![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form 502V

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form 502V

for the current year.

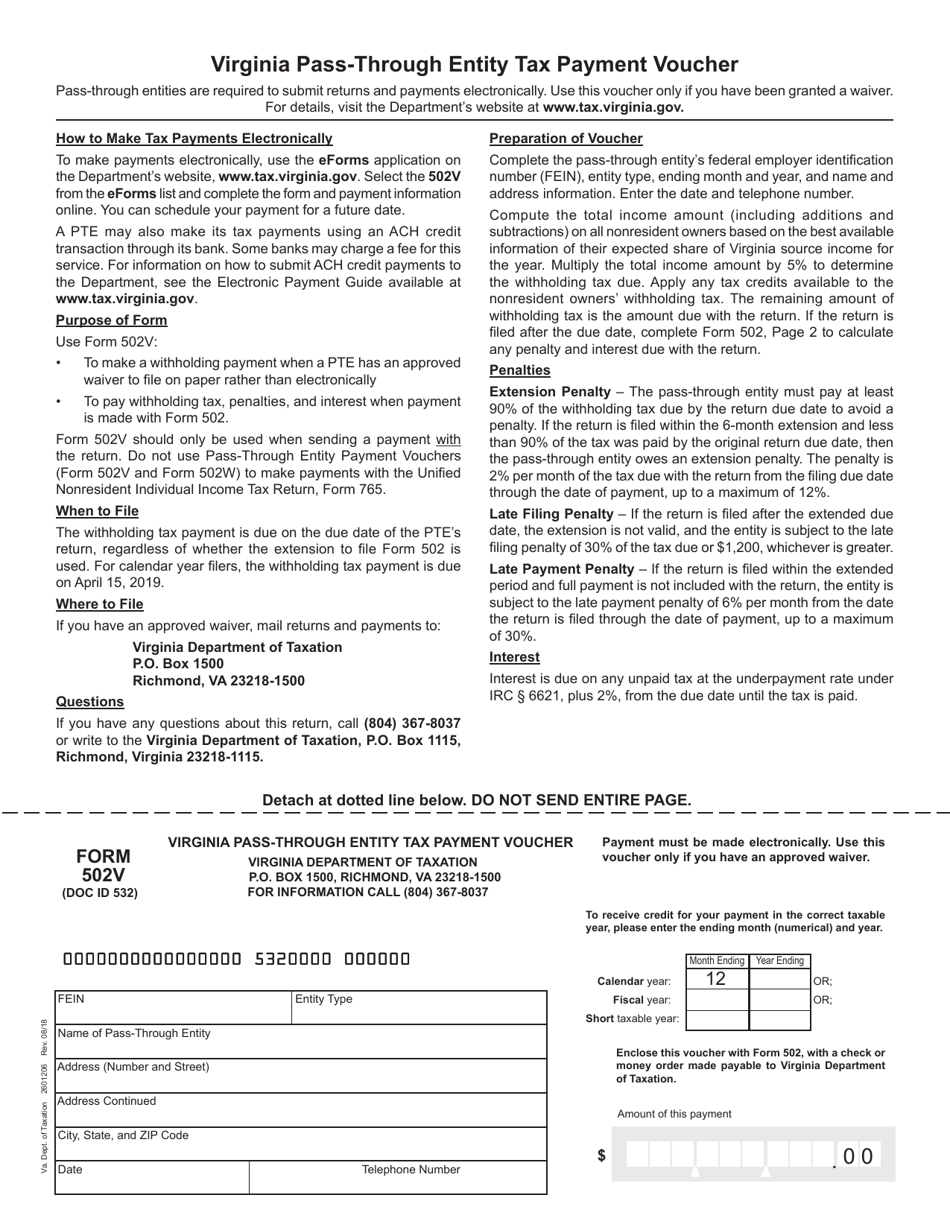

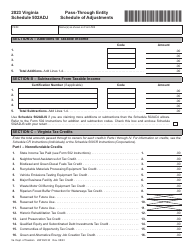

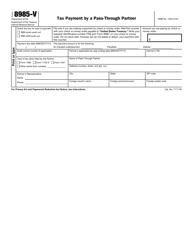

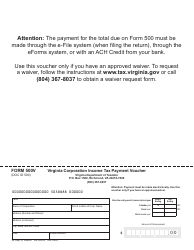

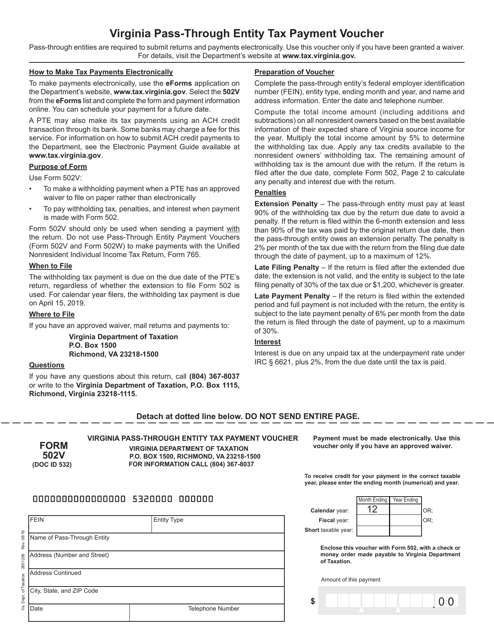

Form 502V Virginia Pass-Through Entity Tax Payment Voucher - Virginia

What Is Form 502V?

This is a legal form that was released by the Virginia Department of Taxation - a government authority operating within Virginia. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is the Form 502V?

A: Form 502V is the Virginia Pass-Through Entity Tax Payment Voucher.

Q: What is a pass-through entity?

A: A pass-through entity is a business structure that passes its income, deductions, and tax credits through to its owners for reporting on their individual tax returns.

Q: Who needs to use Form 502V?

A: Pass-through entities in Virginia need to use Form 502V to make tax payments.

Q: What is the purpose of Form 502V?

A: The purpose of Form 502V is to provide a voucher for pass-through entities to make tax payments to the Virginia Department of Taxation.

Q: When is Form 502V due?

A: Form 502V is generally due on or before the 15th day of the 4th month following the end of the pass-through entity's tax year.

Q: Are there any penalties for late payment?

A: Yes, there may be penalties for late payment of pass-through entity taxes in Virginia.

Q: What payment methods are accepted for Form 502V?

A: Payments for Form 502V can be made by electronic funds transfer (EFT), credit card, check, or money order.

Q: Is there a minimum tax payment requirement?

A: Yes, pass-through entities in Virginia must make a minimum tax payment of $100 with Form 502V.

Form Details:

- Released on August 1, 2018;

- The latest edition provided by the Virginia Department of Taxation;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form 502V by clicking the link below or browse more documents and templates provided by the Virginia Department of Taxation.