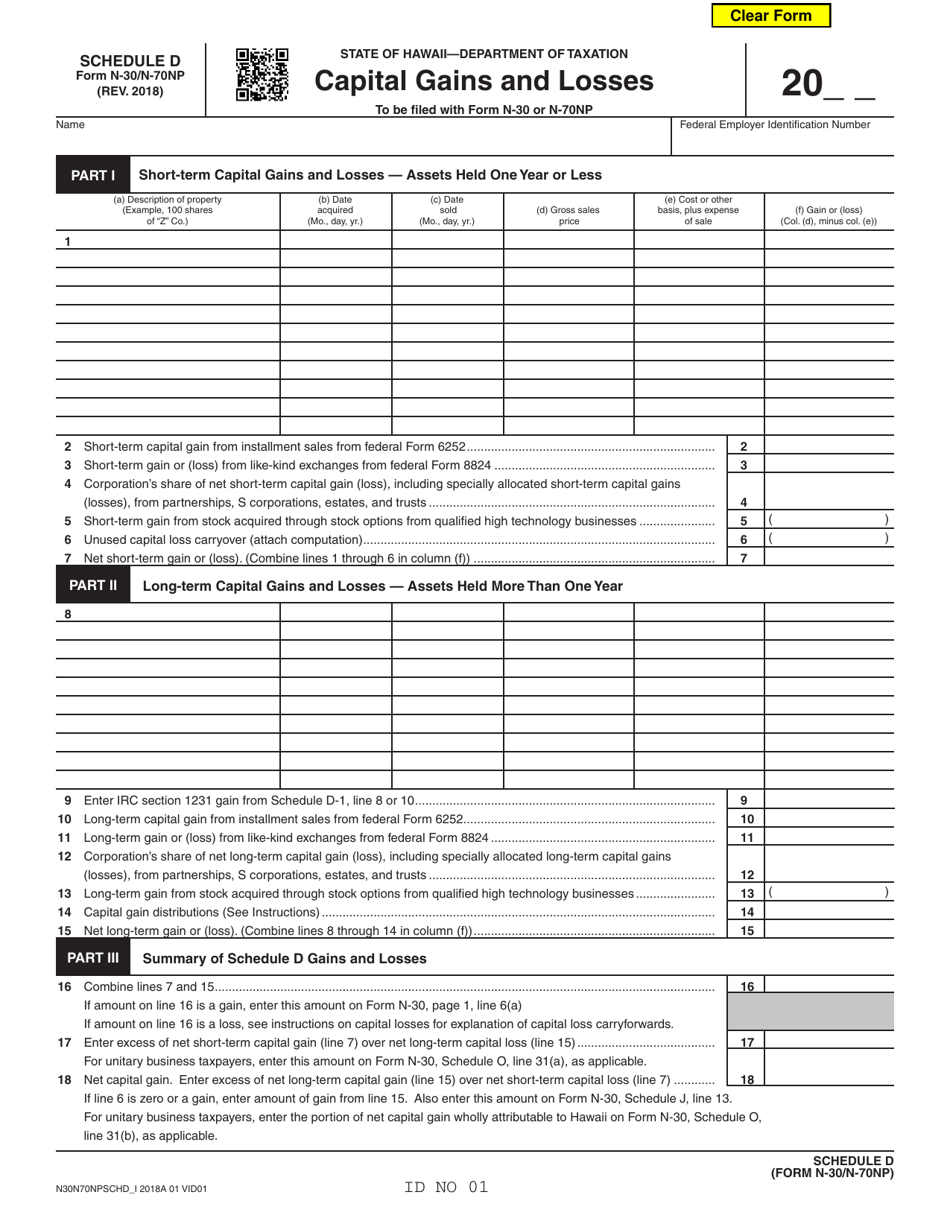

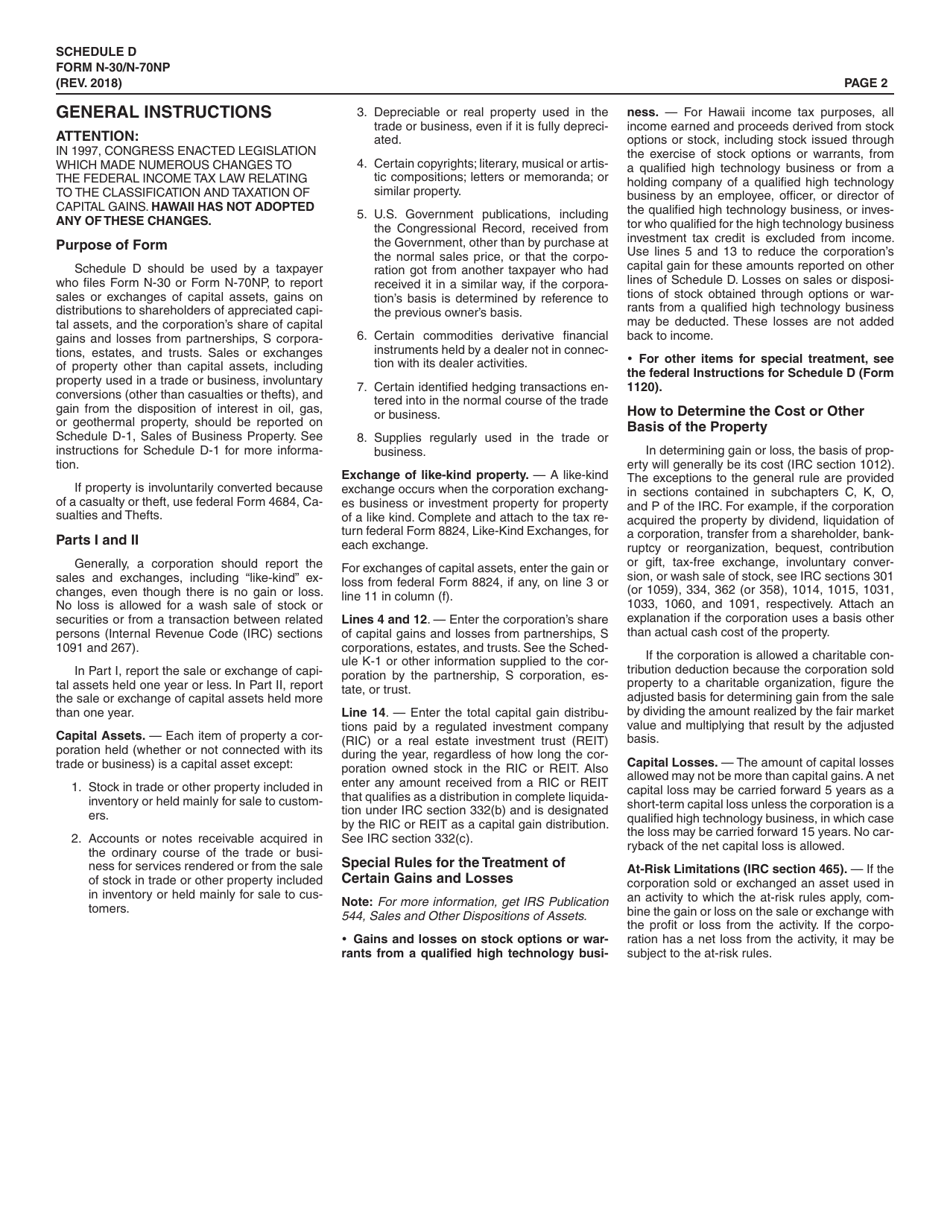

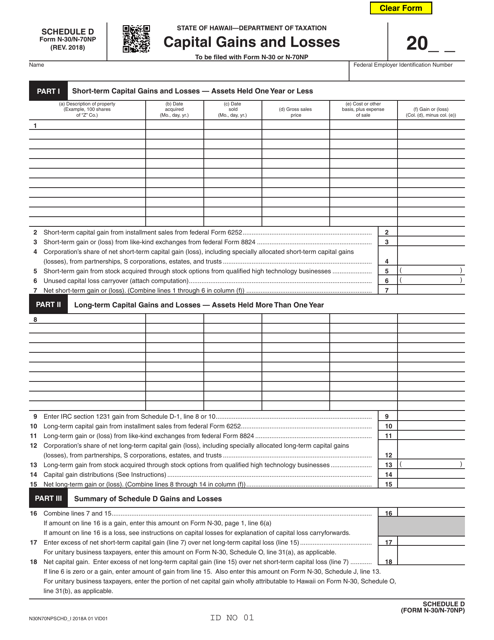

Form N-30 (N-70NP) Schedule D Capital Gains and Losses - Hawaii

What Is Form N-30 (N-70NP) Schedule D?

This is a legal form that was released by the Hawaii Department of Taxation - a government authority operating within Hawaii. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form N-30 (N-70NP)?

A: Form N-30 (N-70NP) is a tax form used in Hawaii to report capital gains and losses.

Q: What is Schedule D?

A: Schedule D is a part of Form N-30 (N-70NP) used to report capital gains and losses.

Q: What are capital gains?

A: Capital gains are profits from the sale of assets such as stocks, bonds, or real estate.

Q: What are capital losses?

A: Capital losses are losses incurred from the sale of assets such as stocks, bonds, or real estate.

Q: Why do I need to report capital gains and losses?

A: You need to report capital gains and losses on your tax return to determine if you owe taxes or are eligible for any deductions or credits.

Q: Is Form N-30 (N-70NP) specific to Hawaii?

A: Yes, Form N-30 (N-70NP) is specific to Hawaii and is used to report Hawaii state taxes.

Q: When is the deadline to file Form N-30 (N-70NP)?

A: The deadline to file Form N-30 (N-70NP) varies and is usually due on April 20th or the 20th day of the 4th month following the close of the tax year.

Q: Do I need to file Form N-30 (N-70NP) if I didn't have any capital gains or losses?

A: If you did not have any capital gains or losses during the tax year, you may not need to file Form N-30 (N-70NP), but it is always recommended to consult with a tax professional or refer to the instructions for the form.

Form Details:

- Released on January 1, 2018;

- The latest edition provided by the Hawaii Department of Taxation;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form N-30 (N-70NP) Schedule D by clicking the link below or browse more documents and templates provided by the Hawaii Department of Taxation.

Download Form N-30 (N-70NP) Schedule D Capital Gains and Losses - Hawaii

1

2