![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form NC-BR

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form NC-BR

for the current year.

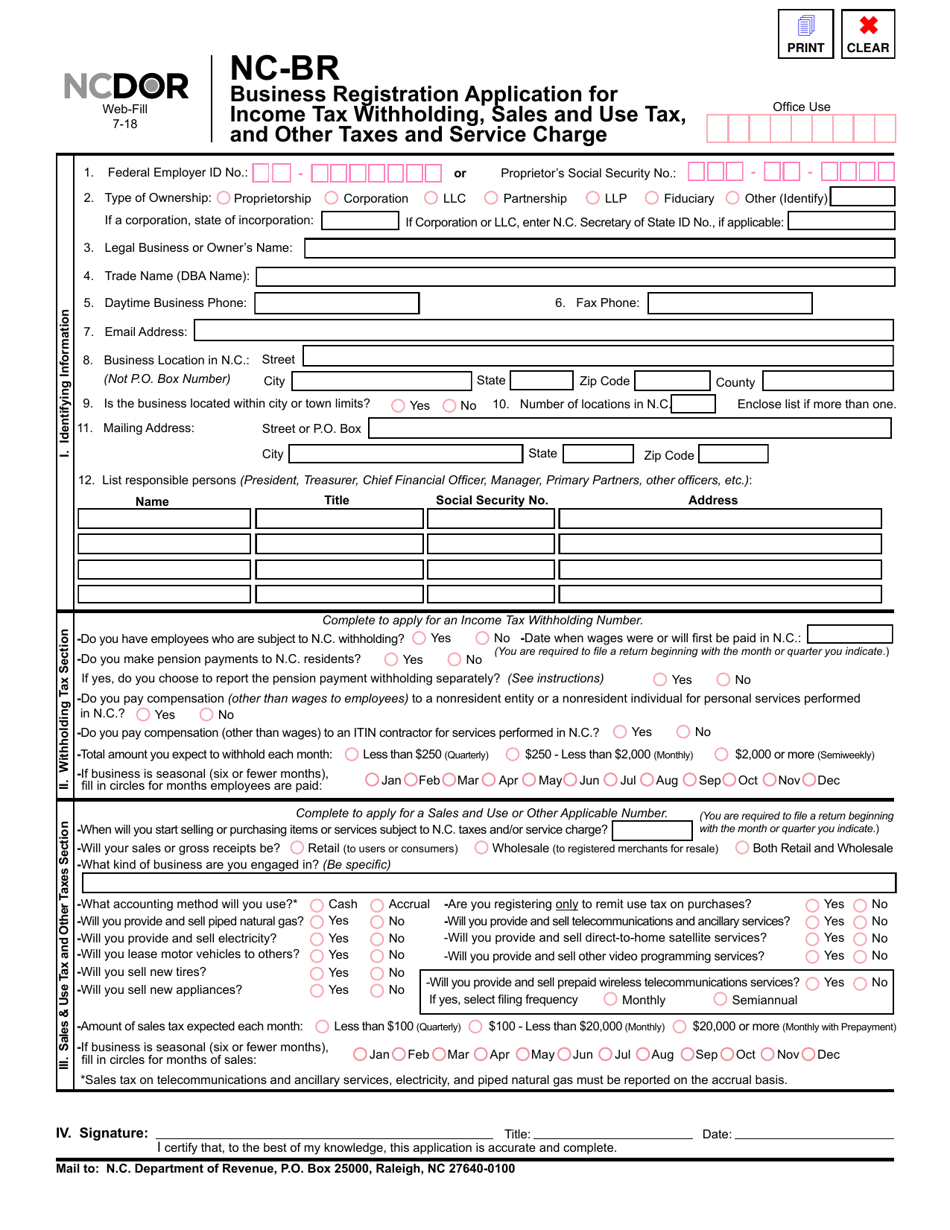

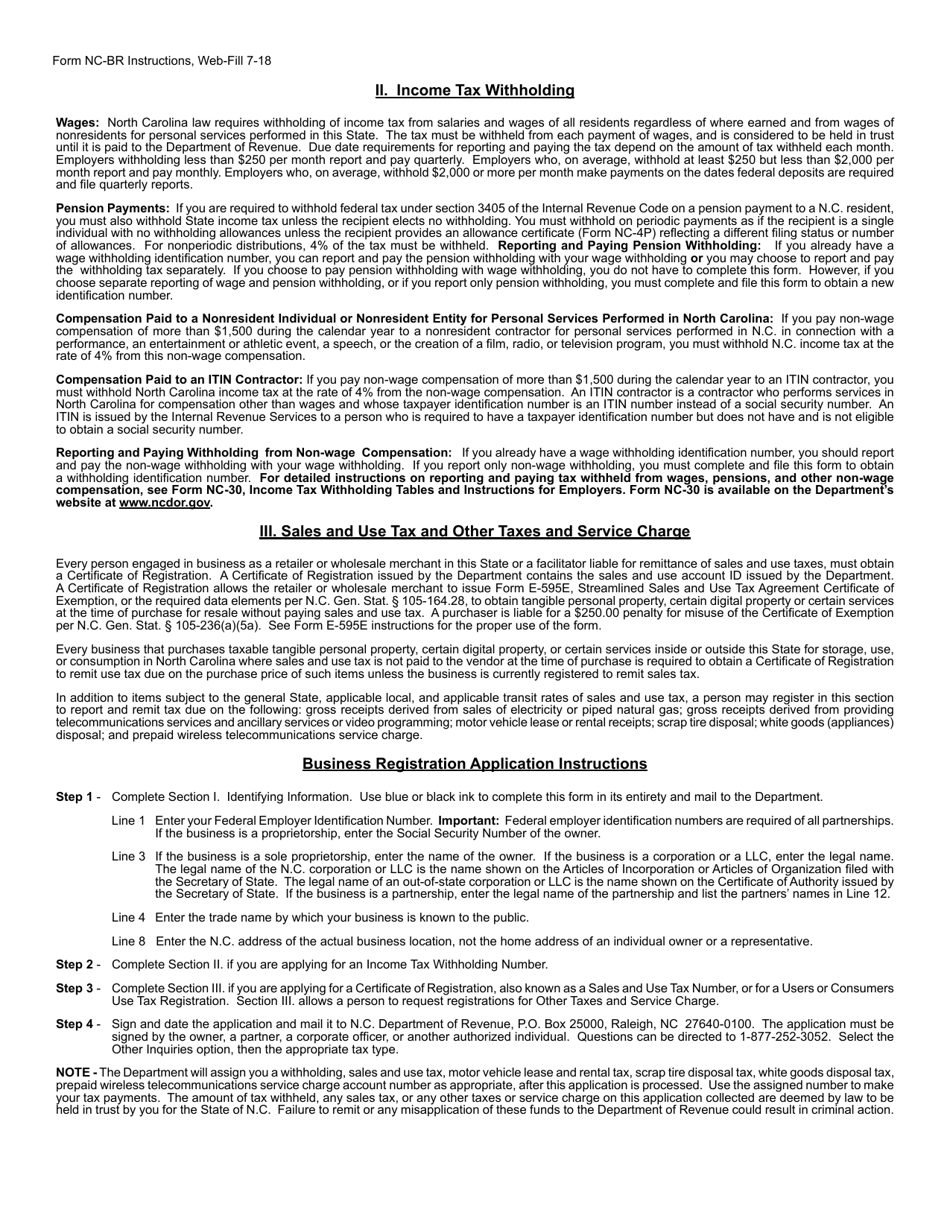

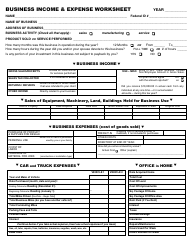

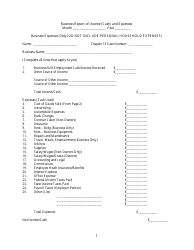

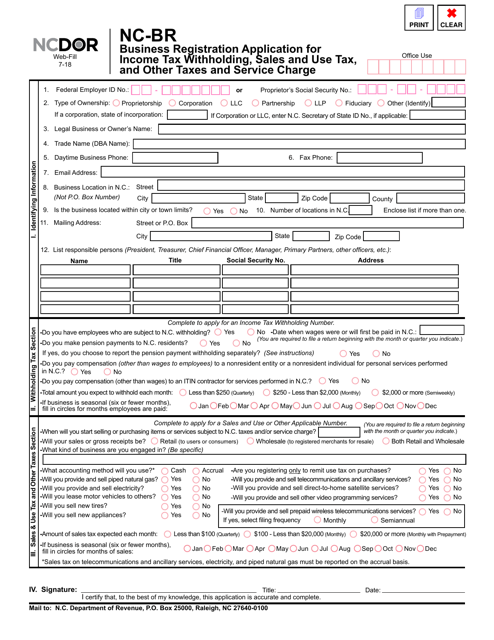

Form NC-BR Business Registration Application for Income Tax Withholding, Sales and Use Tax, and Other Taxes and Service Charge - North Carolina

What Is Form NC-BR?

This is a legal form that was released by the North Carolina Department of Revenue - a government authority operating within North Carolina. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is the NC-BR Business Registration Application?

A: The NC-BR Business Registration Application is a form used in North Carolina to register a business for income tax withholding, sales and use tax, and other taxes and service charge.

Q: What taxes and charges can be registered using the NC-BR form?

A: The NC-BR form can be used to register for income tax withholding, sales and use tax, and other taxes and service charge in North Carolina.

Q: How do I fill out the NC-BR Business Registration Application?

A: To fill out the NC-BR Business Registration Application, you need to provide information about your business, including the legal name, address, federal employer identification number (EIN), type of business, and the taxes and charges you are registering for.

Q: Is there a fee to submit the NC-BR Business Registration Application?

A: No, there is no fee to submit the NC-BR Business Registration Application.

Q: What do I need to do after submitting the NC-BR Business Registration Application?

A: After submitting the NC-BR Business Registration Application, you may need to obtain any necessary licenses or permits for your business. You should also keep a copy of the application for your records.

Form Details:

- Released on July 1, 2018;

- The latest edition provided by the North Carolina Department of Revenue;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form NC-BR by clicking the link below or browse more documents and templates provided by the North Carolina Department of Revenue.

Download Form NC-BR Business Registration Application for Income Tax Withholding, Sales and Use Tax, and Other Taxes and Service Charge - North Carolina

1

2