![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form CT-637

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form CT-637

for the current year.

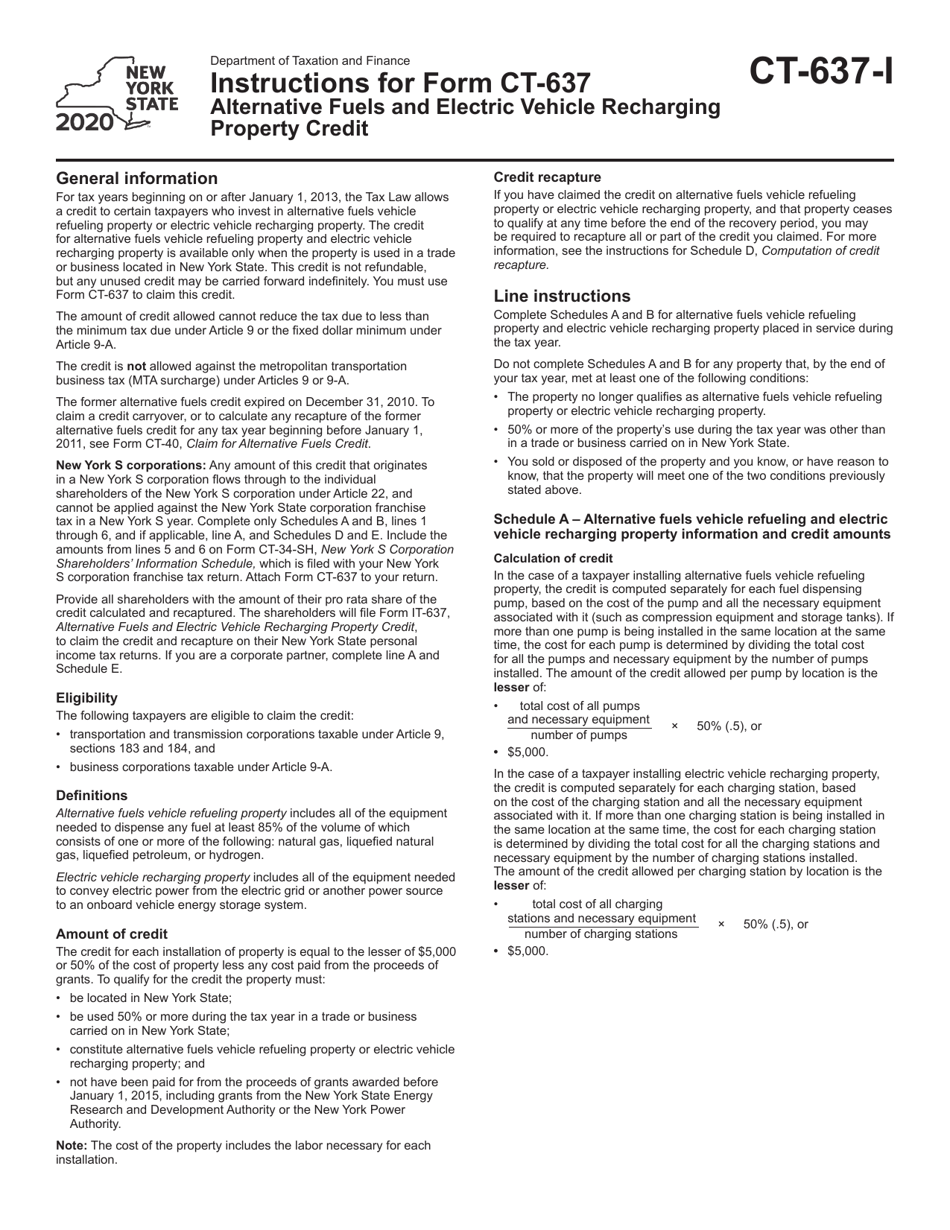

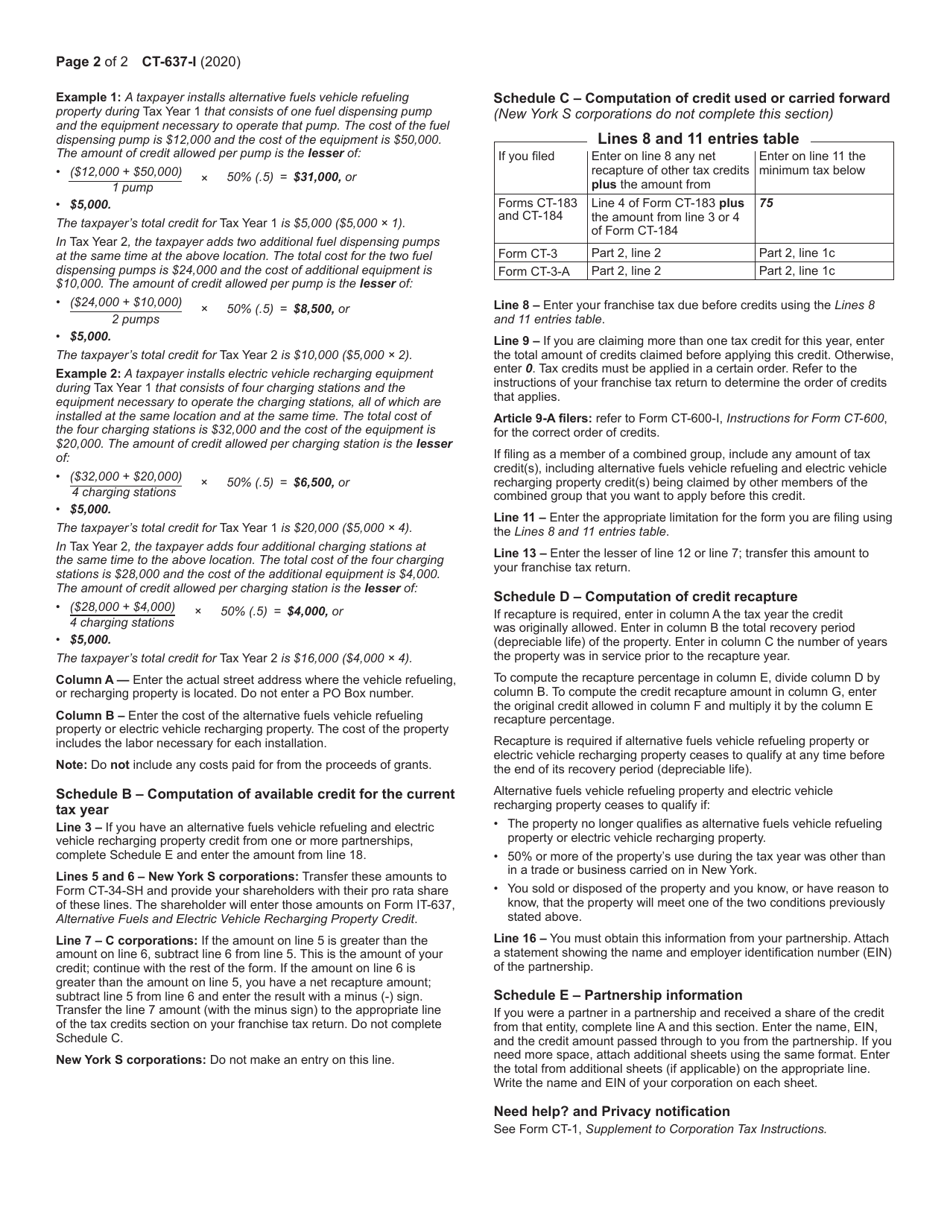

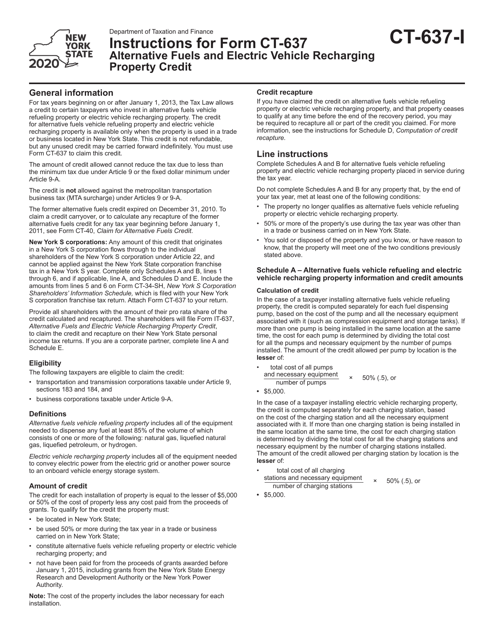

Instructions for Form CT-637 Alternative Fuels and Electric Vehicle Recharging Property Credit - New York

This document contains official instructions for Form CT-637 , Alternative Fuels and Electric Vehicle Recharging Property Credit - a form released and collected by the New York State Department of Taxation and Finance. An up-to-date fillable Form CT-637 is available for download through this link.

FAQ

Q: What is Form CT-637?

A: Form CT-637 is a form used to claim the Alternative Fuels and Electric Vehicle Recharging Property Credit in New York.

Q: What is the Alternative Fuels and Electric Vehicle Recharging Property Credit?

A: The Alternative Fuels and Electric Vehicle Recharging Property Credit is a tax credit available to individuals and businesses in New York who purchase or lease qualified alternative fuel or electric vehicle recharging property.

Q: Who is eligible to claim this credit?

A: Individuals and businesses in New York who purchase or lease qualified alternative fuel or electric vehicle recharging property are eligible to claim this credit.

Q: What is considered qualified alternative fuel property?

A: Qualified alternative fuel property includes equipment used for storing, compressing, or dispensing alternative fuels for use in a motor vehicle.

Q: What is considered qualified electric vehicle recharging property?

A: Qualified electric vehicle recharging property includes equipment used for recharging electric vehicles.

Q: What is the deadline for filing Form CT-637?

A: The deadline for filing Form CT-637 is the same as the deadline for filing your New York State income tax return.

Q: How much is the credit?

A: The credit is equal to 50% of the cost of the qualified alternative fuel or electric vehicle recharging property, up to a maximum credit of $5,000 for individuals and $200,000 for businesses.

Q: Can the credit be carried forward or refunded?

A: Yes, any unused credit can be carried forward for up to five years or refunded if the taxpayer elects to receive a refund instead of applying the credit to their tax liability.

Q: Are there any limitations or restrictions for claiming this credit?

A: Yes, there are various limitations and restrictions for claiming this credit, such as a maximum credit amount, certain taxable year requirements, and documentation requirements. It is recommended to review the instructions for Form CT-637 for more details.

Instruction Details:

- This 2-page document is available for download in PDF;

- Might not be applicable for the current year. Choose a more recent version;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the New York State Department of Taxation and Finance.

Download Instructions for Form CT-637 Alternative Fuels and Electric Vehicle Recharging Property Credit - New York

1

2