Employer's Guide to the Work Opportunity Pportunity Tax Credit

Employer's Guide to the Work Opportunity Pportunity Tax Credit is a 9-page legal document that was released by the U.S. Department of Labor - Employment & Training Administration on August 1, 2014 and used nation-wide.

FAQ

Q: What is the Work Opportunity Tax Credit?

A: The Work Opportunity Tax Credit (WOTC) is a federal tax credit available to employers who hire individuals from specific targeted groups.

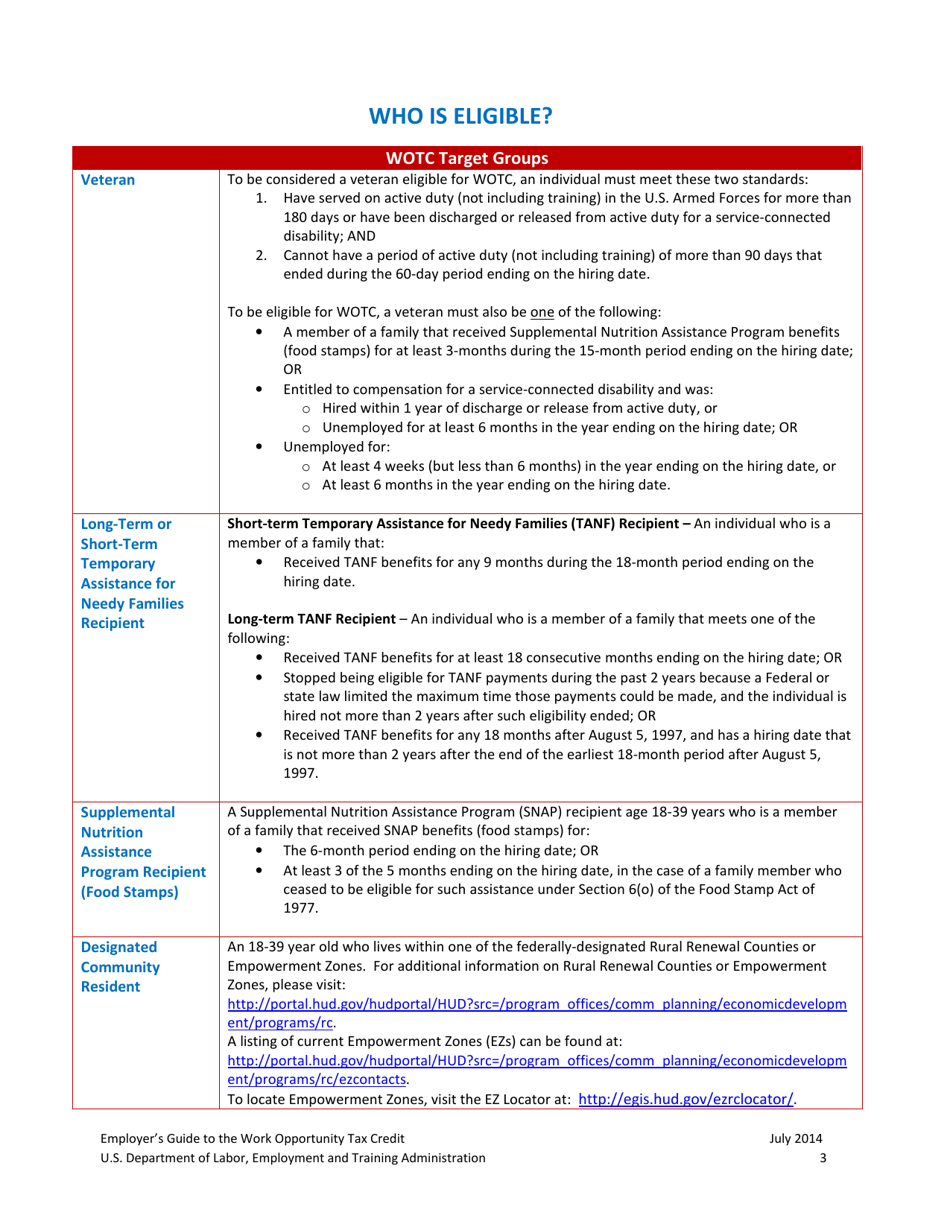

Q: Who qualifies for the Work Opportunity Tax Credit?

A: Individuals from specific targeted groups, such as veterans, long-term unemployed individuals, ex-felons, and recipients of certain government assistance programs.

Q: How much is the Work Opportunity Tax Credit?

A: The amount of the tax credit depends on the target group of the individual hired and the number of hours worked by the employee.

Q: How can employers claim the Work Opportunity Tax Credit?

A: Employers can claim the credit by filing IRS Form 5884 and submitting it with their annual tax return.

Q: Is there a deadline to claim the Work Opportunity Tax Credit?

A: Yes, employers must submit their Form 5884 within 28 days after the eligible employee begins working.

Q: Are there any limitations or restrictions on the Work Opportunity Tax Credit?

A: Yes, the credit is subject to various limitations, such as the number of qualified employees an employer can claim credit for and the amount of wages eligible for the credit.

Q: Can the Work Opportunity Tax Credit be carried forward or back?

A: No, the credit cannot be carried forward or back, but it can be used to offset the employer's income tax liability for the current year.

Q: Are there any other tax incentives available for employers who hire individuals with disabilities?

A: Yes, in addition to the Work Opportunity Tax Credit, there are other tax incentives such as the Disabled Access Credit and the Barrier Removal Tax Deduction.

Form Details:

- The latest edition currently provided by the U.S. Department of Labor - Employment & Training Administration;

- Ready to use and print;

- Easy to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of the form by clicking the link below or browse more legal forms and templates provided by the issuing department.

Download Employer's Guide to the Work Opportunity Pportunity Tax Credit

1

2

3

4

5

6

7

8

9