![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 5307

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 5307

for the current year.

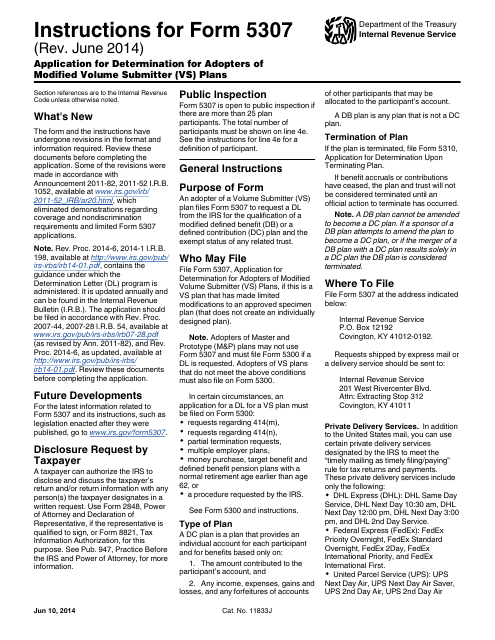

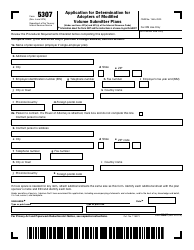

Instructions for IRS Form 5307 Application for Determination for Adopters of Modified Volume Submitter (VS) Plans

This document contains official instructions for IRS Form 5307 , Application for Determination for Adopters of Modified Volume Submitter (VS) Plans - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 5307 is available for download through this link.

FAQ

Q: What is IRS Form 5307?

A: IRS Form 5307 is an application for determination specifically for adopters of Modified Volume Submitter (VS) Plans.

Q: Who should use IRS Form 5307?

A: IRS Form 5307 should be used by those who want to determine if their Modified Volume Submitter (VS) Plan meets the requirements set by the IRS.

Q: What is a Modified Volume Submitter (VS) Plan?

A: A Modified Volume Submitter (VS) Plan is a type of retirement plan that meets specific requirements established by the IRS.

Q: Why do I need to use IRS Form 5307?

A: You need to use IRS Form 5307 to apply for determination from the IRS about your Modified Volume Submitter (VS) Plan.

Q: Are there any fees associated with filing IRS Form 5307?

A: Yes, there are fees associated with filing IRS Form 5307. The amount of the fee depends on the type of plan being submitted.

Q: What supporting documents do I need to submit with IRS Form 5307?

A: You need to submit a copy of the Volume Submitter (VS) Plan document and any other relevant documents as required by the IRS.

Q: How long does it take to process IRS Form 5307?

A: The processing time for IRS Form 5307 varies. It can take several months to receive a determination from the IRS.

Q: Can I file IRS Form 5307 electronically?

A: No, you cannot file IRS Form 5307 electronically. It must be submitted by mail or delivered in person.

Q: What should I do if my application is denied?

A: If your application is denied, you can request a conference with the IRS to discuss the denial and provide additional information or clarification.

Instruction Details:

- This 5-page document is available for download in PDF;

- Actual and applicable for filing 2023 taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

Download Instructions for IRS Form 5307 Application for Determination for Adopters of Modified Volume Submitter (VS) Plans

1

2

3

4

5