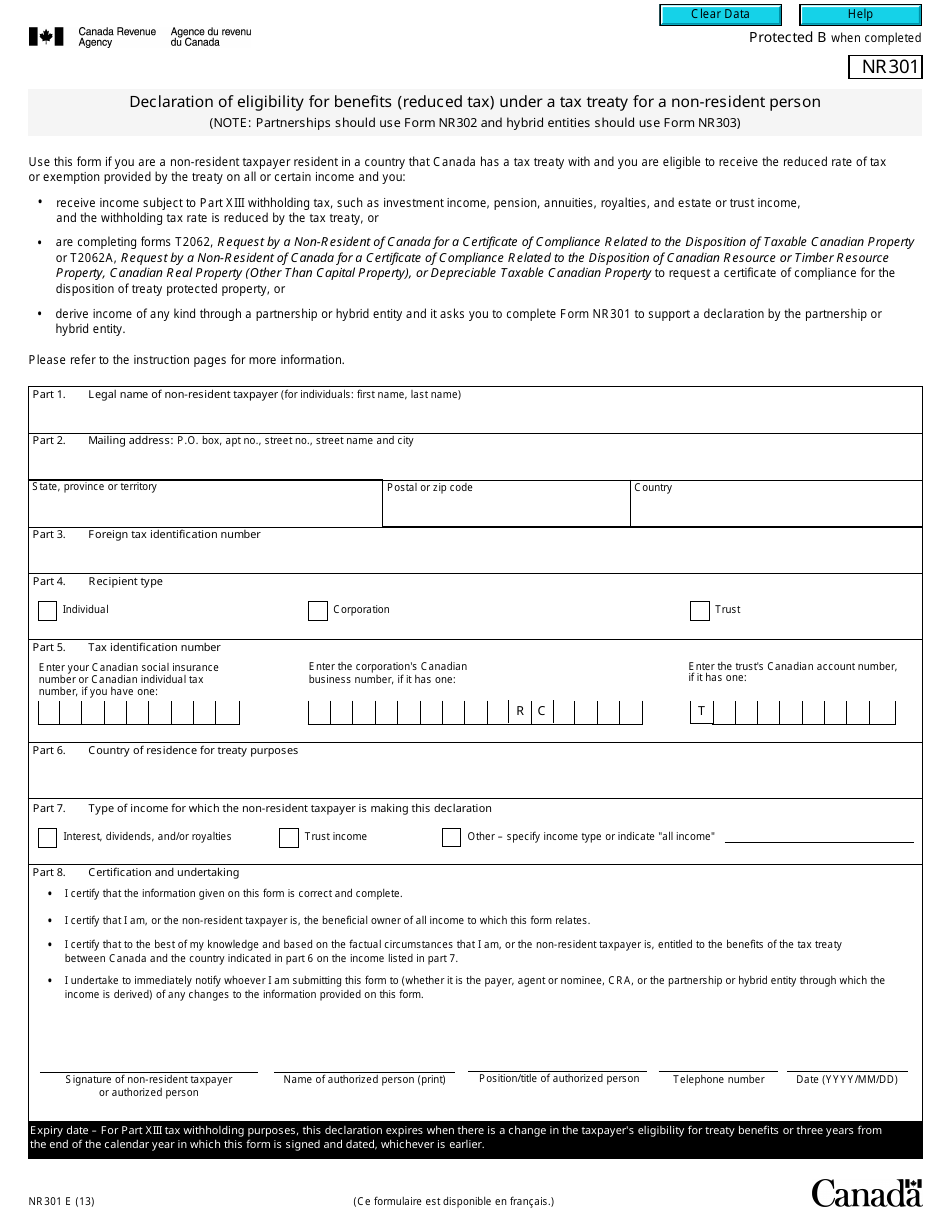

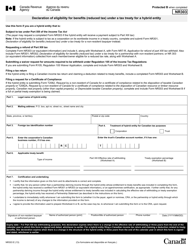

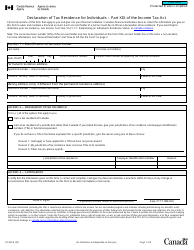

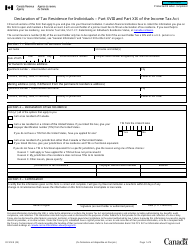

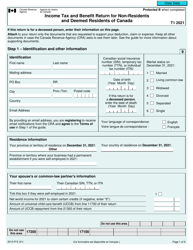

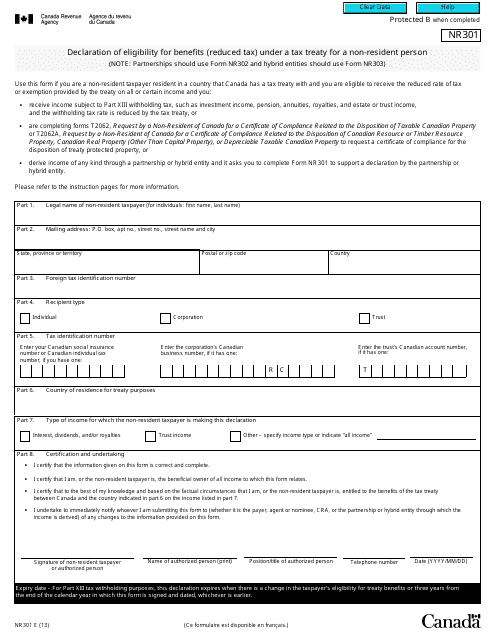

Form NR301 Declaration of Eligibility for Benefits (Reduced Tax) Under a Tax Treaty for a Non-resident Person - Canada

