![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form 1041ME Schedule NR

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form 1041ME Schedule NR

for the current year.

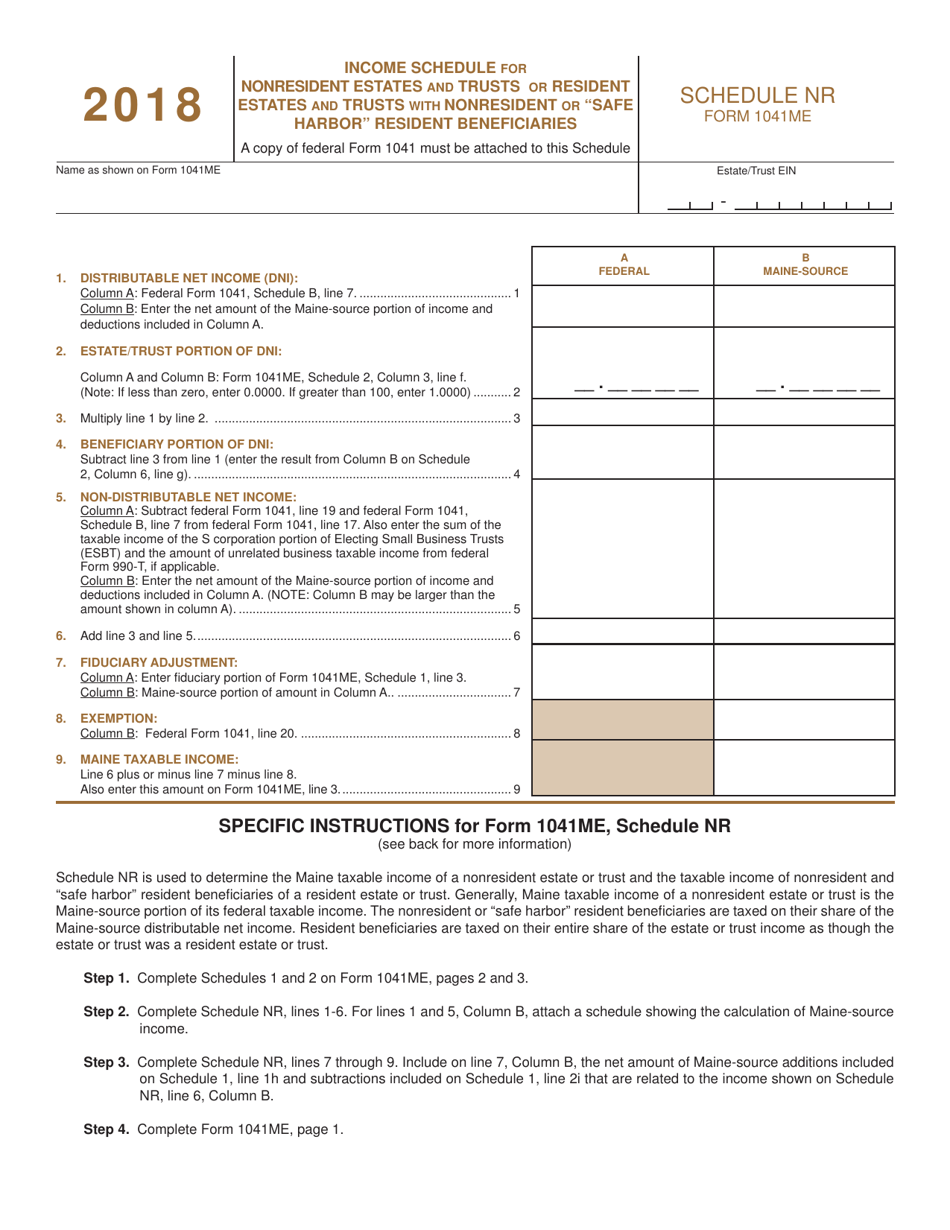

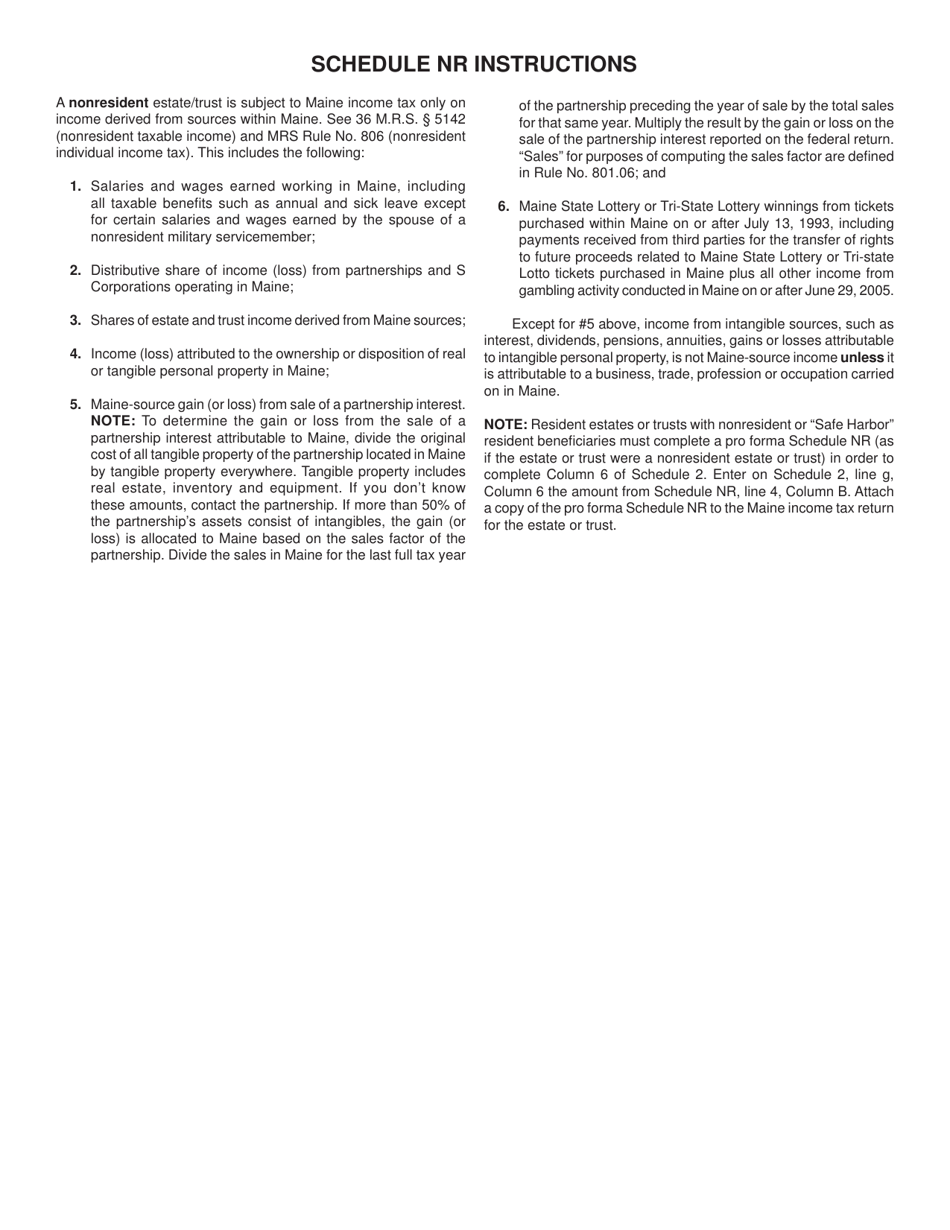

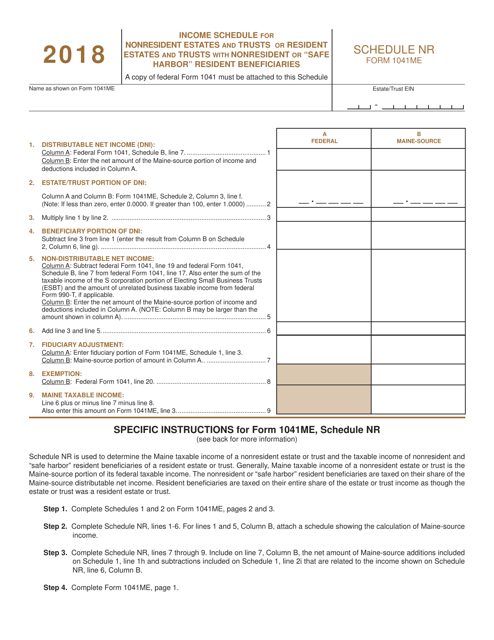

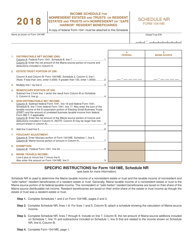

Form 1041ME Schedule NR Income Schedule for Nonresident Estates and Trusts or Resident Estates and Trusts With Nonresident or "safe Harbor" Resident Beneficiaries - Maine

What Is Form 1041ME Schedule NR?

This is a legal form that was released by the Maine Department of Administrative and Financial Services - a government authority operating within Maine.The document is a supplement to Form 1041ME, Income Tax Return for Resident and Nonresident Estates and Trusts. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form 1041ME?

A: Form 1041ME is a tax form used for reporting income for nonresident estates and trusts or resident estates and trusts with nonresident or 'safe harbor' resident beneficiaries in the state of Maine.

Q: Who needs to file Form 1041ME?

A: Form 1041ME needs to be filed by nonresident estates and trusts or resident estates and trusts with nonresident or 'safe harbor' resident beneficiaries in Maine.

Q: What is Schedule NR?

A: Schedule NR is an income schedule that is part of Form 1041ME. It is used to report income for nonresident estates and trusts or resident estates and trusts with nonresident or 'safe harbor' resident beneficiaries.

Q: What is a nonresident estate or trust?

A: A nonresident estate or trust refers to an estate or trust that is not considered a resident of Maine for tax purposes.

