![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form 502W

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form 502W

for the current year.

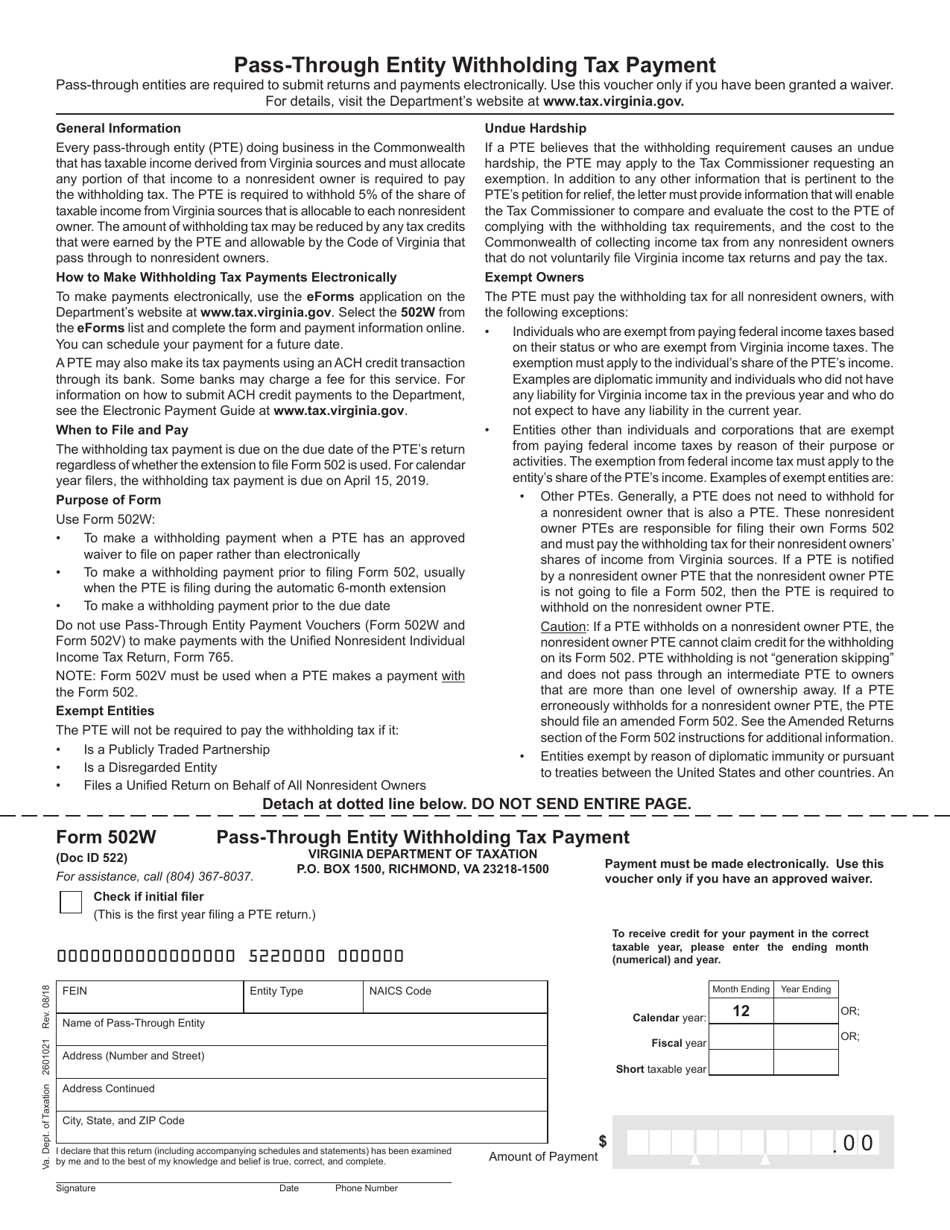

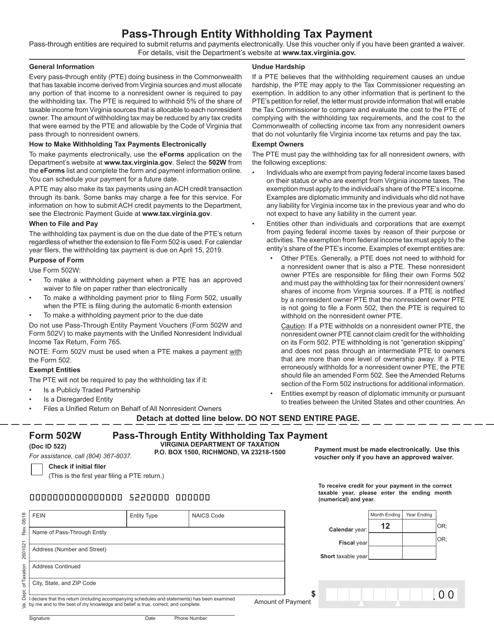

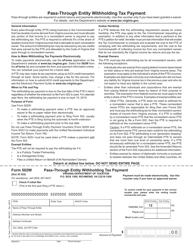

Form 502W Pass-Through Entity Withholding Tax Payment - Virginia

What Is Form 502W?

This is a legal form that was released by the Virginia Department of Taxation - a government authority operating within Virginia. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form 502W?

A: Form 502W is the Pass-Through Entity Withholding Tax Payment form in Virginia.

Q: What is the purpose of Form 502W?

A: Form 502W is used to remit withholding tax payments for pass-through entities (such as partnerships and S corporations) in Virginia.

Q: Who needs to file Form 502W?

A: Pass-through entities that have an obligation to withhold and remit taxes on behalf of their nonresident owners or members need to file Form 502W.

Q: How often should Form 502W be filed?

A: Form 502W should be filed quarterly, on or before the last day of the month following the end of each calendar quarter.

Q: What information is required on Form 502W?

A: Form 502W requires information about the pass-through entity, the amount of tax withheld, and the names and addresses of the nonresident owners or members.

Q: Are there any penalties for late or incorrect filing of Form 502W?

A: Yes, late or incorrect filing of Form 502W may result in penalties imposed by the Virginia Department of Taxation.

Form Details:

- Released on August 1, 2018;

- The latest edition provided by the Virginia Department of Taxation;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form 502W by clicking the link below or browse more documents and templates provided by the Virginia Department of Taxation.

Download Form 502W Pass-Through Entity Withholding Tax Payment - Virginia

1

2