Form T778 Child Care Expenses Deduction - Canada

What Is Form T778?

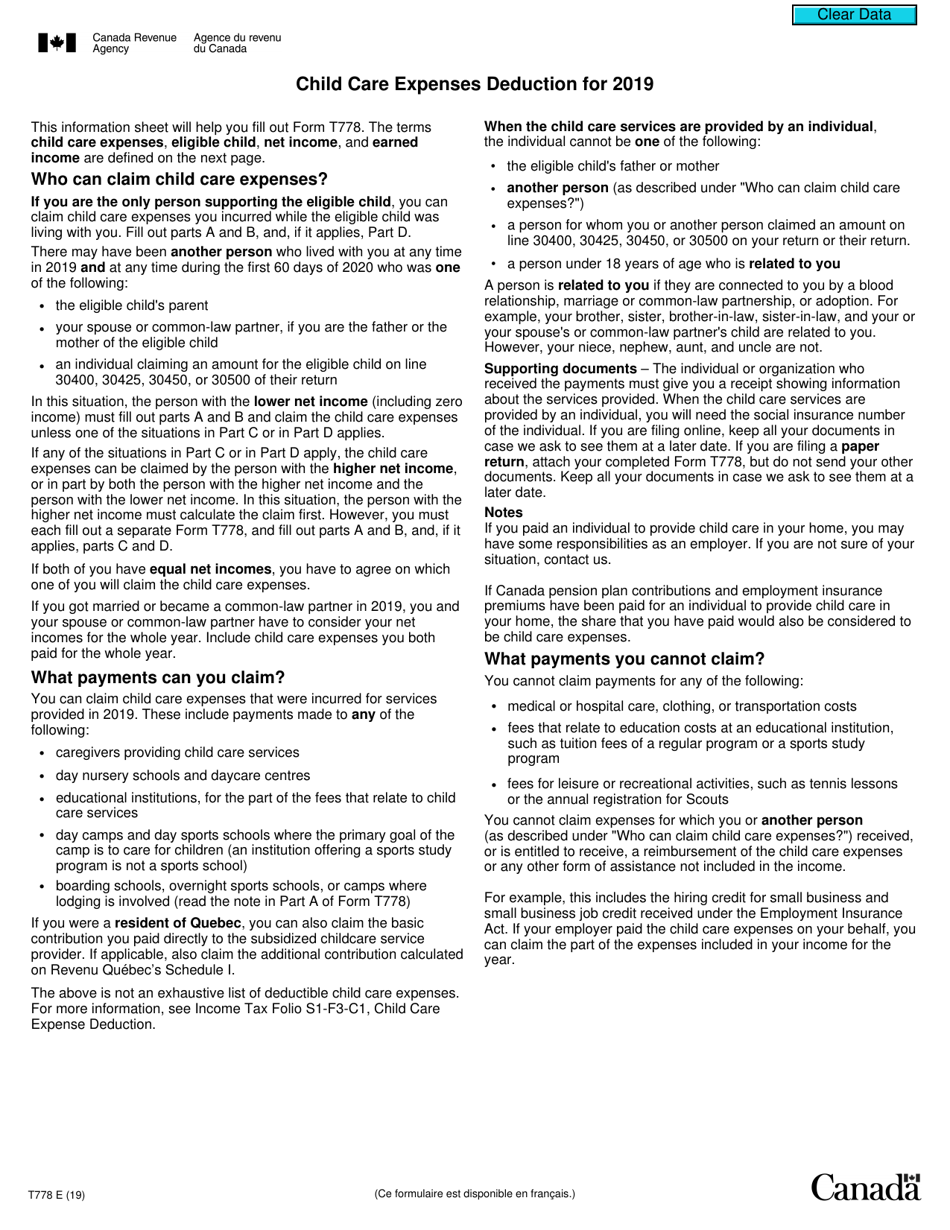

Form T778, Child Care Expenses Deduction , is used by parents to claim expenses incurred from child care on their taxes. The child care expensestax deduction is intended to be used by single parents or in the case of married or common-law partnerships, the parent who is the lower earner, however, both parents of a child will not be able to submit the same claim.

Alternate Name:

- Tax Form T778.

This form is issued by the Canadian Revenue Agency (CRA) and was last updated on January 1, 2019 . A fillable T778 Form is available for download below. A large-print version of this document can be found through this link.

