![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form RC7294

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form RC7294

for the current year.

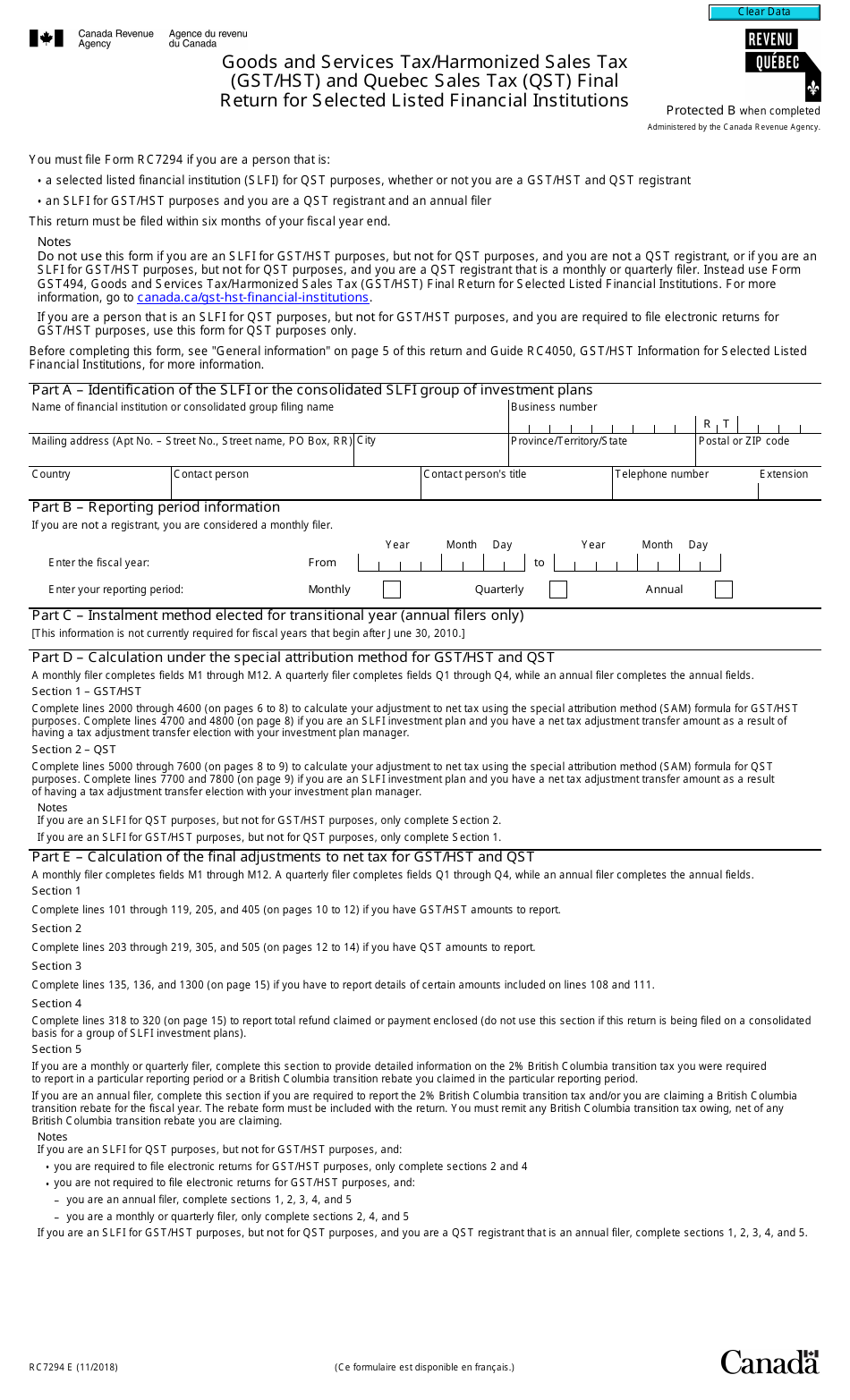

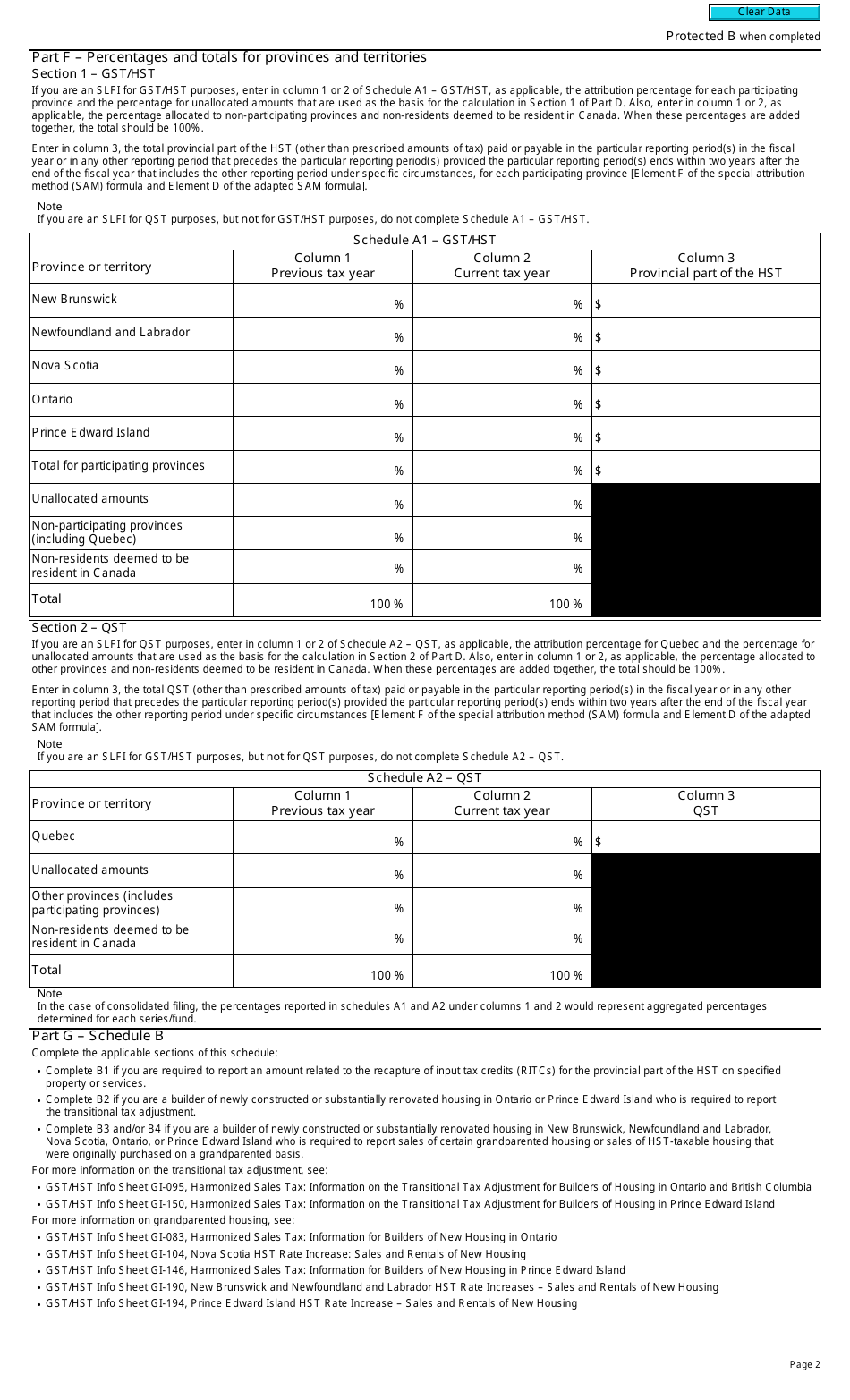

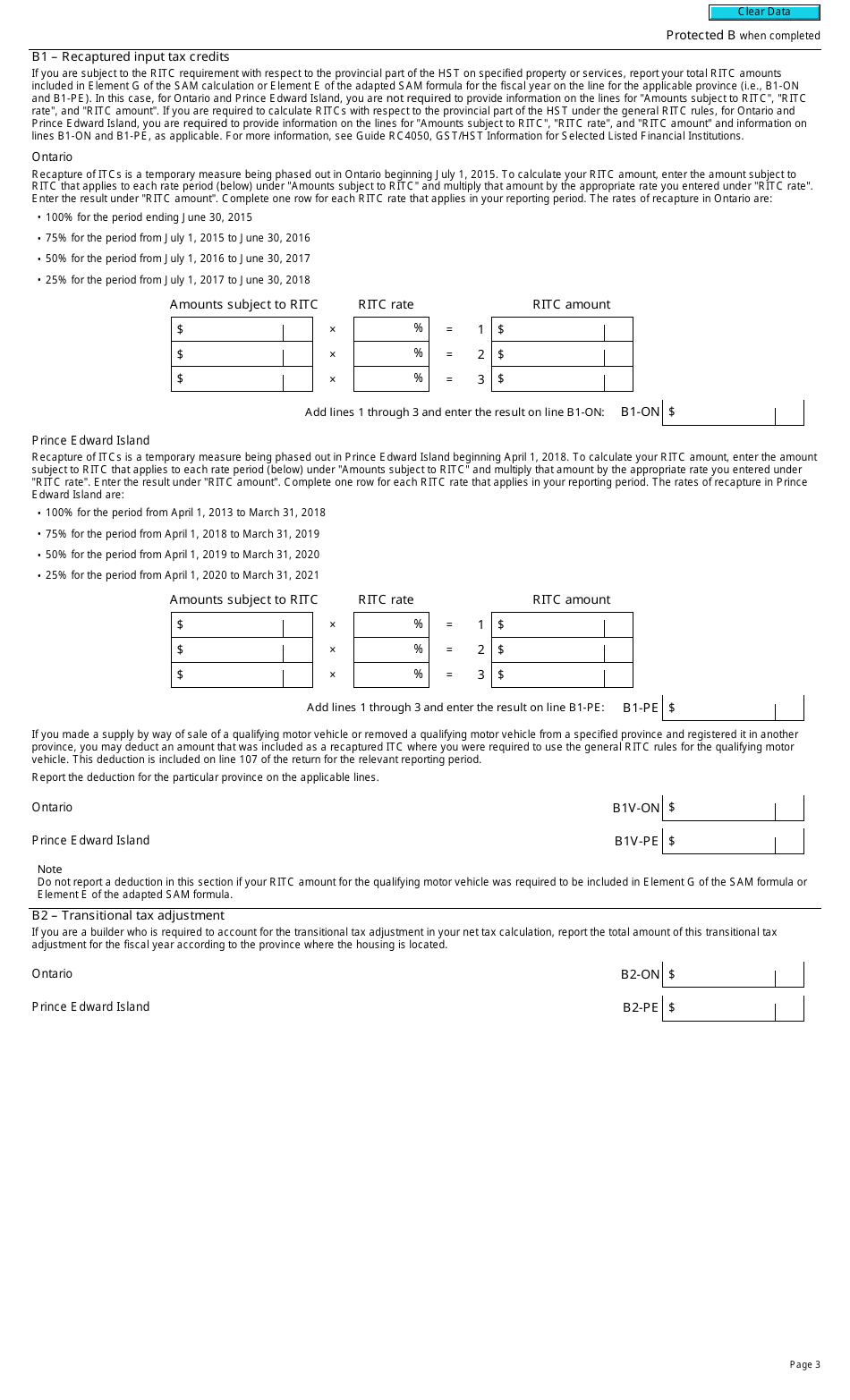

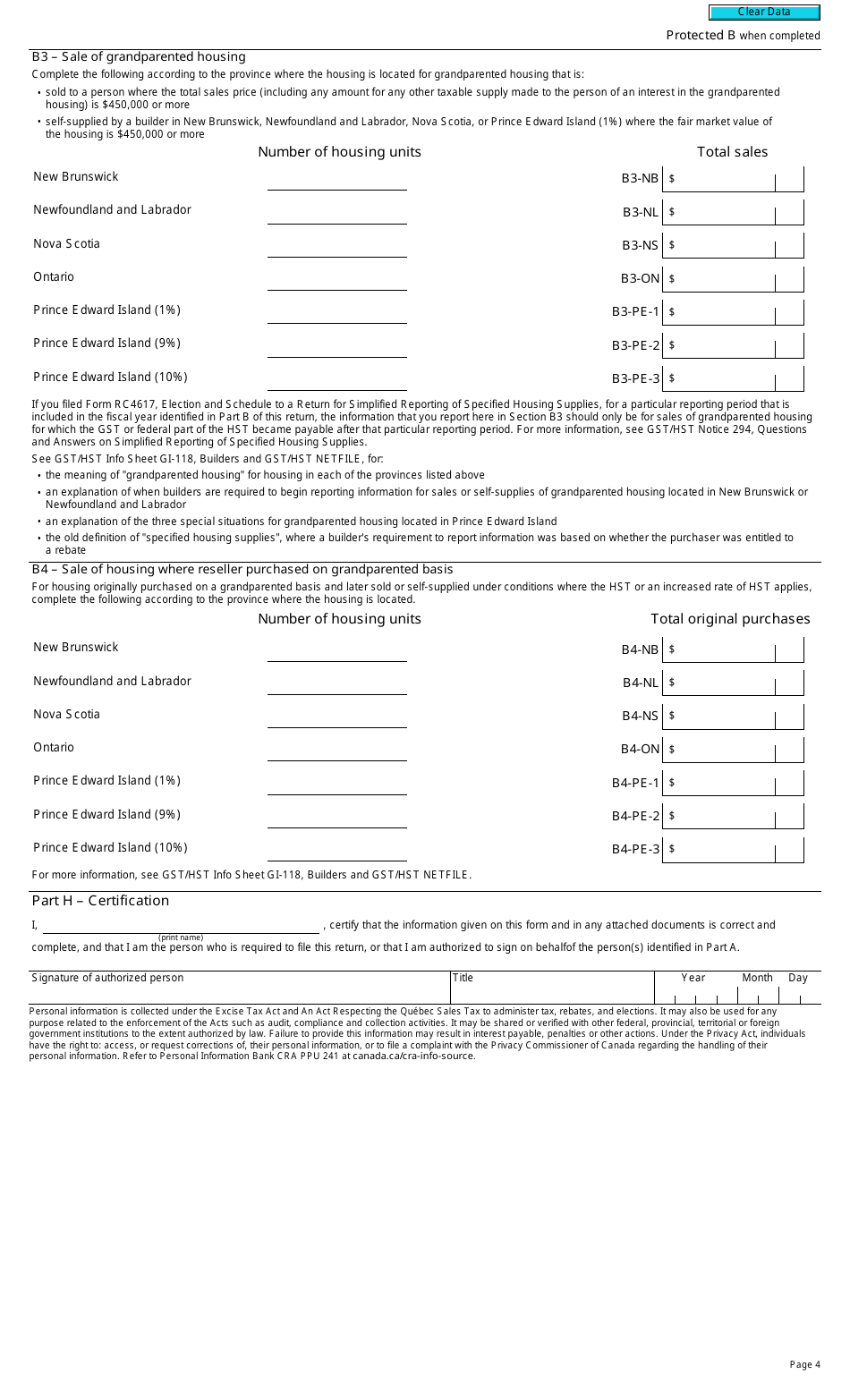

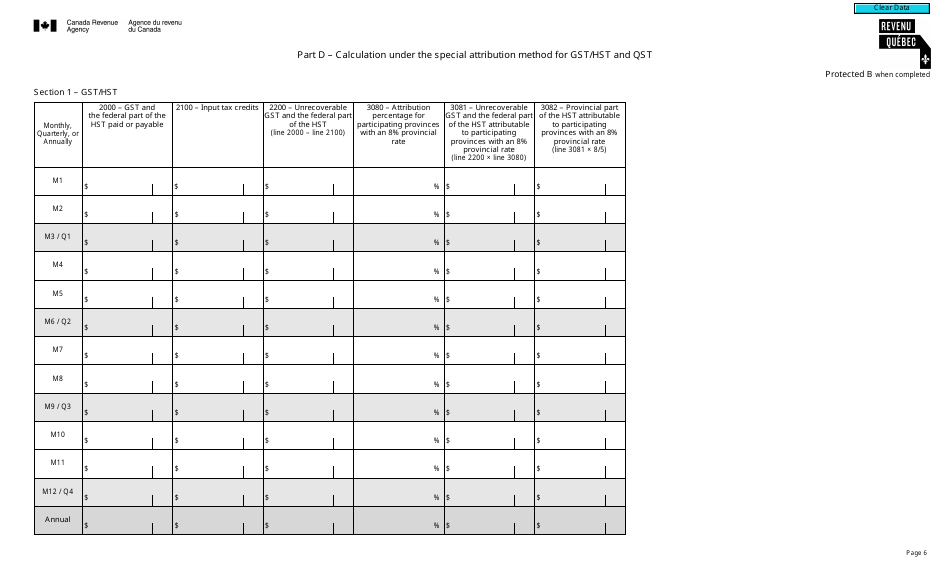

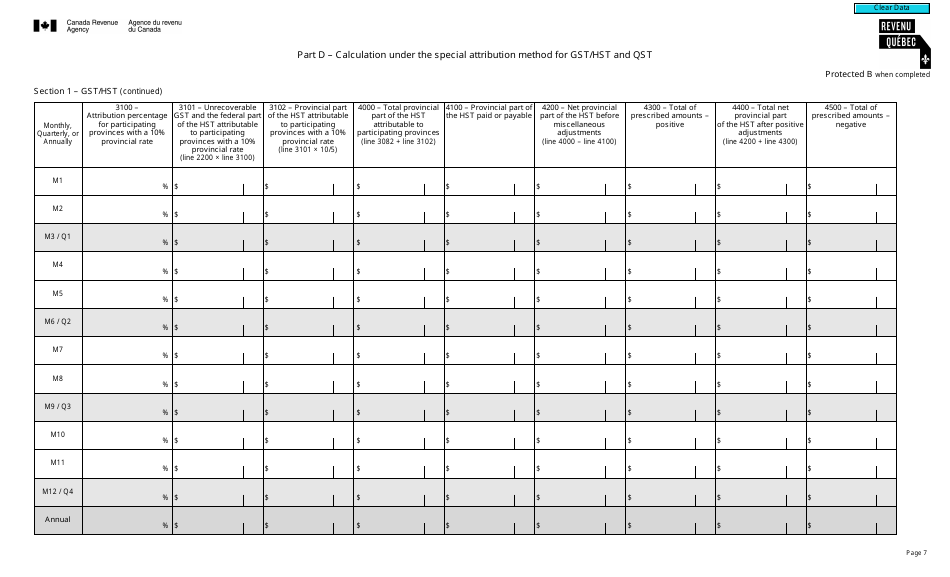

