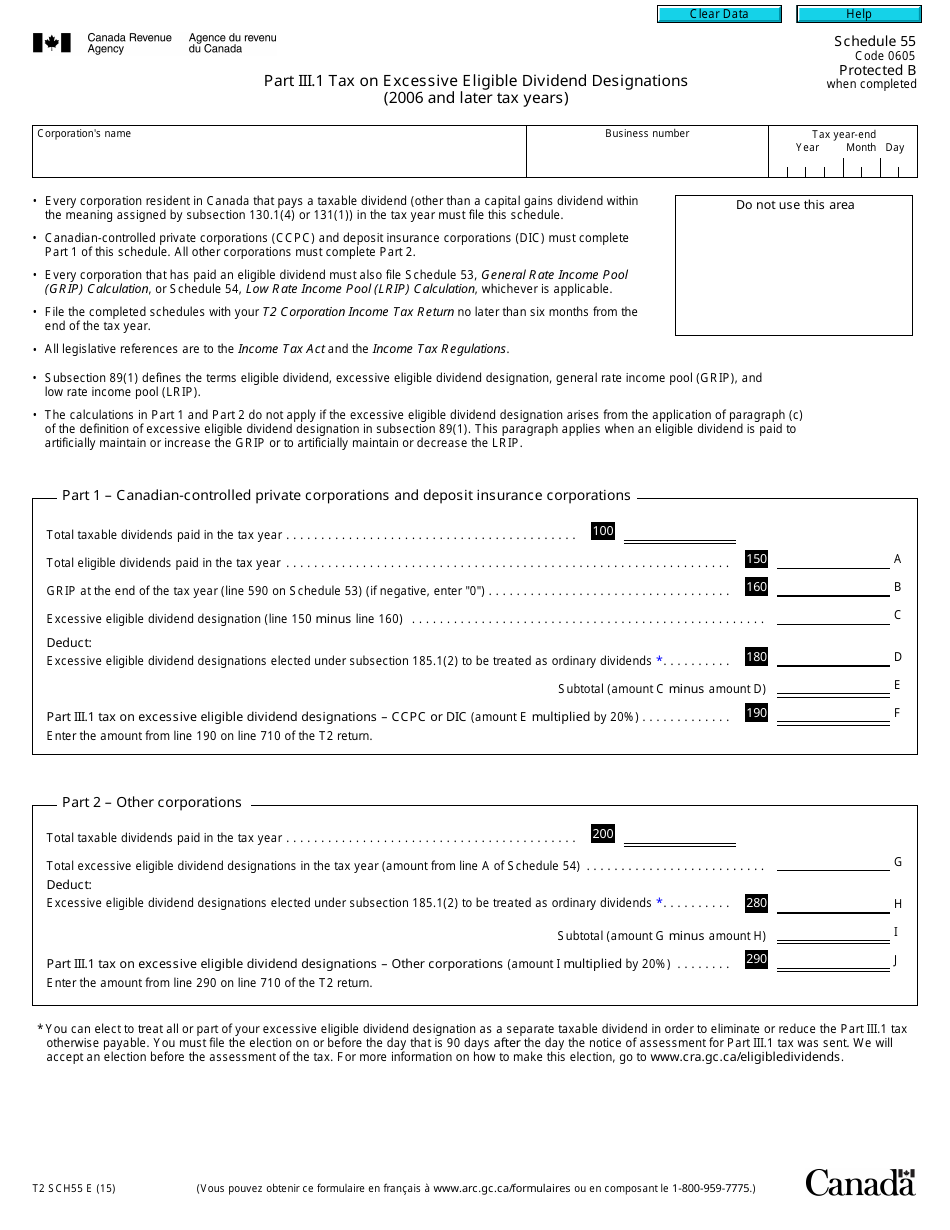

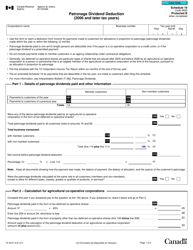

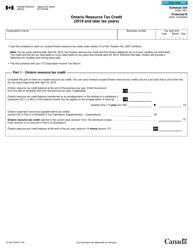

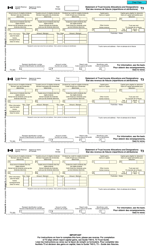

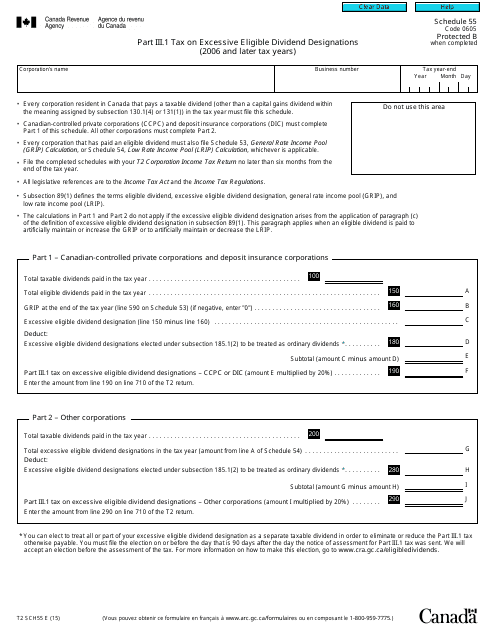

Form T2 Part 55 Part Iii.1 Tax on Excessive Eligible Dividend Designations (2006 and Later Tax Years) - Canada

Form T2 Part 55 Part III.1 is used in Canada to calculate and report the tax on excessive eligible dividend designations for tax years starting in 2006 and onwards. It is a specific section of the T2 corporate income tax return where corporations disclose and calculate the additional tax payable when they designate an excessive amount of dividends as eligible dividends.

The Form T2 Part 55, Part III.1 - Tax on Excessive Eligible Dividend Designations for 2006 and later tax years, is filed by corporations in Canada.

FAQ

Q: What is Form T2 Part 55 Part III.1?

A: Form T2 Part 55 Part III.1 is a tax form used in Canada for reporting excessive eligible dividend designations in tax years 2006 and later.

Q: What is excessive eligible dividend designation?

A: Excessive eligible dividend designation refers to designating a dividend as an eligible dividend when the corporation does not have enough corporate earnings and profits to support the designation.

Q: When is Form T2 Part 55 Part III.1 used?

A: Form T2 Part 55 Part III.1 is used when a corporation has made excessive eligible dividend designations in tax years 2006 and later.

Q: What is the purpose of Form T2 Part 55 Part III.1?

A: The purpose of Form T2 Part 55 Part III.1 is to calculate and report the tax on excessive eligible dividend designations.

Q: Are there any penalties for excessive eligible dividend designations?

A: Yes, there may be penalties for excessive eligible dividend designations, including additional taxes and interest.

Q: Do I need to file Form T2 Part 55 Part III.1 if I haven't made any excessive eligible dividend designations?

A: No, you do not need to file Form T2 Part 55 Part III.1 if you have not made any excessive eligible dividend designations.

Q: Is Form T2 Part 55 Part III.1 applicable to individual taxpayers?

A: No, Form T2 Part 55 Part III.1 is not applicable to individual taxpayers. It is specifically for corporations.

Q: What should I do if I have made excessive eligible dividend designations?

A: If you have made excessive eligible dividend designations, you should complete and file Form T2 Part 55 Part III.1 to calculate and report the tax on those designations.

Q: Can I make excessive eligible dividend designations in current tax years?

A: It is important to ensure that any dividend designations are supported by sufficient corporate earnings and profits. Making excessive eligible dividend designations can result in penalties and additional taxes.