Q: What is a 'safe harbor' resident beneficiary?

A: A 'safe harbor' resident beneficiary refers to a beneficiary of an estate or trust who is considered a resident of Maine for tax purposes, even if they do not physically reside in the state.

Q: Why do nonresident estates and trusts need to file Form 1041ME?

A: Nonresident estates and trusts need to file Form 1041ME to report their income from Maine sources and determine any tax liability in the state.

Q: What types of income should be reported on Schedule NR?

A: Schedule NR should be used to report income from Maine sources, such as rental income from Maine property or income from Maine businesses.

Q: Is there a deadline for filing Form 1041ME?

A: Yes, the deadline for filing Form 1041ME is generally April 15th, or the 15th day of the 4th month following the close of the tax year for estates and trusts that use the calendar year as their tax year.

Q: Do nonresident estates and trusts have to pay tax in Maine?

A: Yes, nonresident estates and trusts may have to pay tax in Maine if they have income from Maine sources and meet certain filing requirements.

Form Details:

- The latest edition provided by the Maine Department of Administrative and Financial Services;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of Form 1041ME Schedule NR by clicking the link below or browse more documents and templates provided by the Maine Department of Administrative and Financial Services.

Download Form 1041ME Schedule NR Income Schedule for Nonresident Estates and Trusts or Resident Estates and Trusts With Nonresident or "safe Harbor" Resident Beneficiaries - Maine

1

2