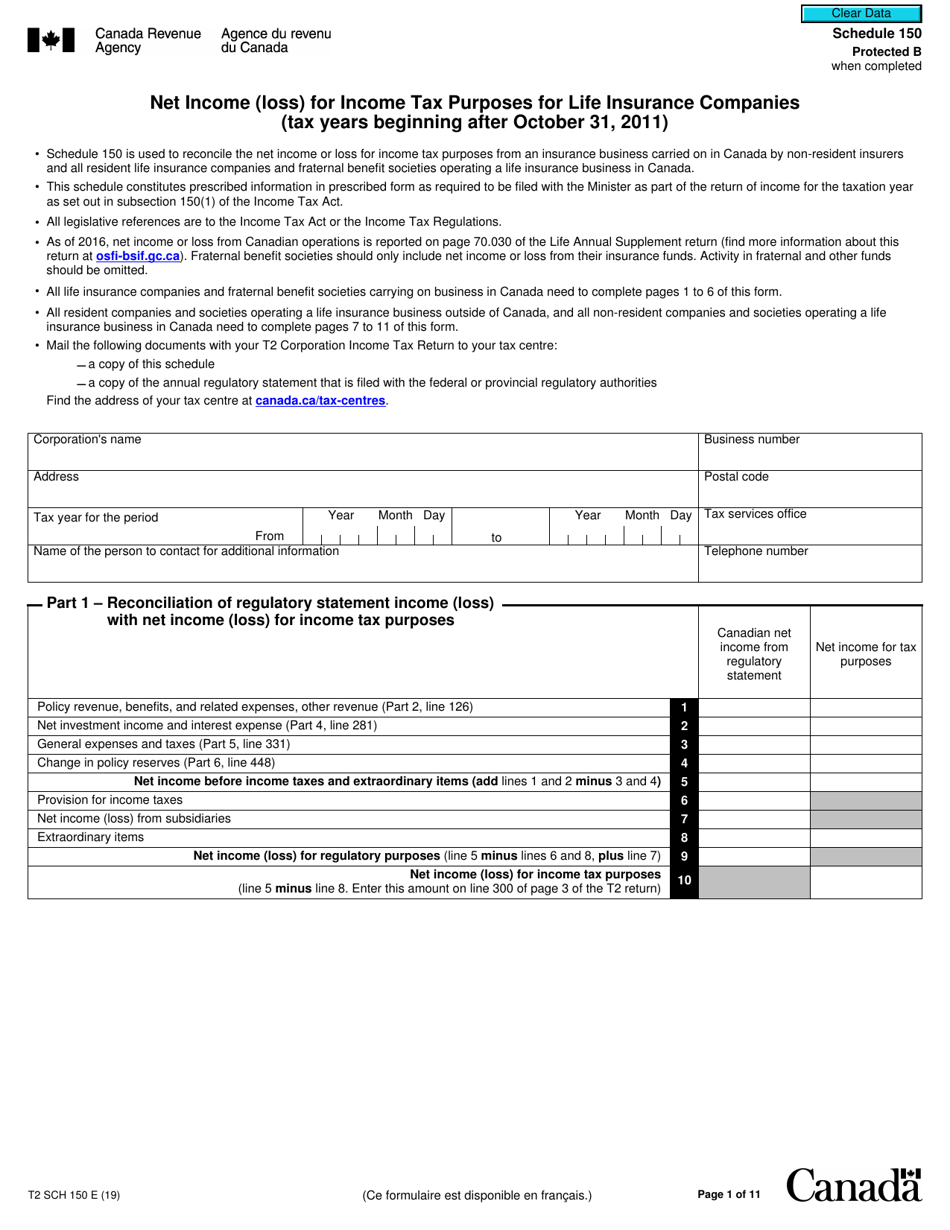

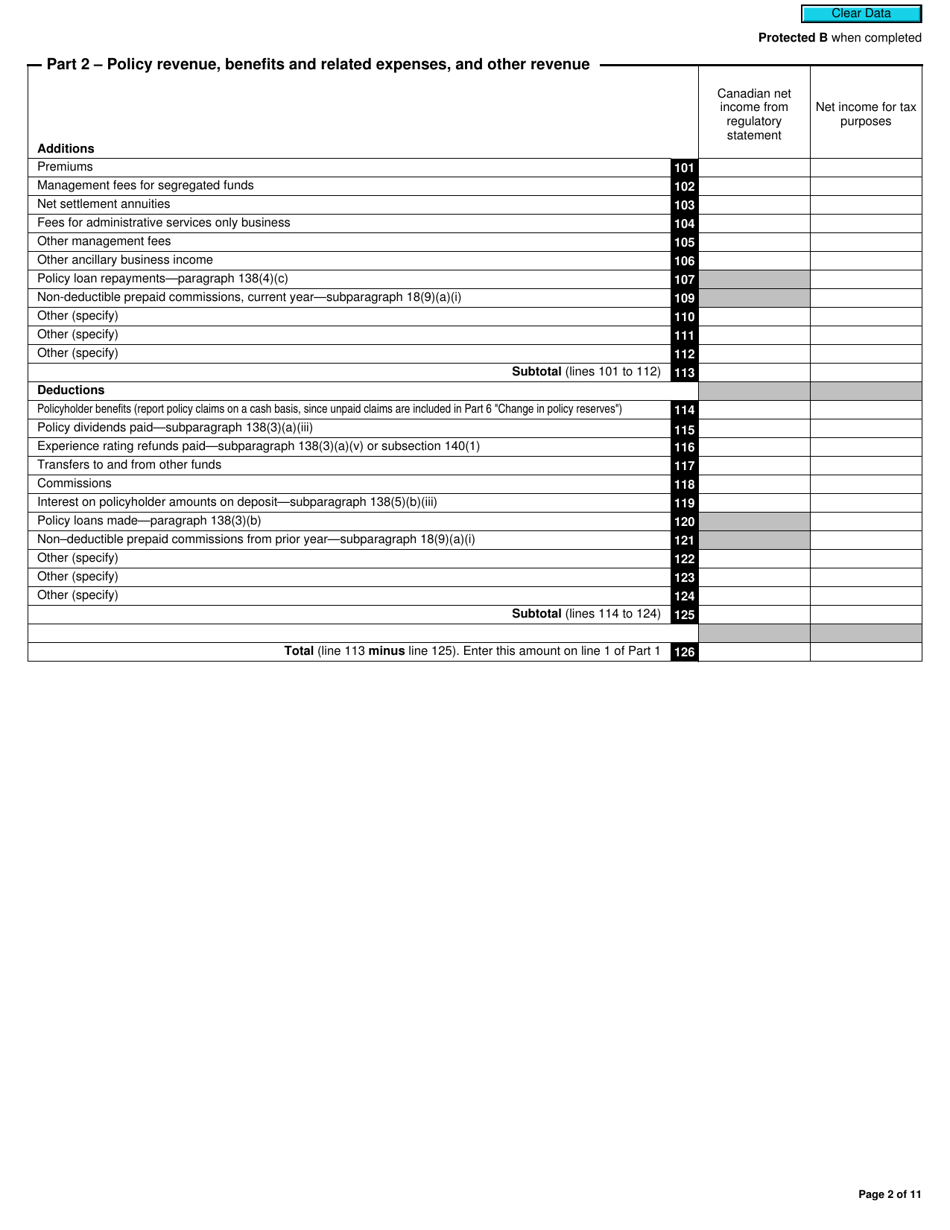

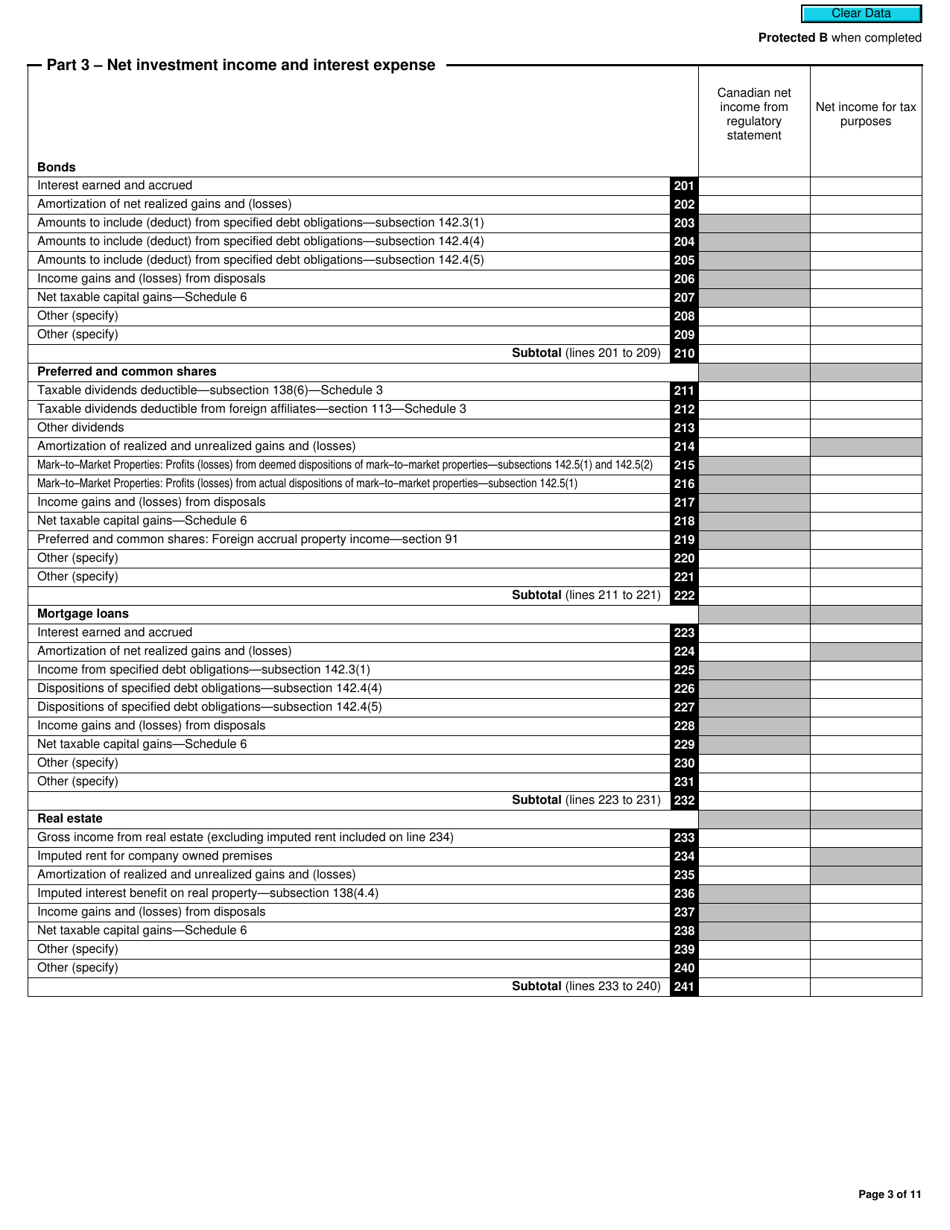

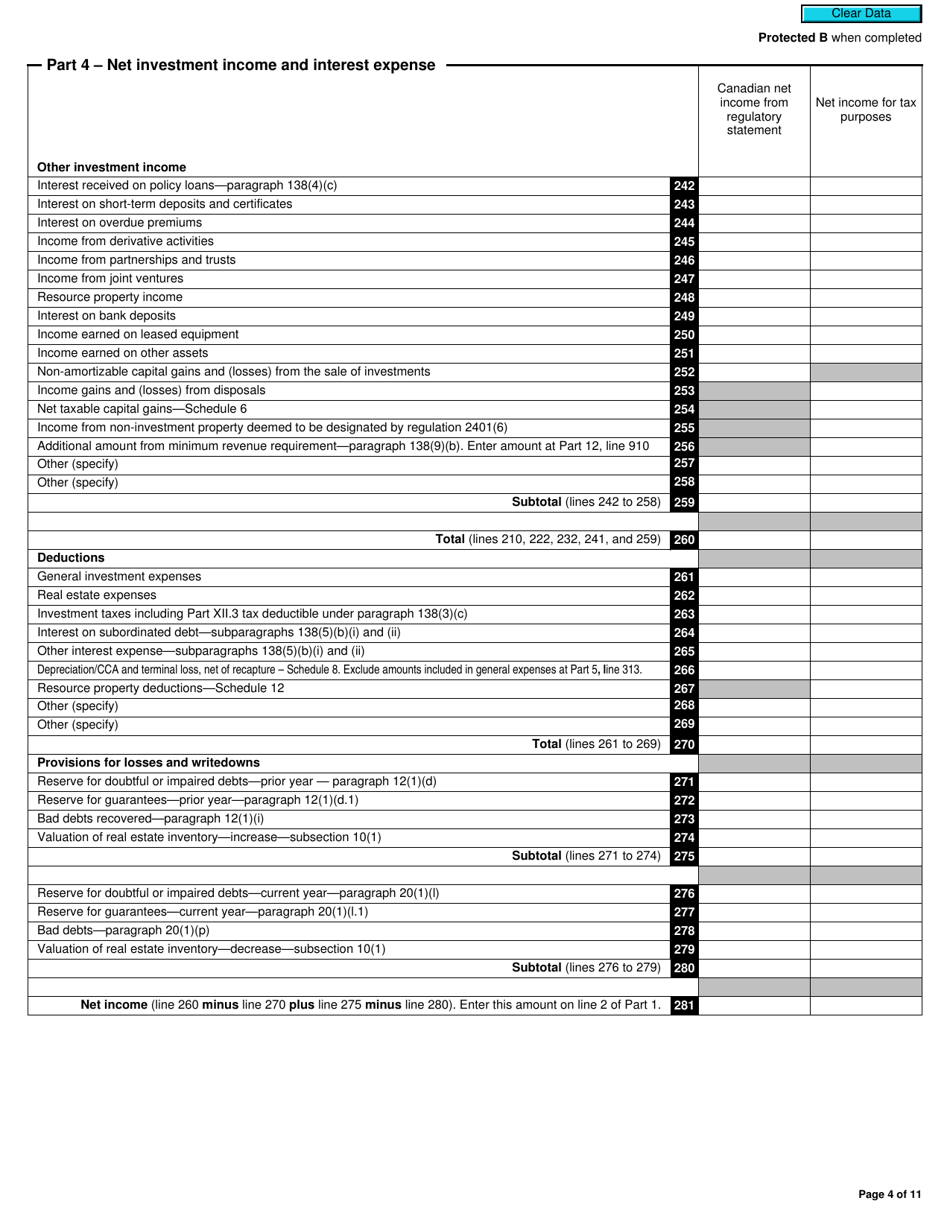

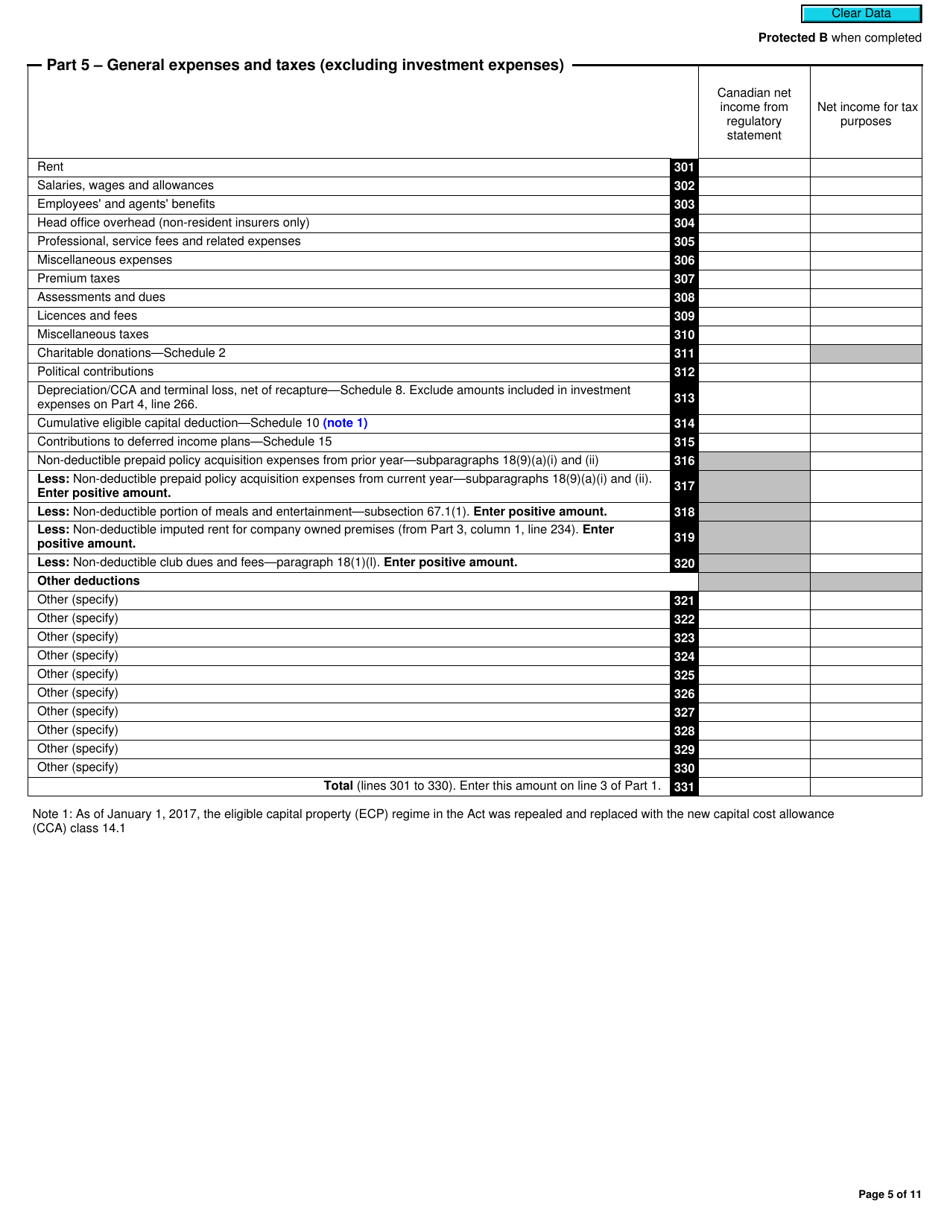

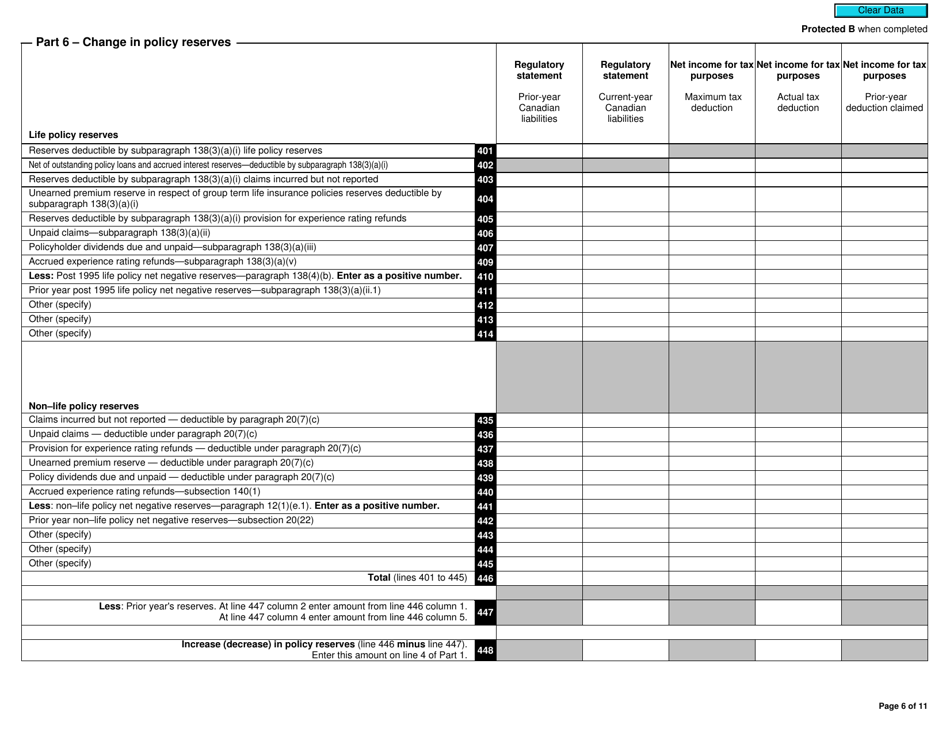

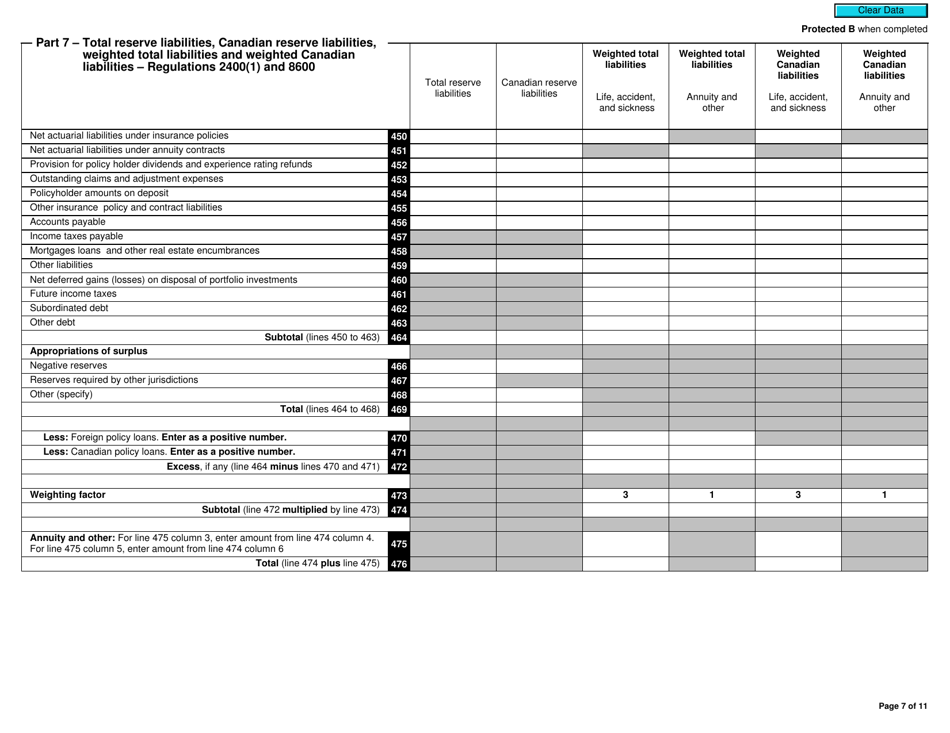

