Loan Rehabilitation: Income and Expense Information

A Loan Rehabilitation: Income and Expense Information Form , is a legal document used by Collection Agencies to calculate the size of an affordable minimum monthly payment for the loan rehabilitation program.

Alternate Names:

- Federal Loan Rehabilitation Form.

The U.S. Department of Education has approved new revisions for Loan Rehabilitation Income and Expense Information form. This is the newest version of the form and filers should disregard the OMB Control Number. This form will not expire and if it does - we will have it replaced. A fillable Federal Loan Rehabilitation Form is available for download below.

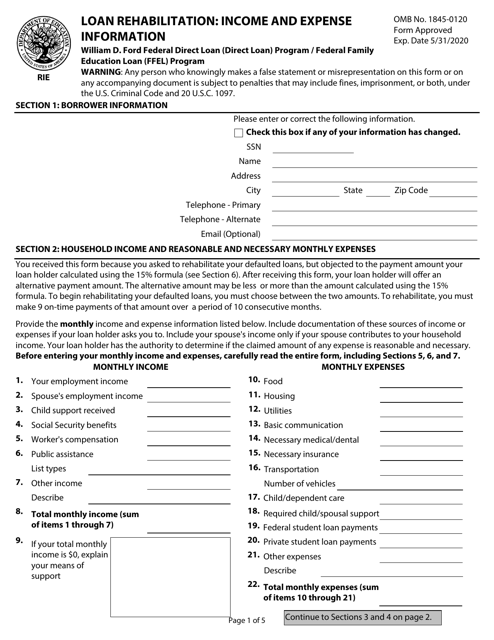

Federal Loan Rehabilitation Form Instructions

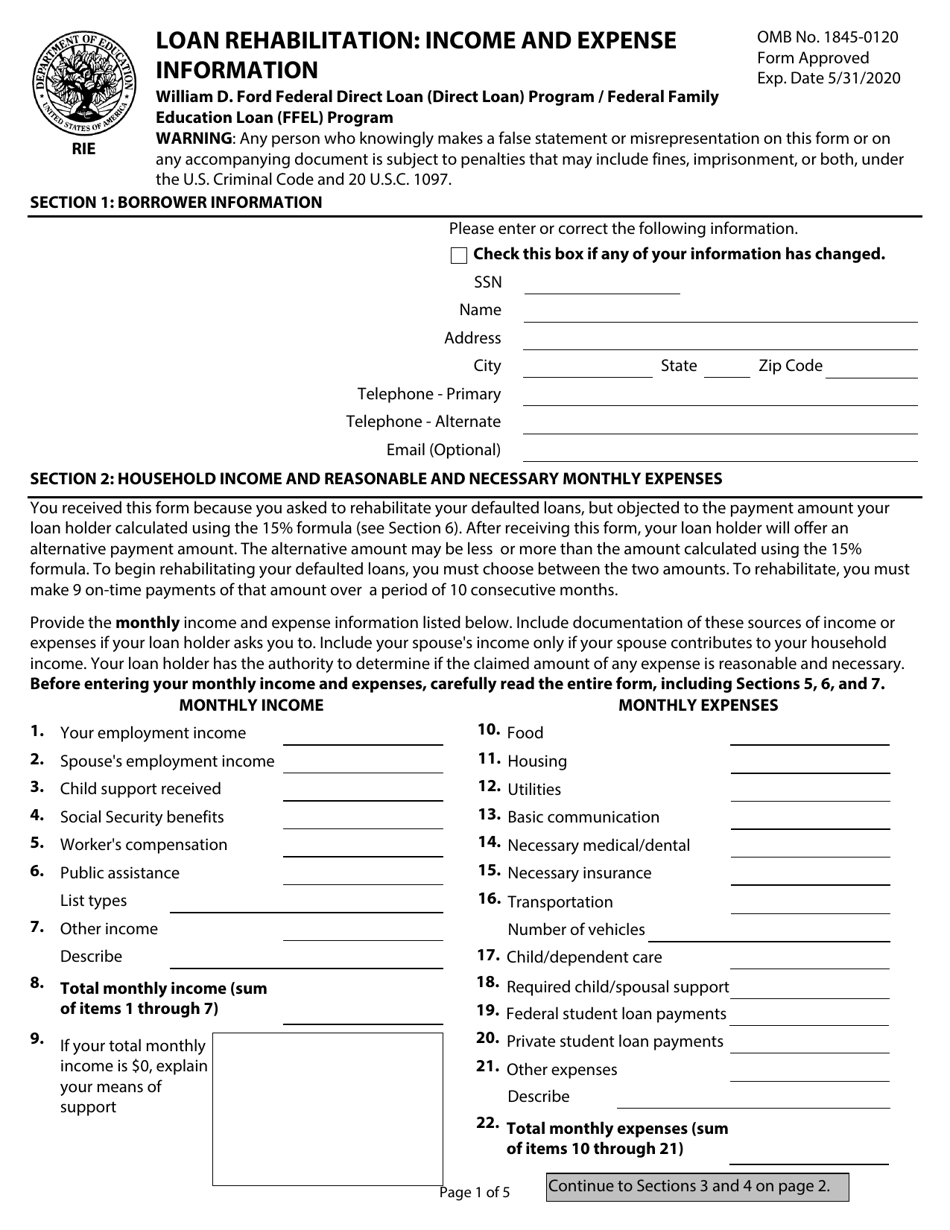

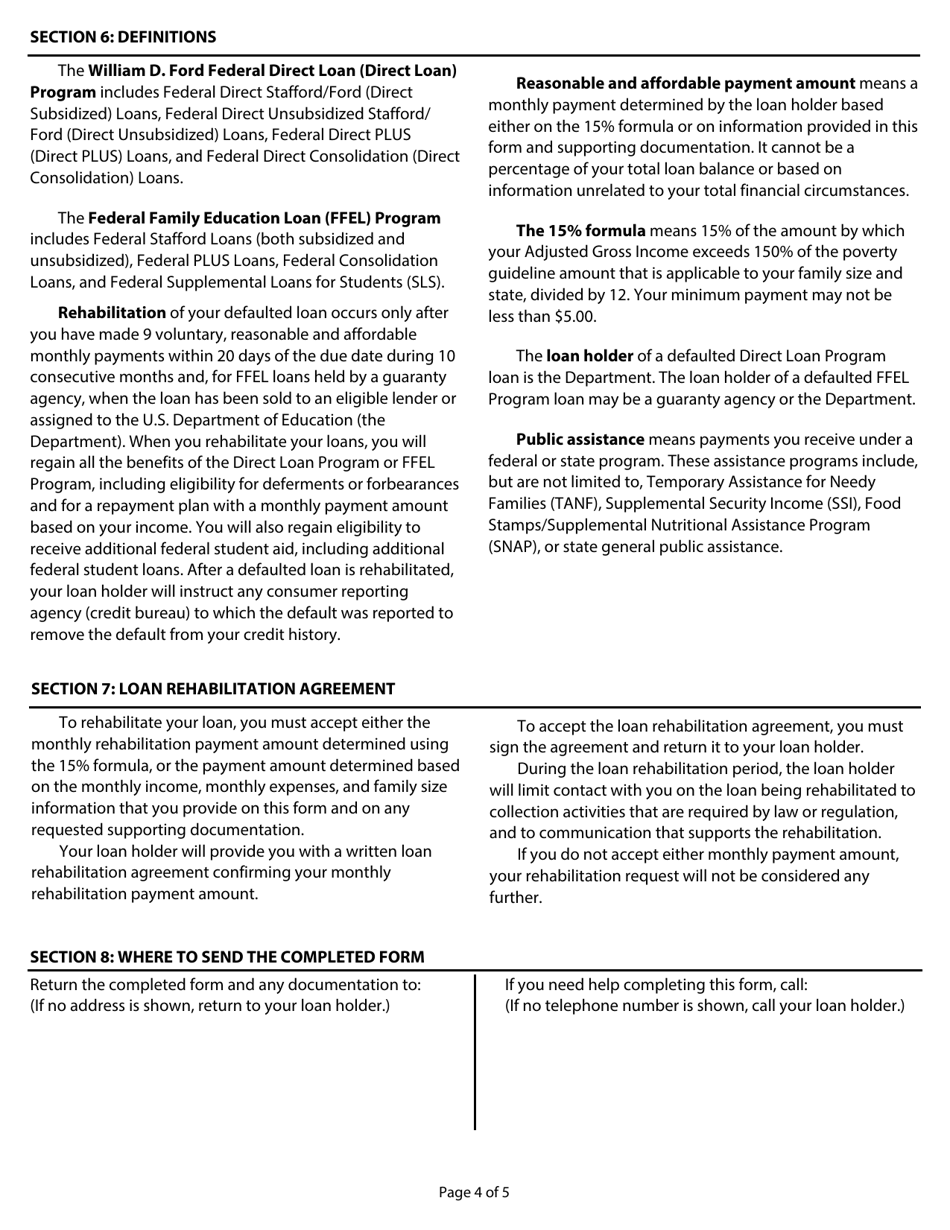

Why rehabilitate your loans? To get Public Assistance (payments one receives under a federal or state program) if such a need occurs due to family circumstances, and to regain the benefits of the various loan programs for a repayment plan on previously defaulted loans with a monthly payment amount based on an individual's income.