Form NR301, Declaration of Eligibility for Benefits (Reduced Tax) Under a Tax Treaty for a Non-resident Person, is used by a non-resident person from Canada to claim reduced tax rates or exemptions on certain types of income, such as dividends, interest, or royalties, as specified in the tax treaty between the United States and Canada.

The Form NR301 Declaration of Eligibility for Benefits (Reduced Tax) Under a Tax Treaty for a Non-resident Person - Canada is typically filed by a non-resident person from Canada who is claiming reduced tax benefits under a tax treaty.

FAQ

Q: What is the Form NR301?

A: Form NR301 is a declaration of eligibility for benefits under a tax treaty for a non-resident person from Canada.

Q: Who can use Form NR301?

A: Form NR301 is for non-resident persons from Canada who are eligible for reduced tax benefits under a tax treaty between the United States and Canada.

Q: What is the purpose of Form NR301?

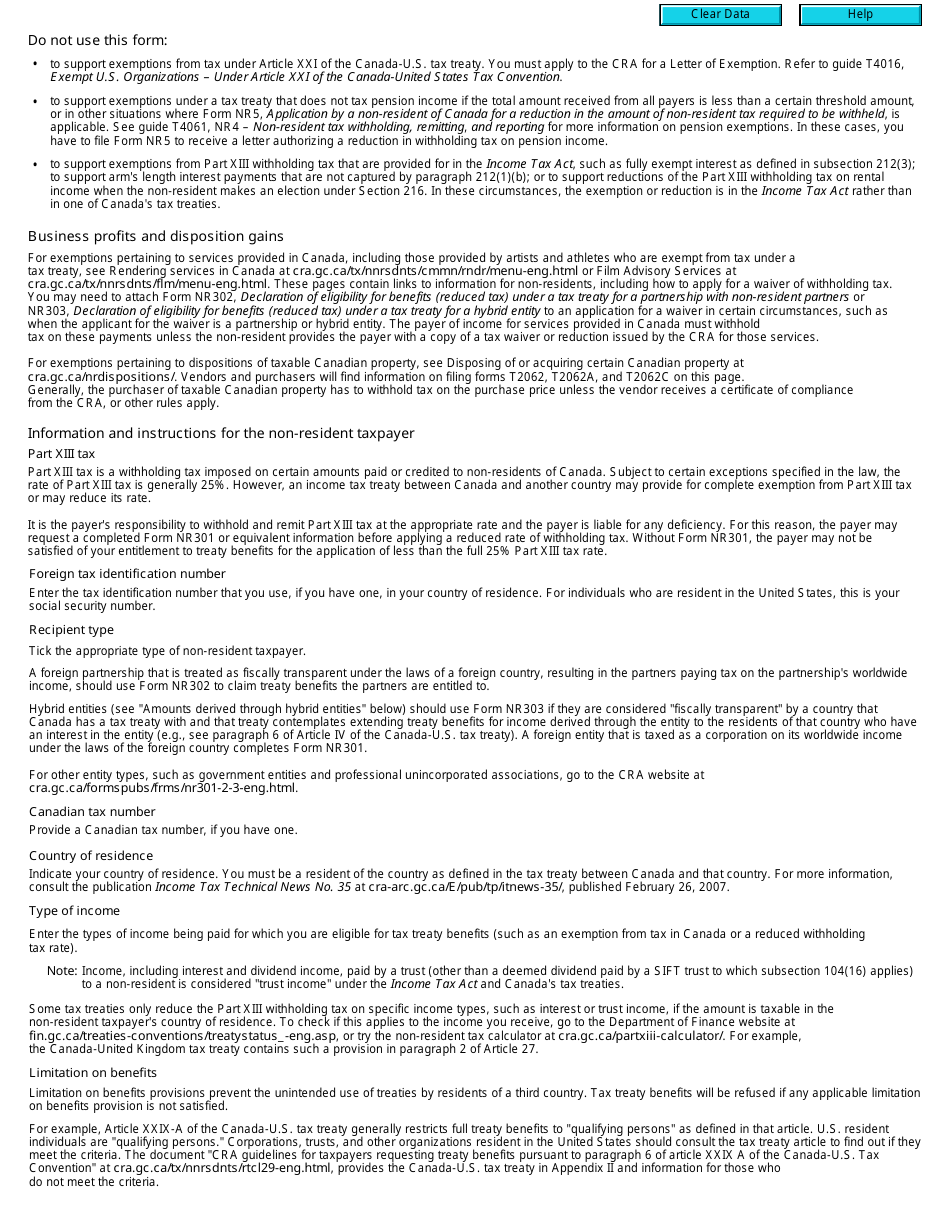

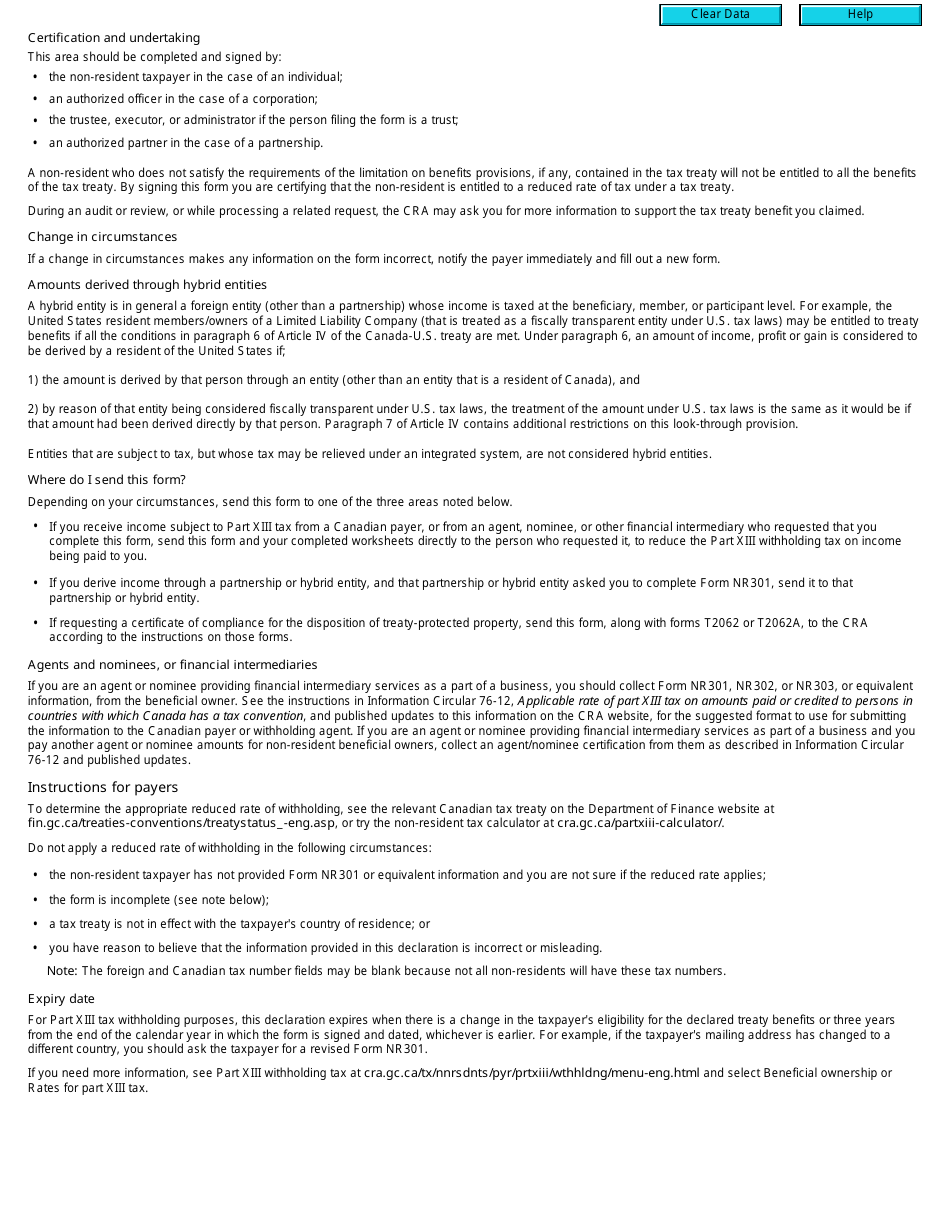

A: The purpose of Form NR301 is to declare eligibility for reduced tax benefits under a tax treaty and to claim those benefits when filing taxes in the United States.

Q: What information do I need to provide on Form NR301?

A: You will need to provide your personal information, including your name, address, and taxpayer identification number, as well as details about your eligibility for benefits under the tax treaty.

Q: When should I file Form NR301?

A: You should file Form NR301 at the time you are required to file your tax return in the United States.

Q: Are there any specific instructions for completing Form NR301?

A: Yes, there are specific instructions provided by the IRS that should be followed to complete Form NR301 accurately.

Q: What happens after I file Form NR301?

A: After you file Form NR301, the IRS will review your declaration and determine if you are eligible for the claimed benefits under the tax treaty.

Q: Can I claim both US and Canadian tax benefits?

A: No, you cannot claim both US and Canadian tax benefits under the same tax treaty.

Q: Can I use Form NR301 if I am a US resident?

A: No, Form NR301 is specifically for non-resident persons from Canada. US residents are not eligible to use this form.

Download Form NR301 Declaration of Eligibility for Benefits (Reduced Tax) Under a Tax Treaty for a Non-resident Person - Canada

1

2

3