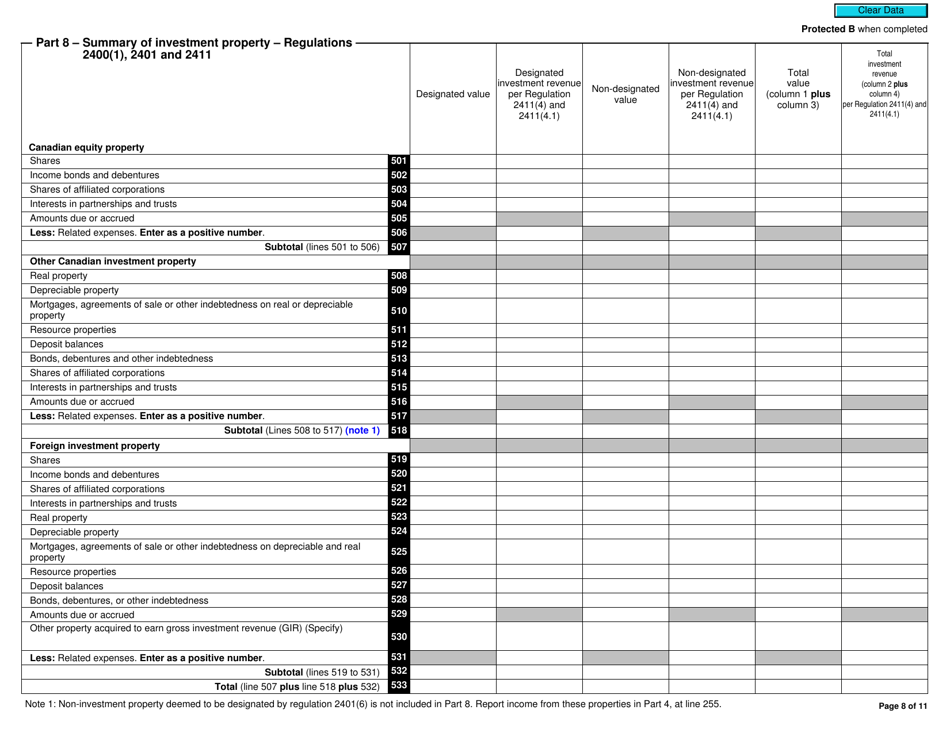

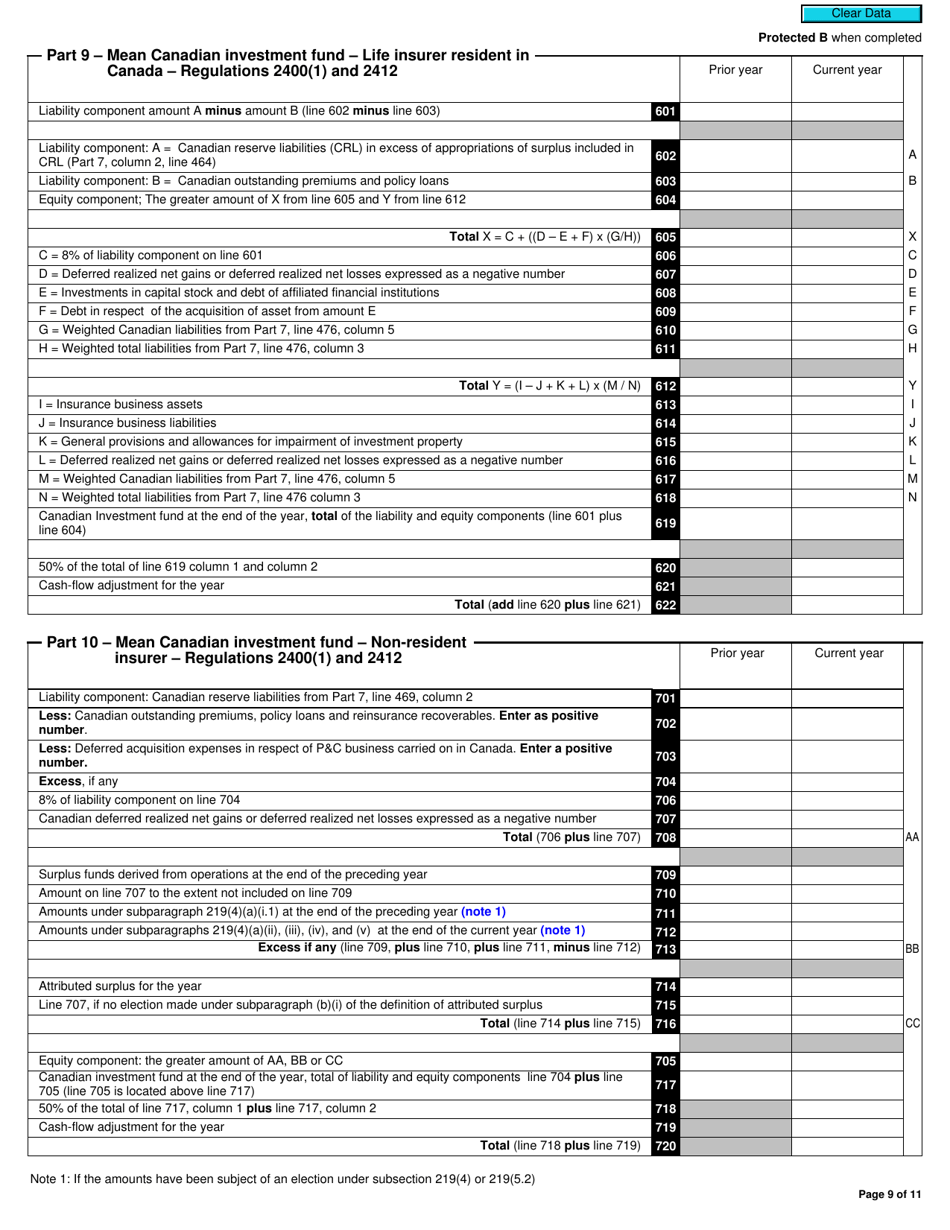

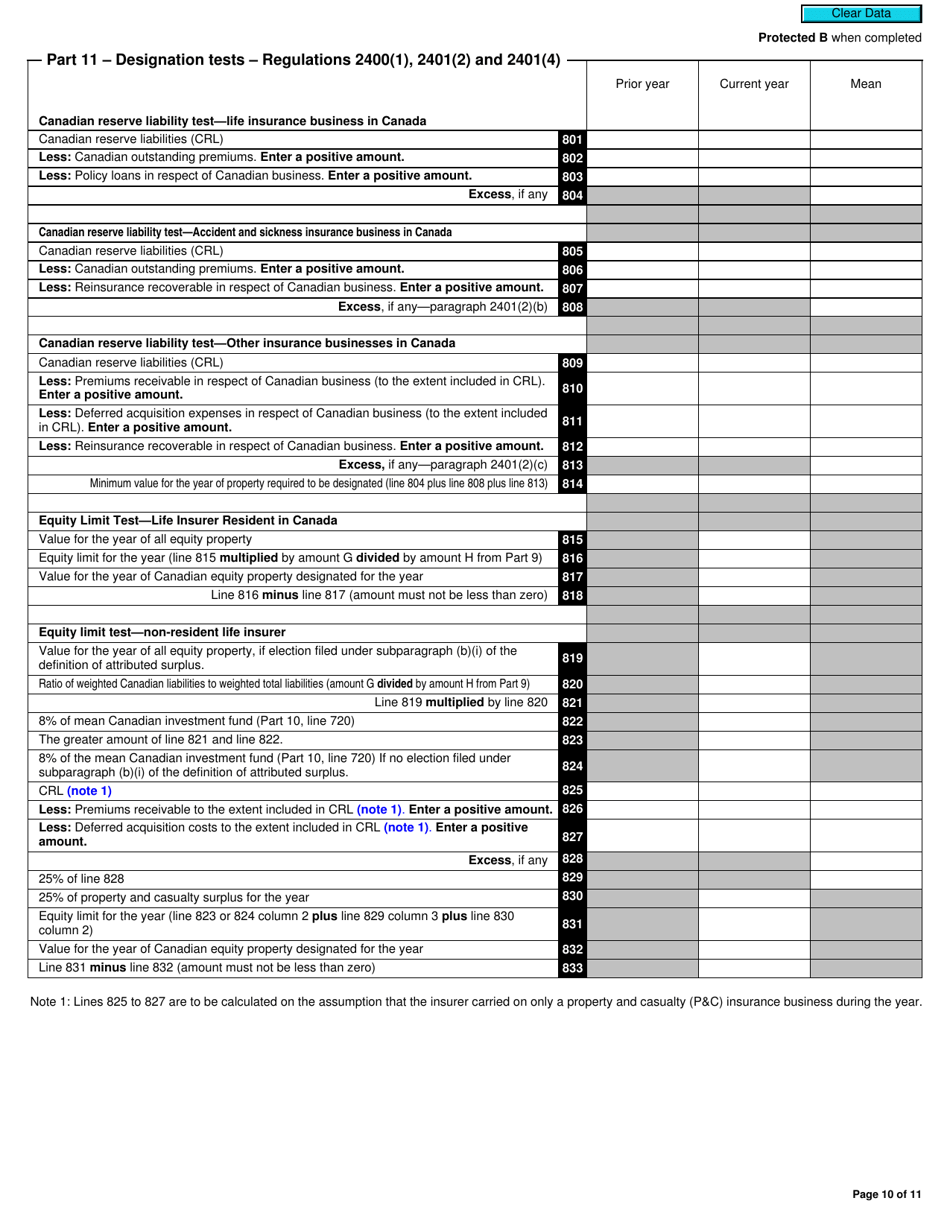

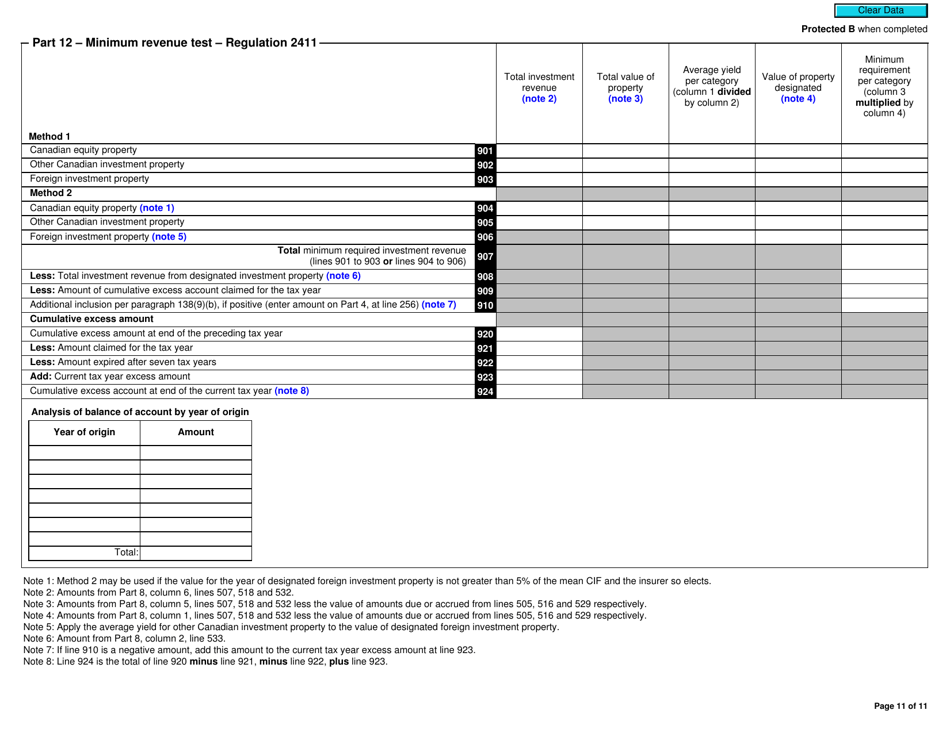

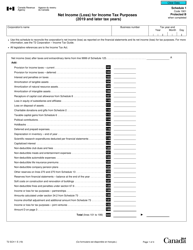

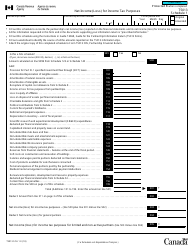

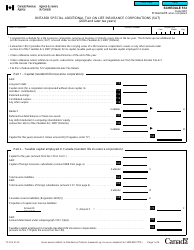

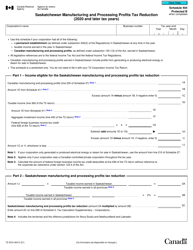