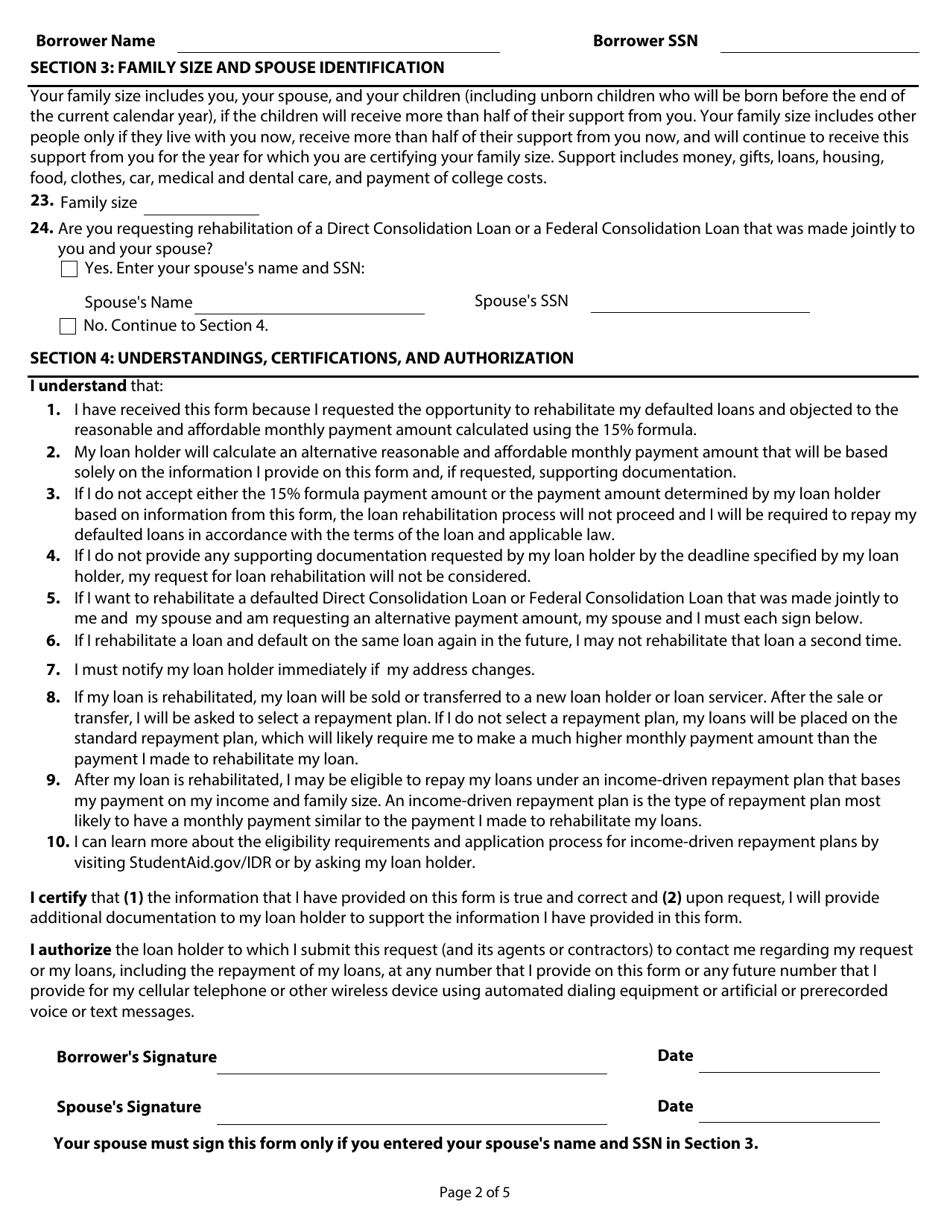

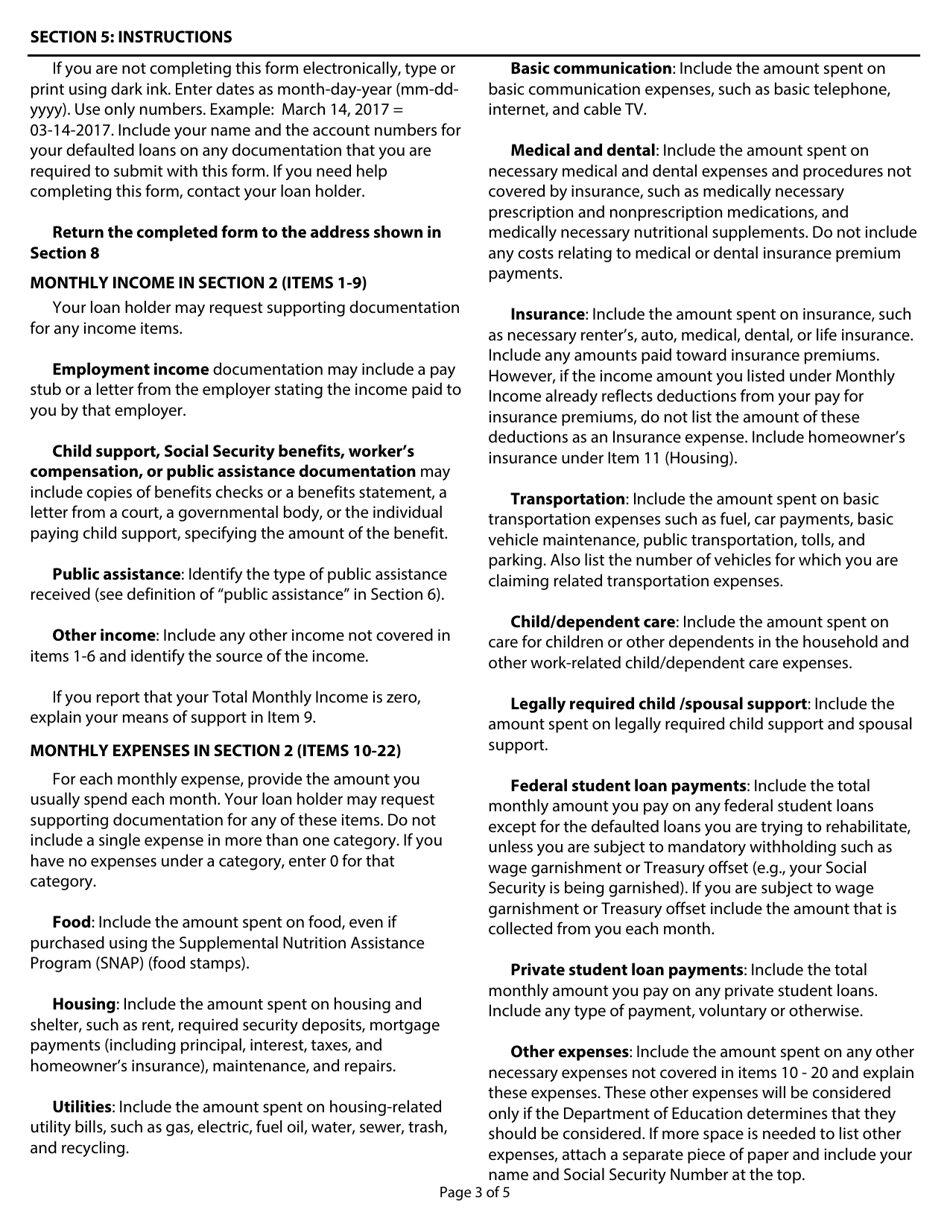

The purpose of the Federal Loan Rehabilitation Form is to get the right size payment based on income and expenses. To prepare the information needed for filing all necessary information on a form, some documents like pay stubs or proof of other income for the last 90 days have to be collected as well as documented necessary expenses (receipts and such). Only certain expenses qualify as necessary expenses. It is the cost of groceries and housing (including utility and insurance costs), communication costs (ie phone bills), necessary medical and dental, child care, some student loans, etc. An AGI, or Adjusted Gross Income, will have to be calculated based on this information. AGI is an individual's total gross income minus allowed deductions (expenses).

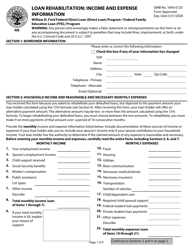

There are two ways to calculate monthly payment: It can be 15% of your monthly discretionary income (subtracting 150% of the poverty guidelines for the family size, divided by 12 from a calculated AGI); or calculating income and expenses using the Federal Loan Rehabilitation Form. The federal poverty guidelines are set by the Census Bureau (Issued annually by the Department of Health and Human Services).

Related Tags and Topics:

Download Loan Rehabilitation: Income and Expense Information

1

2

3

4

5