![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form ST-3

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form ST-3

for the current year.

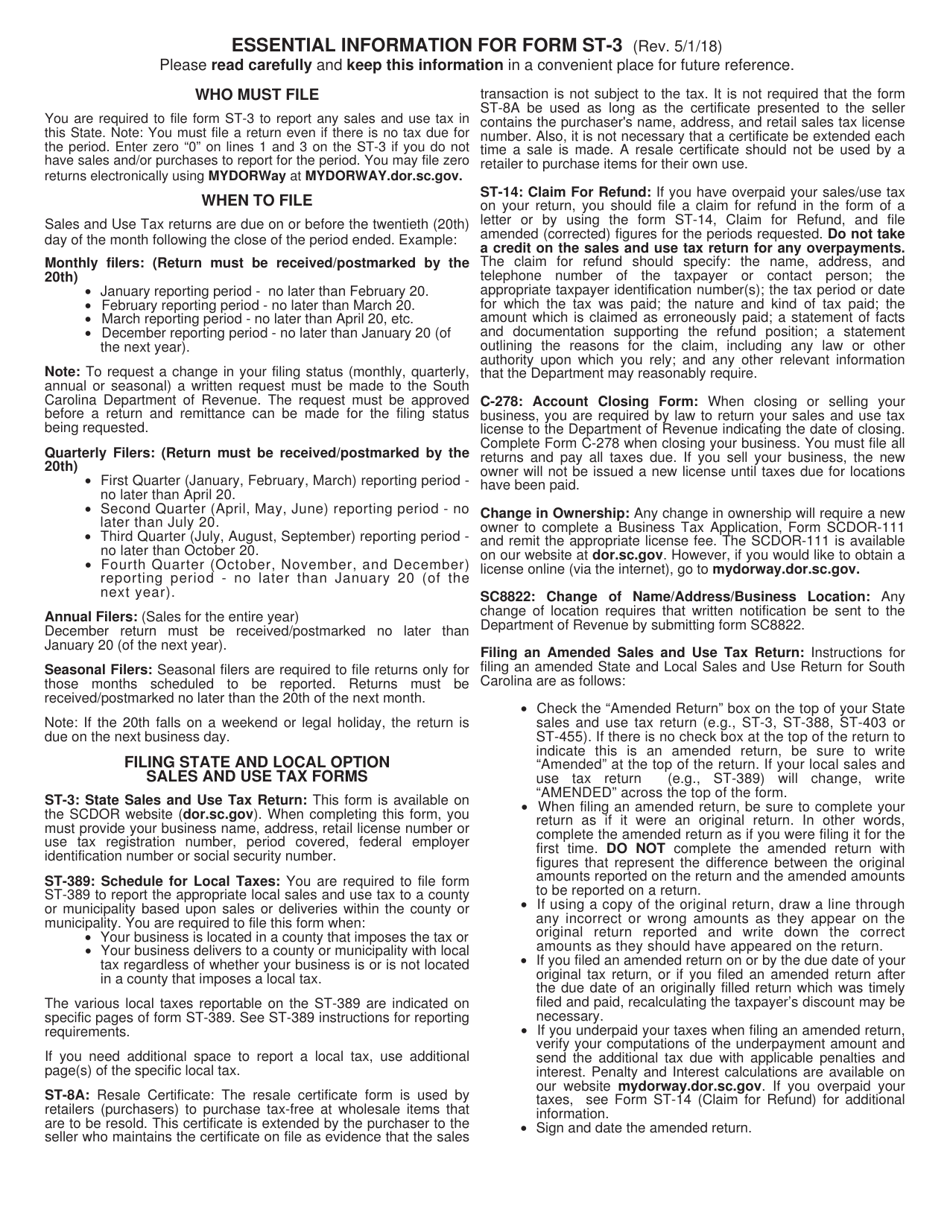

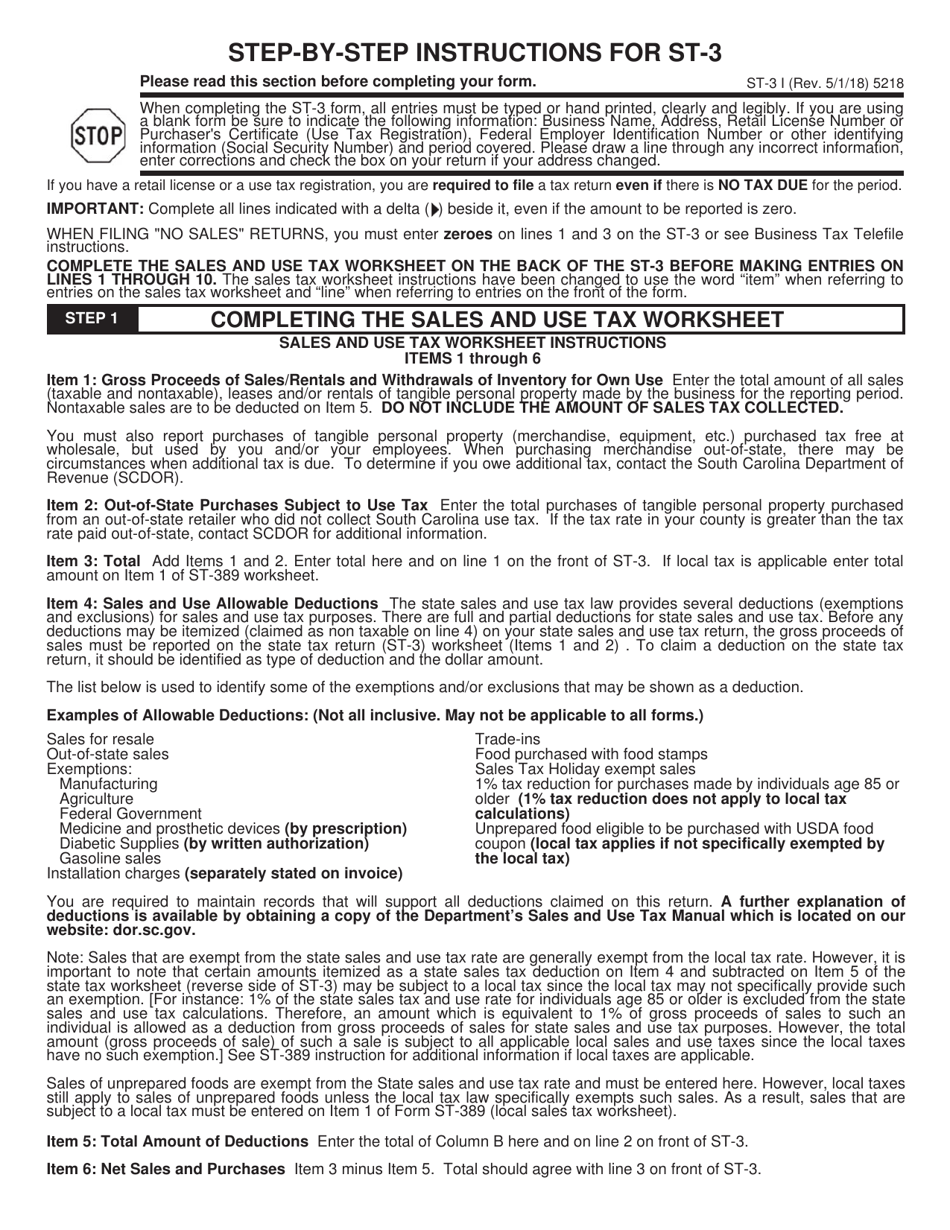

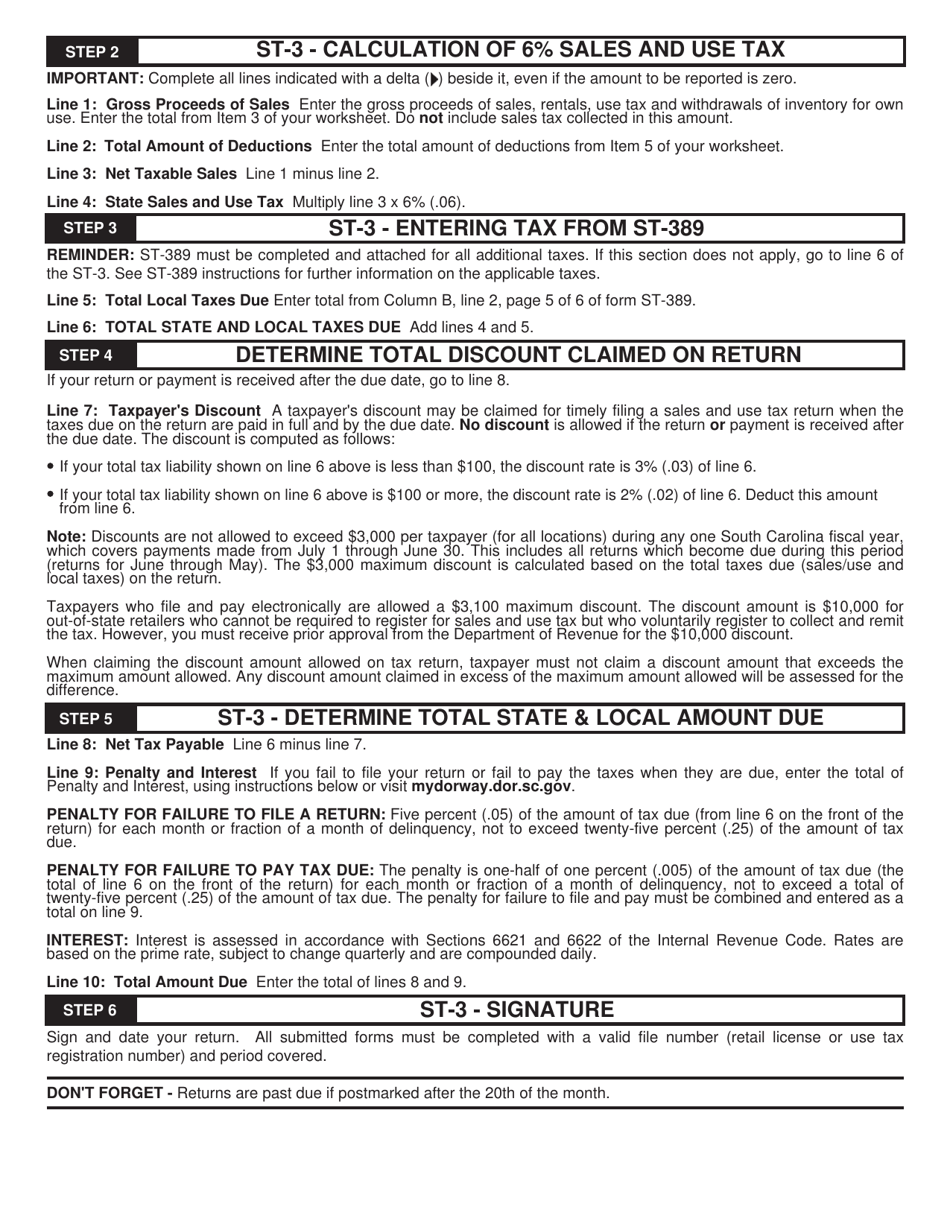

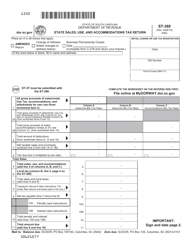

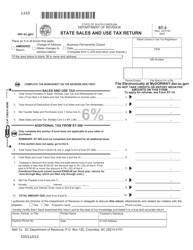

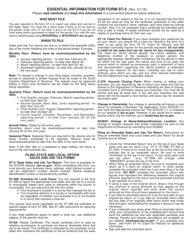

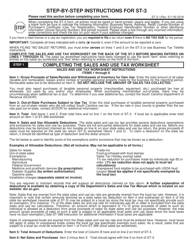

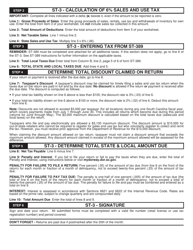

Instructions for Form ST-3 State Sales and Use Tax Return - South Carolina

This document contains official instructions for Form ST-3 , State Sales and Use Tax Return - a form released and collected by the South Carolina Department of Revenue. An up-to-date fillable Form ST-3 is available for download through this link.

FAQ

Q: What is Form ST-3?

A: Form ST-3 is the State Sales and Use Tax Return for South Carolina.

Q: Who needs to file Form ST-3?

A: Any business or individual who collects sales and use tax in South Carolina needs to file Form ST-3.

Q: When is Form ST-3 due?

A: Form ST-3 is generally due on or before the 20th day of the month following the reporting period.

Q: What information do I need to complete Form ST-3?

A: You will need information about your sales and use tax collections, exemptions, and deductions for the reporting period.

Q: Are there any penalties for not filing Form ST-3?

A: Yes, failing to file Form ST-3 or paying the sales and use tax owed on time can result in penalties and interest.

Instruction Details:

- This 3-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the South Carolina Department of Revenue.

1

2

3