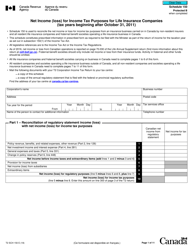

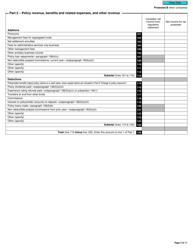

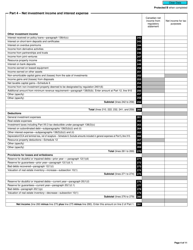

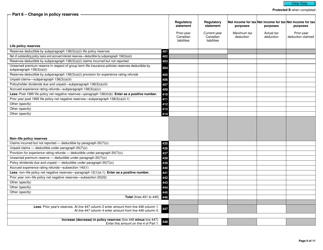

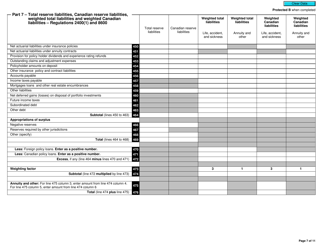

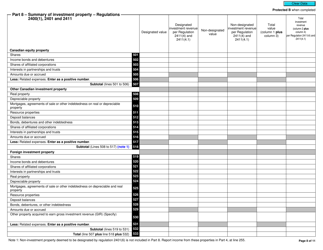

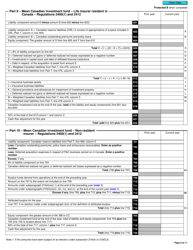