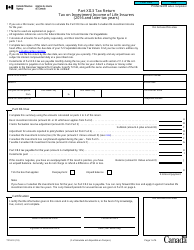

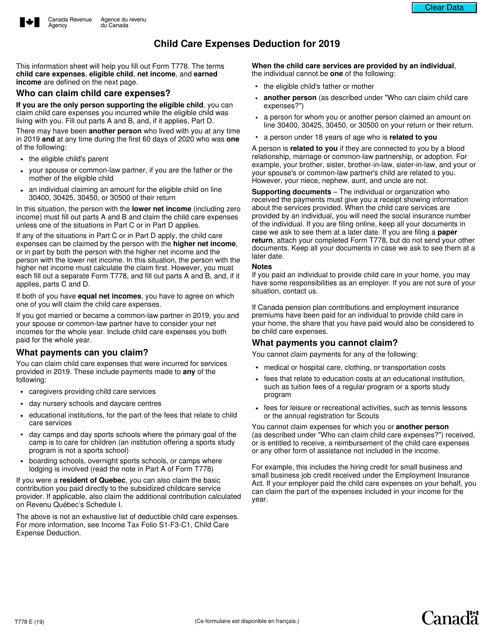

How to Fill Out Form T778?

To complete Form T778, the Child Care Expenses Deduction, you will need to provide the following information:

-

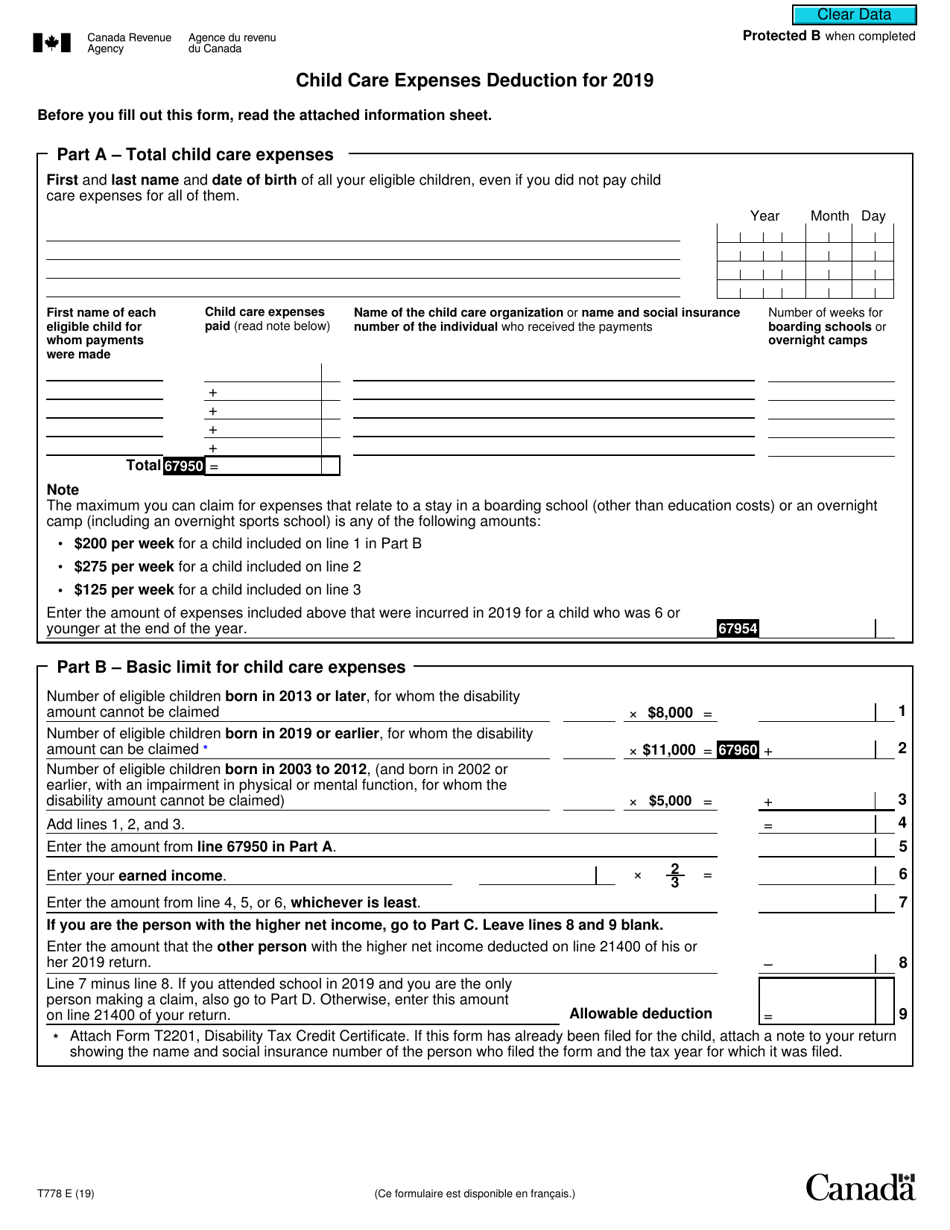

Information about your children and expenses related to child care:

- The name of each child that qualifies for the deduction and their date of birth;

- The total dollar amount of child care expenses per child and the name of the business or organization where the child attended child care;

- If your child attended any boarding school or overnight outdoor program you can also include the number of weeks they stayed;

- Use the "Note" section of this part to make sure you do not claim over the maximum deduction amount permitted for each child;

- There is an additional line where you can input the number of expenses for a child age six or younger from the previous tax year.

