![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 8962

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 8962

for the current year.

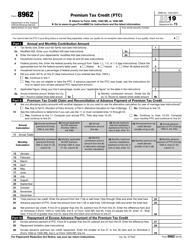

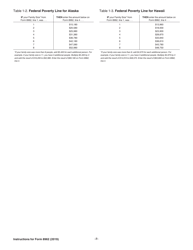

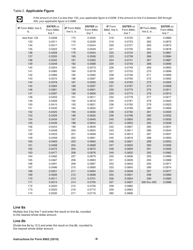

Instructions for IRS Form 8962 Premium Tax Credit (Ptc)

This document contains official instructions for IRS Form 8962 , Premium Tax Credit (Ptc) - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 8962 is available for download through this link.

FAQ

Q: What is IRS Form 8962?

A: IRS Form 8962 is the form used to reconcile and claim the Premium Tax Credit (PTC).

Q: What is the Premium Tax Credit (PTC)?

A: The Premium Tax Credit (PTC) is a refundable tax credit that helps eligible individuals and families pay for health insurance premiums through the Health Insurance Marketplace.

Q: Who needs to file Form 8962?

A: You need to file Form 8962 if you received advance payments of the Premium Tax Credit (APTC) or want to claim the PTC.

Q: How do I fill out IRS Form 8962?

A: You will need to provide information about your household and your health insurance coverage to fill out IRS Form 8962.

Q: What documents do I need to complete Form 8962?

A: You will need your Form 1095-A (Health Insurance Marketplace Statement) and Form 1095-B or 1095-C (if applicable) to complete Form 8962.

Q: What happens if I don't file Form 8962?

A: If you are required to file Form 8962 and fail to do so, your refund may be delayed or you may owe additional taxes.

Q: Can I file Form 8962 electronically?

A: Yes, you can file Form 8962 electronically if you are e-filing your tax return.

Q: How long does it take to process Form 8962?

A: The processing time for Form 8962 can vary, but the IRS generally processes it within 45 days.

Q: What if I made a mistake on Form 8962?

A: If you made a mistake on Form 8962, you should file an amended return using Form 1040X to correct the error.

Instruction Details:

- This 20-page document is available for download in PDF;

- Not applicable for the current tax year. Choose a more recent version to file this year's taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20