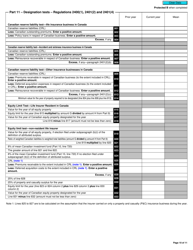

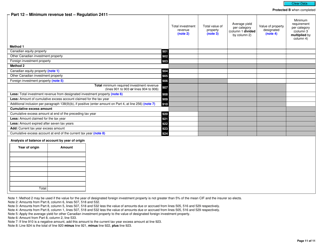

Form T2SCH150 Schedule 150 Net Income (Loss) for Income Tax Purposes for Life Insurance Companies (For Tax Years Beginning After October 31, 2011) - Canada

Form T2SCH150 Schedule 150 is used by life insurance companies in Canada to calculate their net income or loss for income tax purposes. It is specifically for tax years beginning after October 31, 2011.

Life insurance companies in Canada file the Form T2SCH150 Schedule 150 Net Income (Loss) for Income Tax Purposes for Life Insurance Companies (For Tax Years Beginning After October 31, 2011).

FAQ

Q: What is T2SCH150?

A: T2SCH150 is a schedule for reporting net income (loss) for income tax purposes for life insurance companies in Canada.

Q: Which tax years does T2SCH150 apply to?

A: T2SCH150 applies to tax years beginning after October 31, 2011.

Q: Who needs to file T2SCH150?

A: Life insurance companies in Canada need to file T2SCH150.

Q: What does T2SCH150 report?

A: T2SCH150 reports the net income (loss) for income tax purposes for life insurance companies.

Q: Is there a deadline for filing T2SCH150?

A: Yes, the deadline for filing T2SCH150 is the same as the deadline for filing the T2 corporate income tax return, which is generally within six months after the end of the tax year.

Download Form T2SCH150 Schedule 150 Net Income (Loss) for Income Tax Purposes for Life Insurance Companies (For Tax Years Beginning After October 31, 2011) - Canada

1

2

3

4

5

6

7

8

9

10

11