-

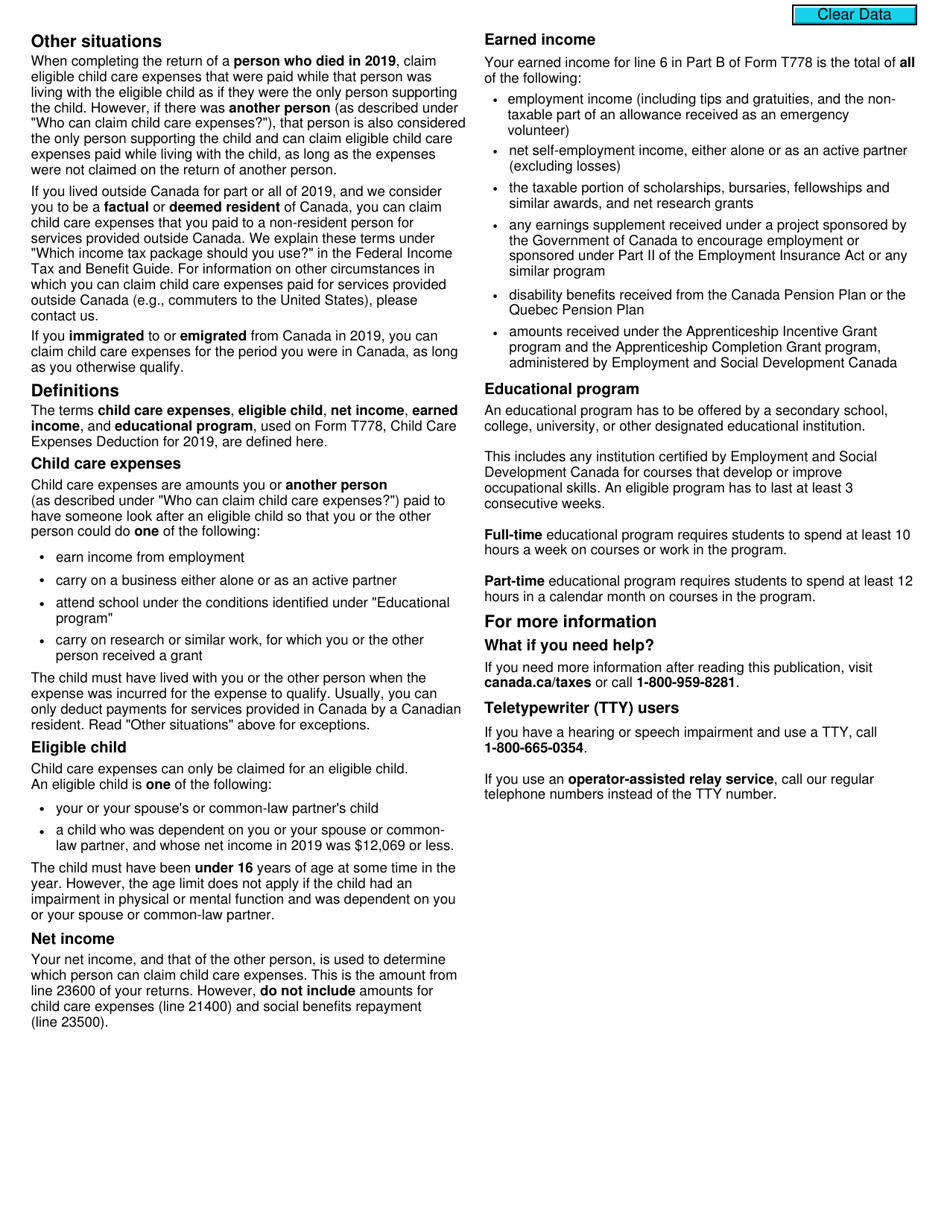

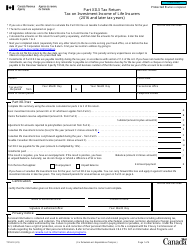

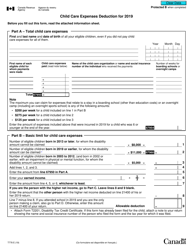

Expenses related to children born with a physical or mental impairment and the parent's earned income:

- List the children who have a disability that you are a parent or guardian of to calculate additional deductions;

- Add the total deduction amounts related to disabilities, below that you will list the total amount of deductions from the first section;

- Enter the amount of income earned and multiply this number by two-thirds;

- From this total, subtract the total deduction amount the parent with the higher income listed on Line 21400 of their tax return. This will then give you the total amount of your allowable deduction.