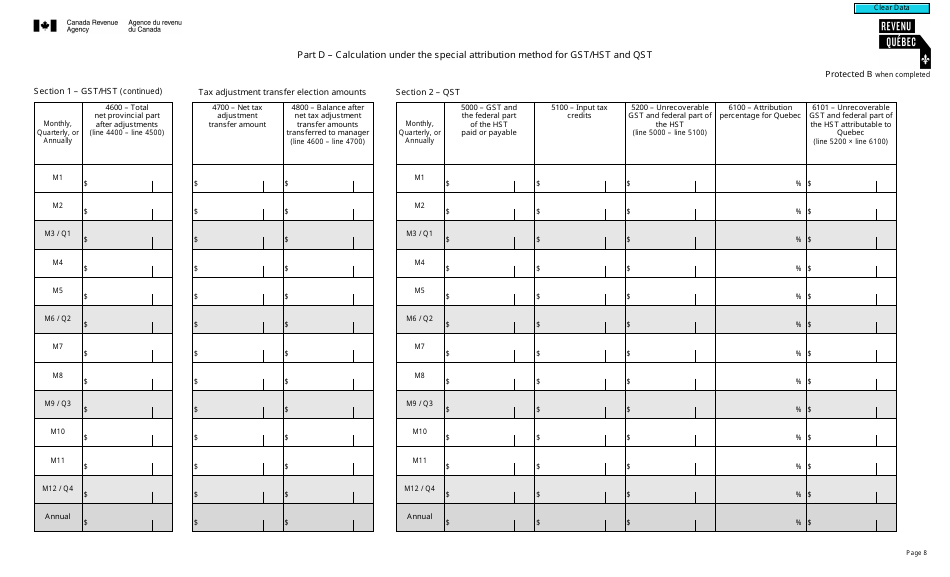

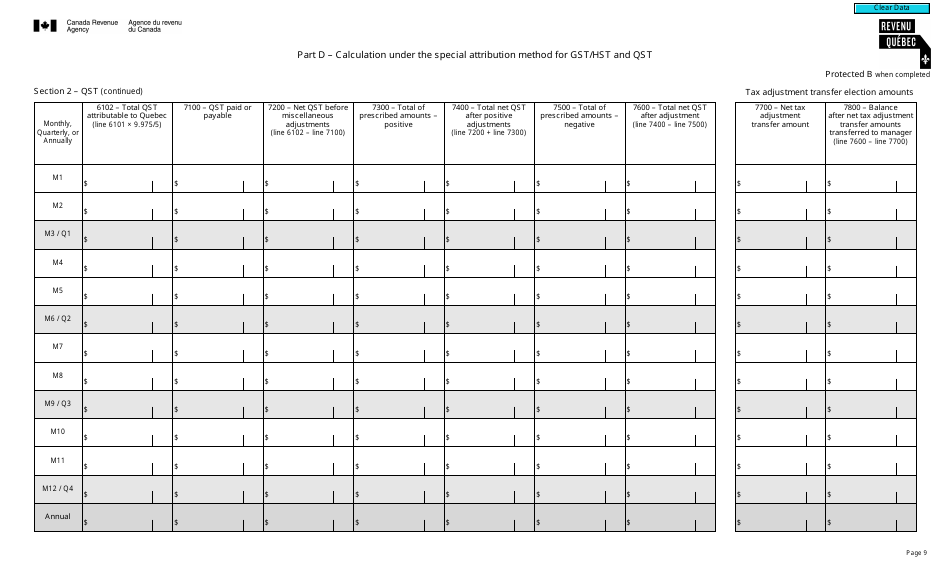

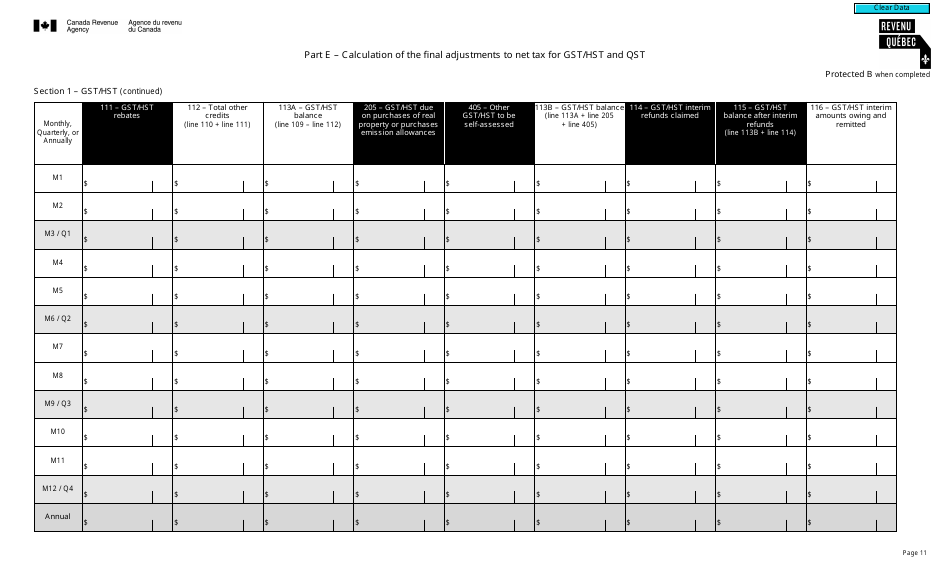

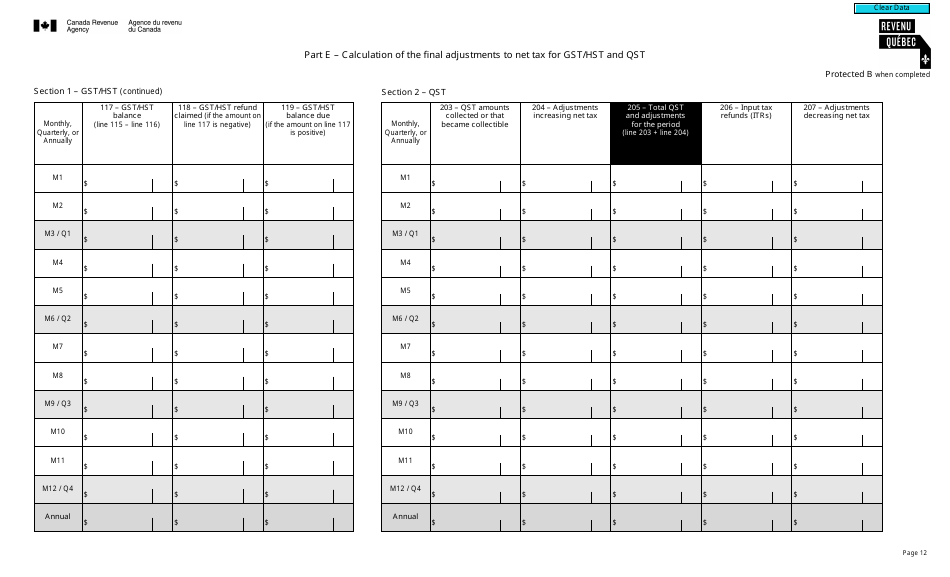

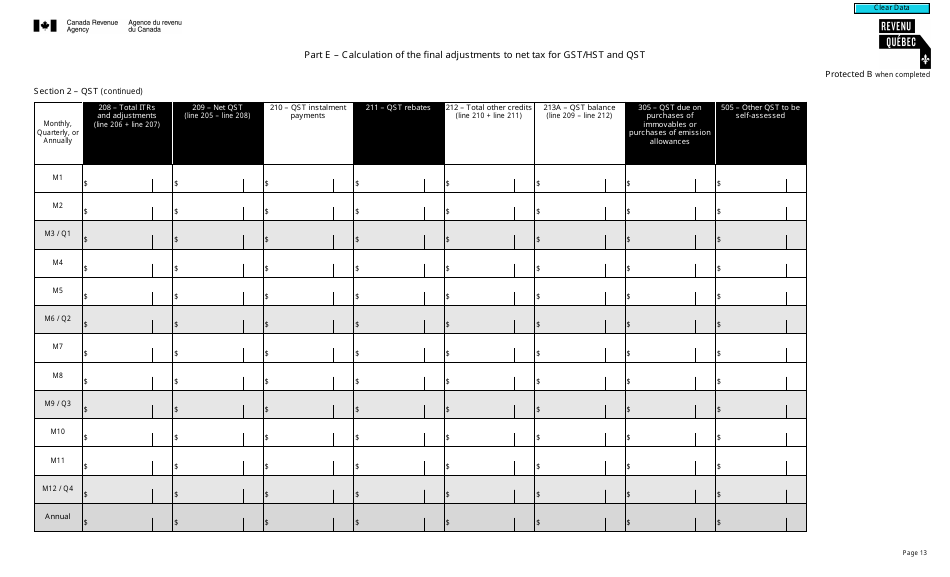

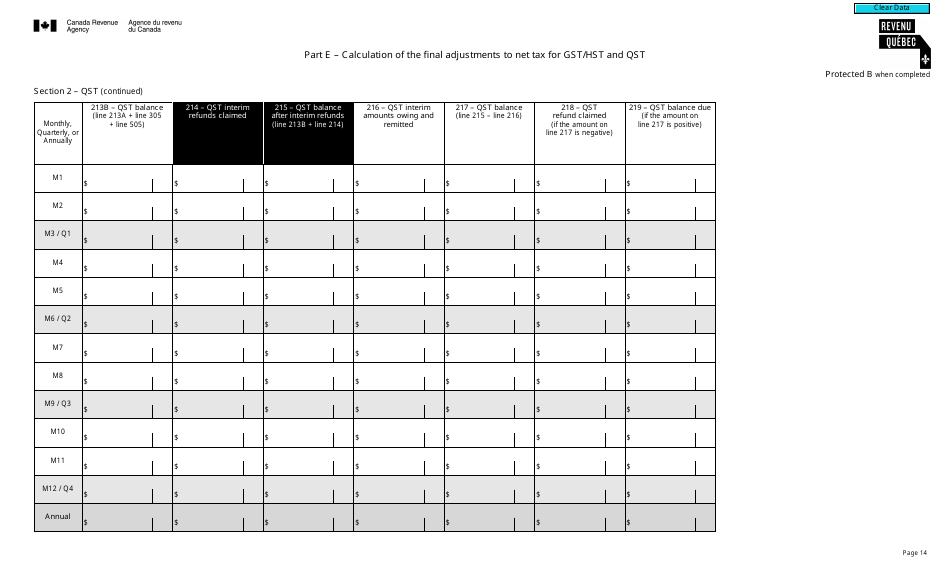

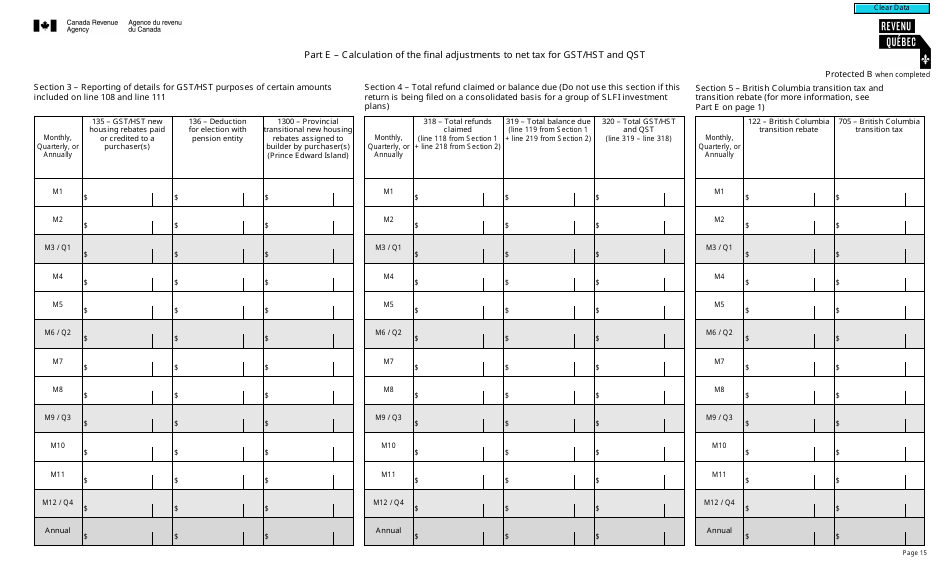

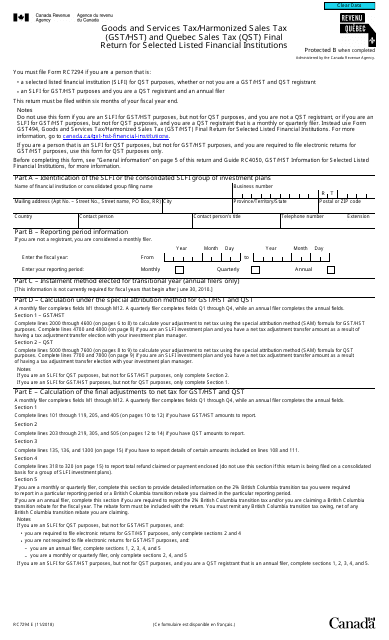

Form RC7294 Goods and Services Tax / Harmonized Sales Tax (Gst / Hst) and Quebec Sales Tax (Qst) Final Return for Selected Listed Financial Institutions - Canada

Form RC7294 is used by selected listed financial institutions in Canada to report their final Goods and Services Tax/Harmonized Sales Tax (GST/HST) and Quebec Sales Tax (QST) return. It is specifically designed for financial institutions that are required to remit the GST/HST and QST on certain supplies made by them. This form helps them to calculate and report the taxes owed to the Canada Revenue Agency (CRA) and Revenu Québec.

Financial institutions that are classified as selected listed financial institutions in Canada must file the Form RC7294 Goods and Services Tax/Harmonized Sales Tax (GST/HST) and Quebec Sales Tax (QST) Final Return.

FAQ

Q: What is Form RC7294?

A: Form RC7294 is the Final Return for Selected Listed Financial Institutions in Canada to report Goods and Services Tax/Harmonized Sales Tax (GST/HST) and Quebec Sales Tax (QST).

Q: Who needs to file Form RC7294?

A: Selected Listed Financial Institutions in Canada need to file Form RC7294 to report GST/HST and QST.

Q: What taxes are reported on Form RC7294?

A: Form RC7294 is used to report the Goods and Services Tax (GST), Harmonized Sales Tax (HST), and Quebec Sales Tax (QST).

Q: Is Form RC7294 applicable only in Quebec?

A: No, Form RC7294 is applicable to selected listed financial institutions across Canada.

Q: What is the purpose of filing Form RC7294?

A: The purpose of filing Form RC7294 is to report and remit the GST/HST and QST collected by selected listed financial institutions.

Q: Can individuals file Form RC7294?

A: No, Form RC7294 is specifically for selected listed financial institutions and not for individuals.

Q: When is Form RC7294 due?

A: The due date for filing Form RC7294 varies and depends on the specific reporting period. It is important to check the instructions or consult the Canada Revenue Agency (CRA) for the specific due date.

Q: Are there any penalties for not filing Form RC7294?

A: Yes, there may be penalties for not filing Form RC7294 or for filing it late. It is important to meet the filing requirements and deadlines set by the CRA to avoid penalties.

Download Form RC7294 Goods and Services Tax / Harmonized Sales Tax (Gst / Hst) and Quebec Sales Tax (Qst) Final Return for Selected Listed Financial Institutions - Canada

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15