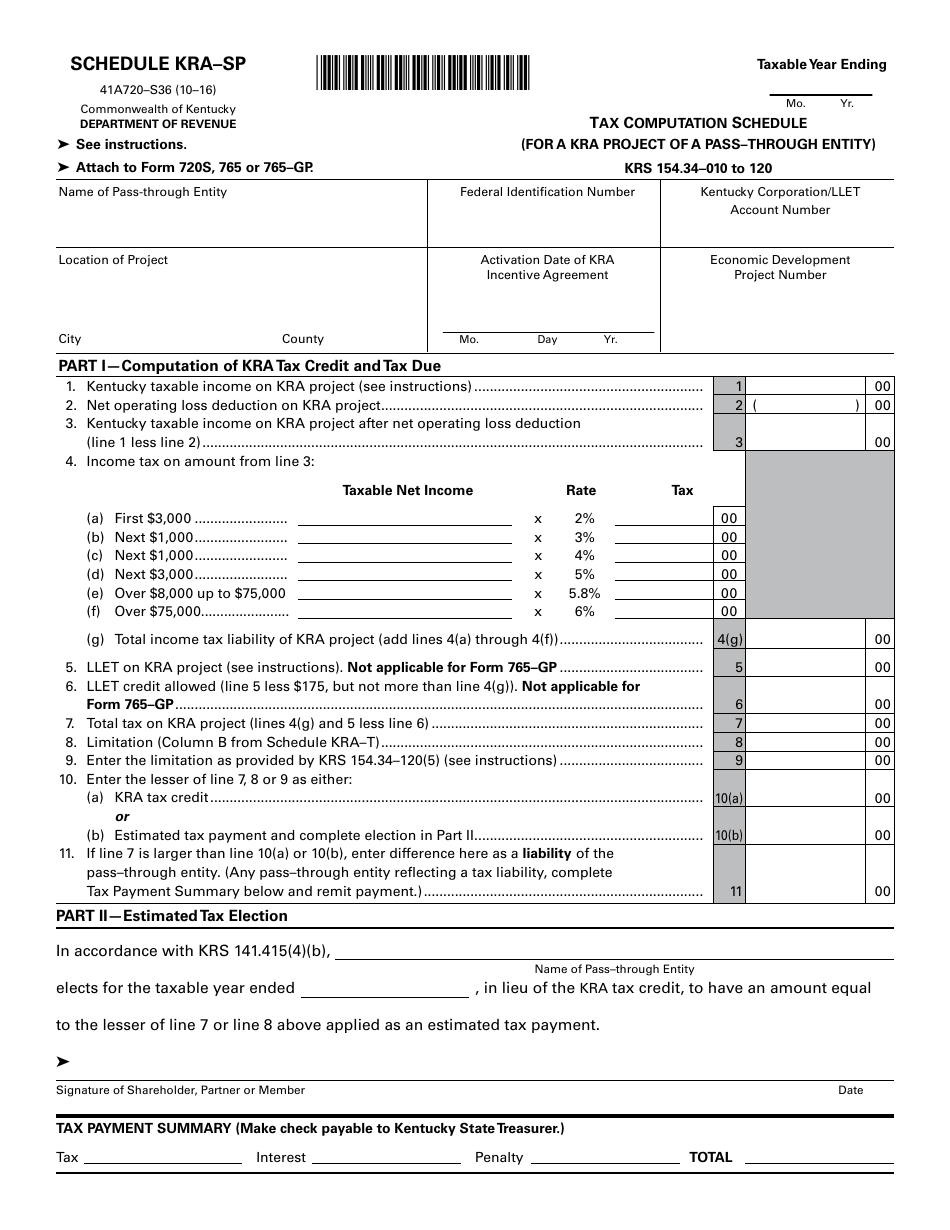

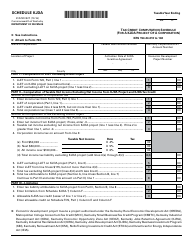

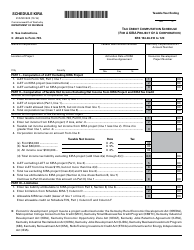

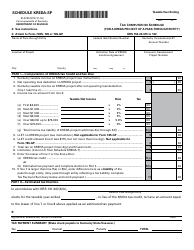

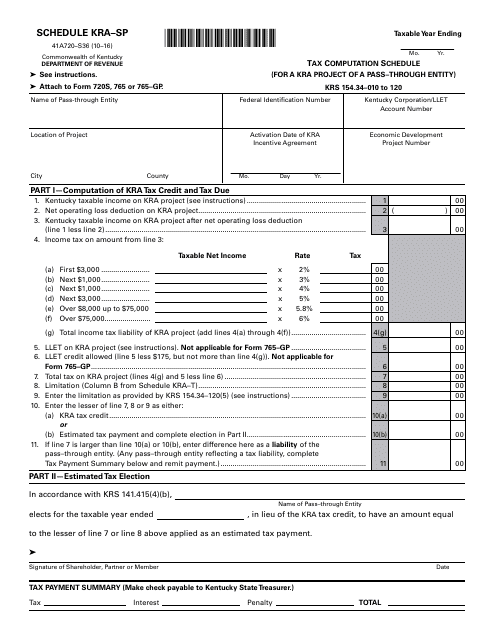

Form 41A720-S36 Schedule KRA-SP Tax Computation Schedule (For a Kra Project of a Pass-Through Entity) - Kentucky

What Is Form 41A720-S36 Schedule KRA-SP?

This is a legal form that was released by the Kentucky Department of Revenue - a government authority operating within Kentucky. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form 41A720-S36?

A: Form 41A720-S36 is the Schedule KRA-SP Tax Computation Schedule for a Kra Project of a Pass-Through Entity in Kentucky.

Q: What is a pass-through entity?

A: A pass-through entity is a business structure where the profits and losses of the business pass through to the owners or shareholders for tax purposes.

Q: What is a Kra Project?

A: A Kra Project refers to a Kentucky Resource Assessment (KRA) Project.

Q: What is the purpose of the Schedule KRA-SP?

A: The Schedule KRA-SP is used by pass-through entities in Kentucky to calculate the tax liability for a Kra Project.

Q: Who needs to file Form 41A720-S36?

A: Pass-through entities in Kentucky that have a Kra Project need to file Form 41A720-S36.

Q: What information is required on Form 41A720-S36?

A: Form 41A720-S36 requires information about the pass-through entity, the Kra Project, and the tax computation for the project.

Q: What is the deadline for filing Form 41A720-S36?

A: The deadline for filing Form 41A720-S36 is usually the same as the deadline for filing the pass-through entity's Kentucky tax return.

Q: Are there any penalties for late filing of Form 41A720-S36?

A: Yes, late filing of Form 41A720-S36 may result in penalties and interest charges.

Q: Is Form 41A720-S36 used for individual tax filing?

A: No, Form 41A720-S36 is specifically for pass-through entities and does not apply to individual tax filing in Kentucky.

Form Details:

- Released on October 1, 2016;

- The latest edition provided by the Kentucky Department of Revenue;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form 41A720-S36 Schedule KRA-SP by clicking the link below or browse more documents and templates provided by the Kentucky Department of Revenue.

Download Form 41A720-S36 Schedule KRA-SP Tax Computation Schedule (For a Kra Project of a Pass-Through Entity) - Kentucky

1

2