-

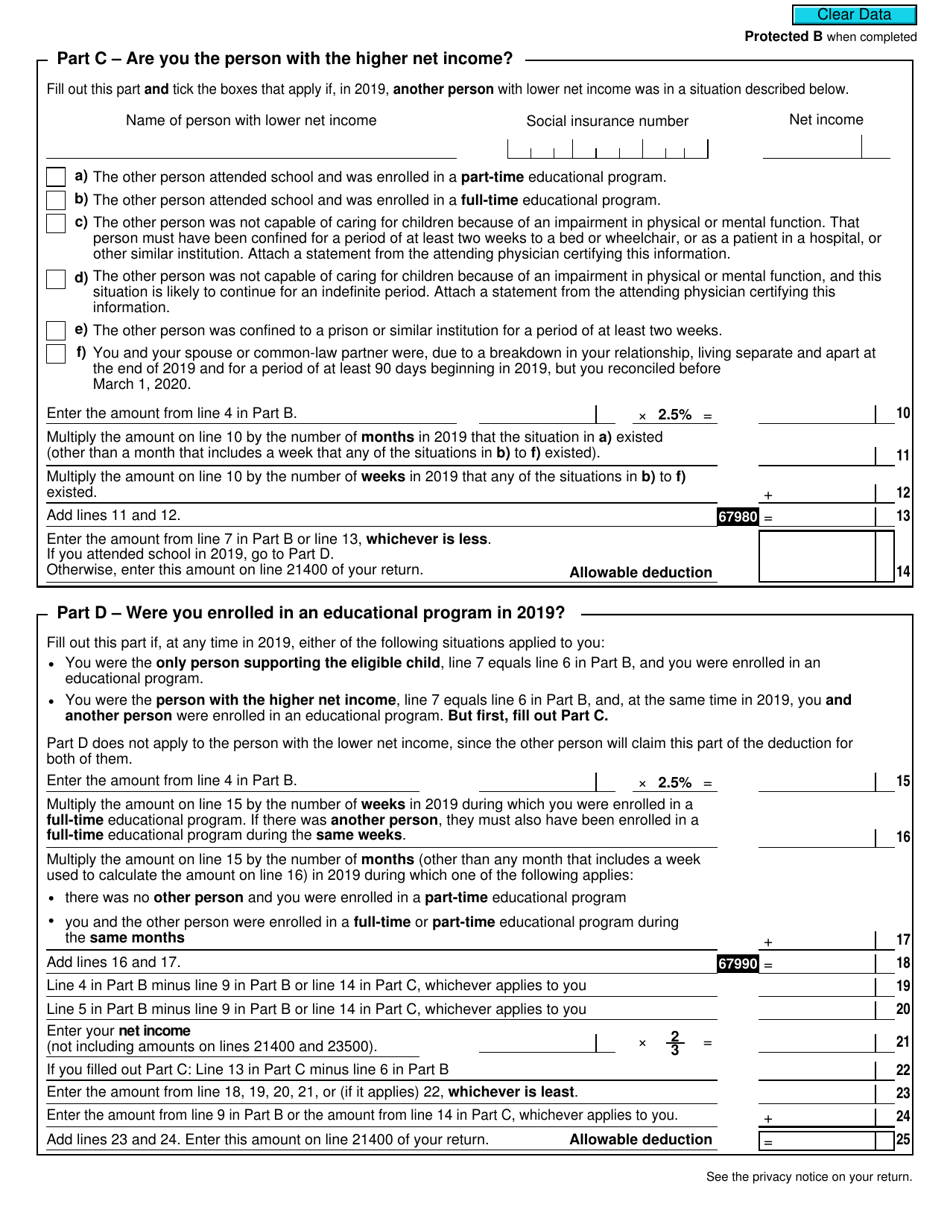

If you find you are the parent with the higher income you will need to complete the next section that will have you input the total income amount earned by the parent with the lower income. This section will then calculate the total amount of deduction you are able to claim as the higher earner.

-

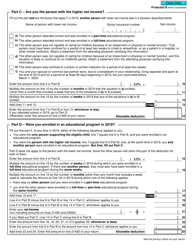

The final section of Tax Form T778 asks if either parent had been enrolled in any educational program during the year to calculate deductions for education.

Download Form T778 Child Care Expenses Deduction - Canada

1

2

3

4