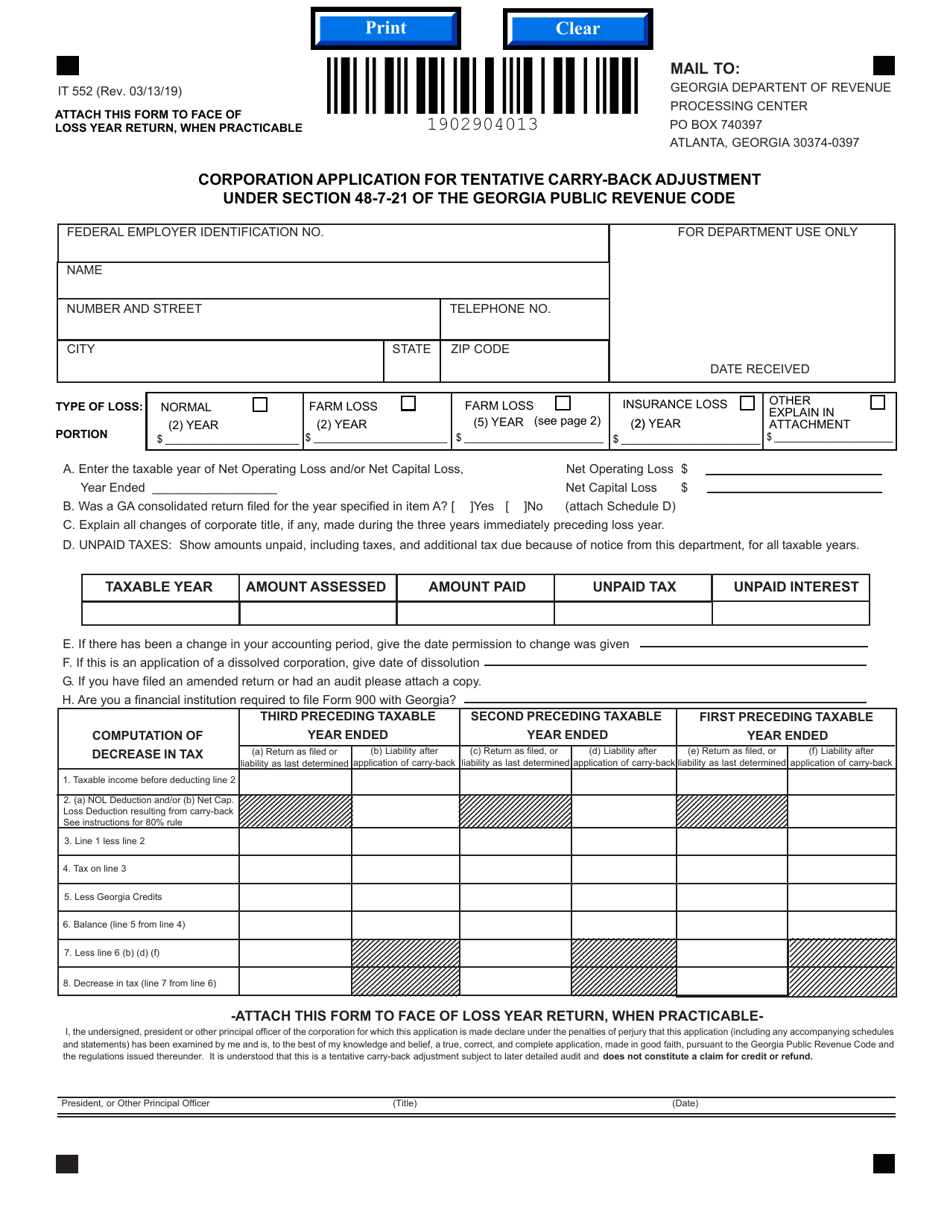

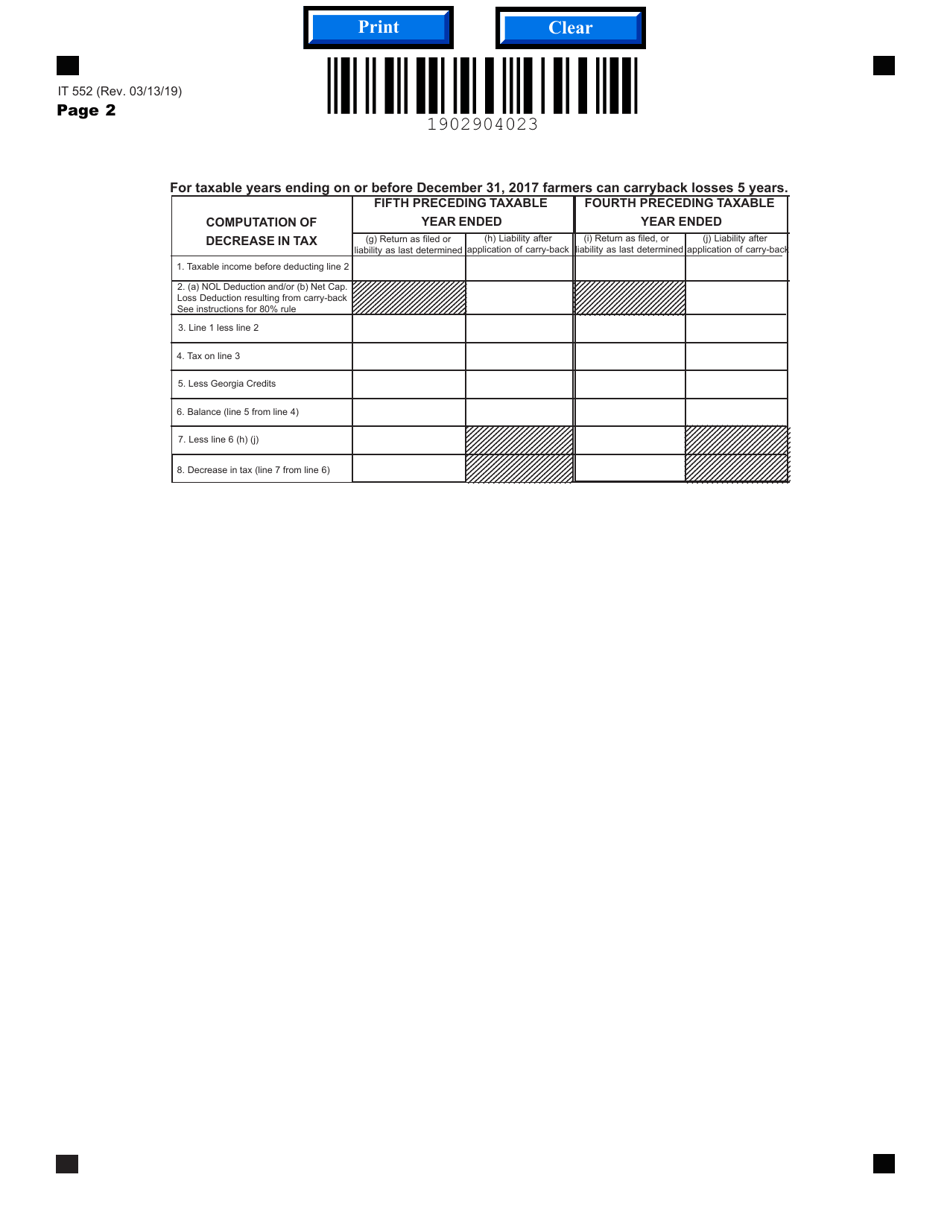

Form IT552 Corporation Application for Tentative Carry-Back Adjustment Under Section 48-7-2 1 of the Georgia Public Revenue Code - Georgia (United States)

What Is Form IT552?

This is a legal form that was released by the Georgia Department of Revenue - a government authority operating within Georgia (United States). As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is the IT552 form?

A: The IT552 form is the Corporation Application for Tentative Carry-Back Adjustment Under Section 48-7-21 of the Georgia Public Revenue Code.

Q: What is the purpose of the IT552 form?

A: The purpose of the IT552 form is to apply for a tentative carry-back adjustment for a corporation's tax liability in Georgia.

Q: Which section of the Georgia Public Revenue Code does the IT552 form refer to?

A: The IT552 form refers to Section 48-7-21 of the Georgia Public Revenue Code.

Q: Who is eligible to use the IT552 form?

A: Corporations in Georgia are eligible to use the IT552 form.

Q: What is a tentative carry-back adjustment?

A: A tentative carry-back adjustment allows a corporation to apply a net operating loss to a previous tax year to reduce its tax liability.

Q: Are there any fees associated with filing the IT552 form?

A: There are no fees associated with filing the IT552 form.

Q: What documents should be included with the IT552 form?

A: You should include supporting documentation such as federal tax return forms and schedules with the IT552 form.

Q: What is the deadline for filing the IT552 form?

A: The IT552 form should be filed within three years from the original due date of the return for the tax year in which the net operating loss occurred.

Form Details:

- Released on March 13, 2019;

- The latest edition provided by the Georgia Department of Revenue;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form IT552 by clicking the link below or browse more documents and templates provided by the Georgia Department of Revenue.

Download Form IT552 Corporation Application for Tentative Carry-Back Adjustment Under Section 48-7-2 1 of the Georgia Public Revenue Code - Georgia (United States)

1

2

3