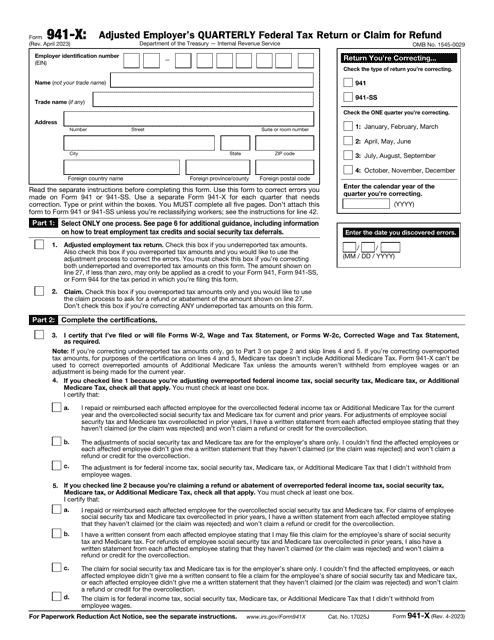

IRS Form 941-X Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund

What Is IRS Form 941-X?

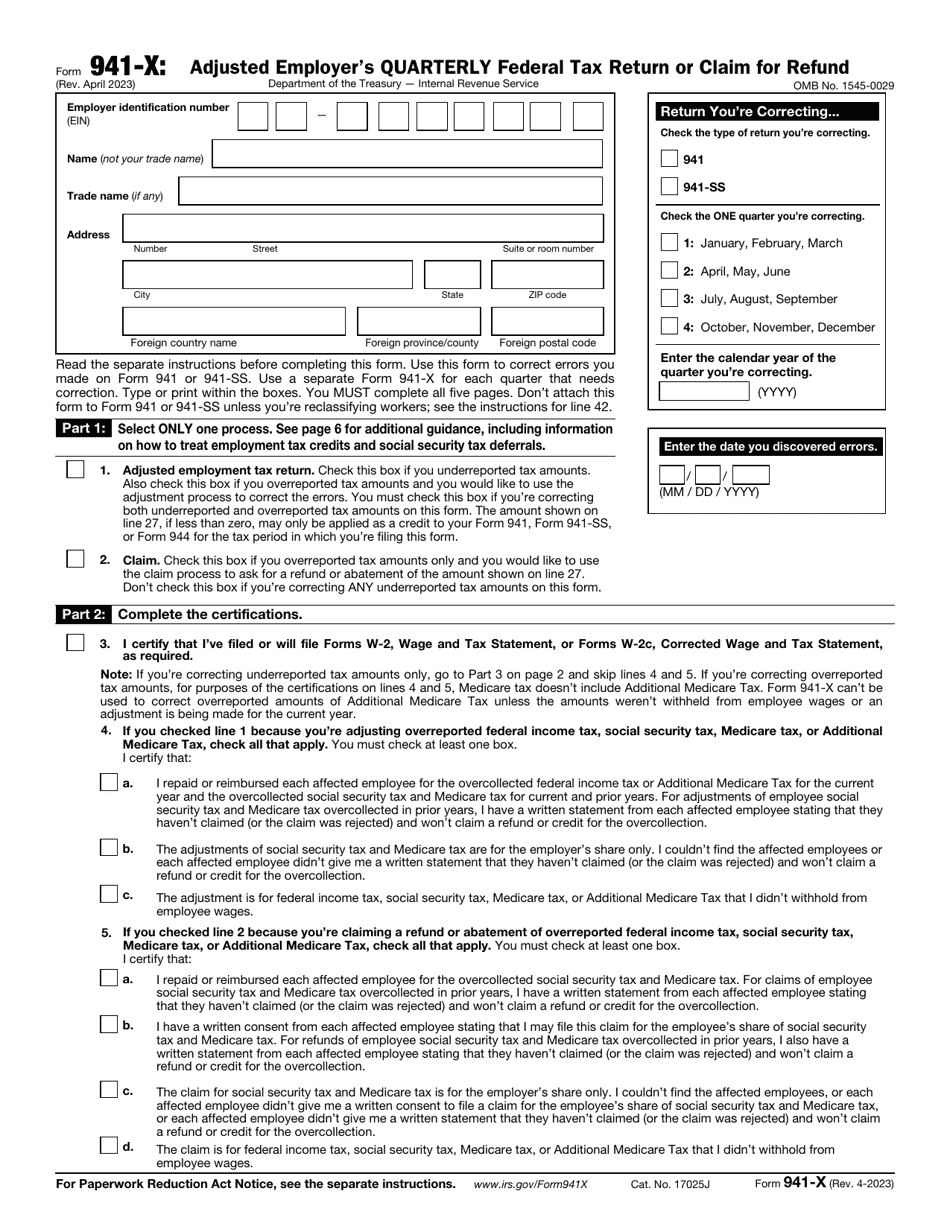

IRS Form 941-X, Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund , is a formal instrument used by taxpayers that need to fix the mistakes they have discovered upon filing IRS Form 941, Employer's Quarterly Federal Tax Return.

Alternate Name:

- Tax Form 941-X.

Employers have an opportunity to correct the numbers they have submitted to tax organs - from wages and compensation to tax and tax credits - and outline wages and taxes that relate to certain quarters of the year if they failed to treat their workers as employees. Additionally, the employer should prepare this form to request a refund if they paid too much tax after making an error during the process of computations.

This document was released by the Internal Revenue Service (IRS) on April 1, 2023 , making older editions of the form outdated. You can find an IRS Form 941-X fillable version below.

Check out the IRS 941 Series of forms to see more documents in this series.

Form 941-X Instructions

The IRS Form 941-X Instructions are as follows:

-

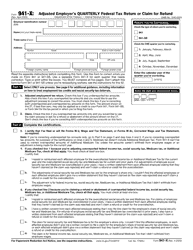

List the details of your business - the employer identification number, the name of your company, and its correspondence address . Check the appropriate boxes to specify what type of return you are amending and what quarter is described in the form you previously filed. State the year recorded in the instrument and the date when you learned about an error.

-

Confirm you either overreported or underreported tax and verify you complied with the requirement to submit IRS Form W-2, Wage and Tax Statement . Elaborate on potential reimbursement your employees got if necessary or state the adjustments or the claim did not affect anyone's wages.

-

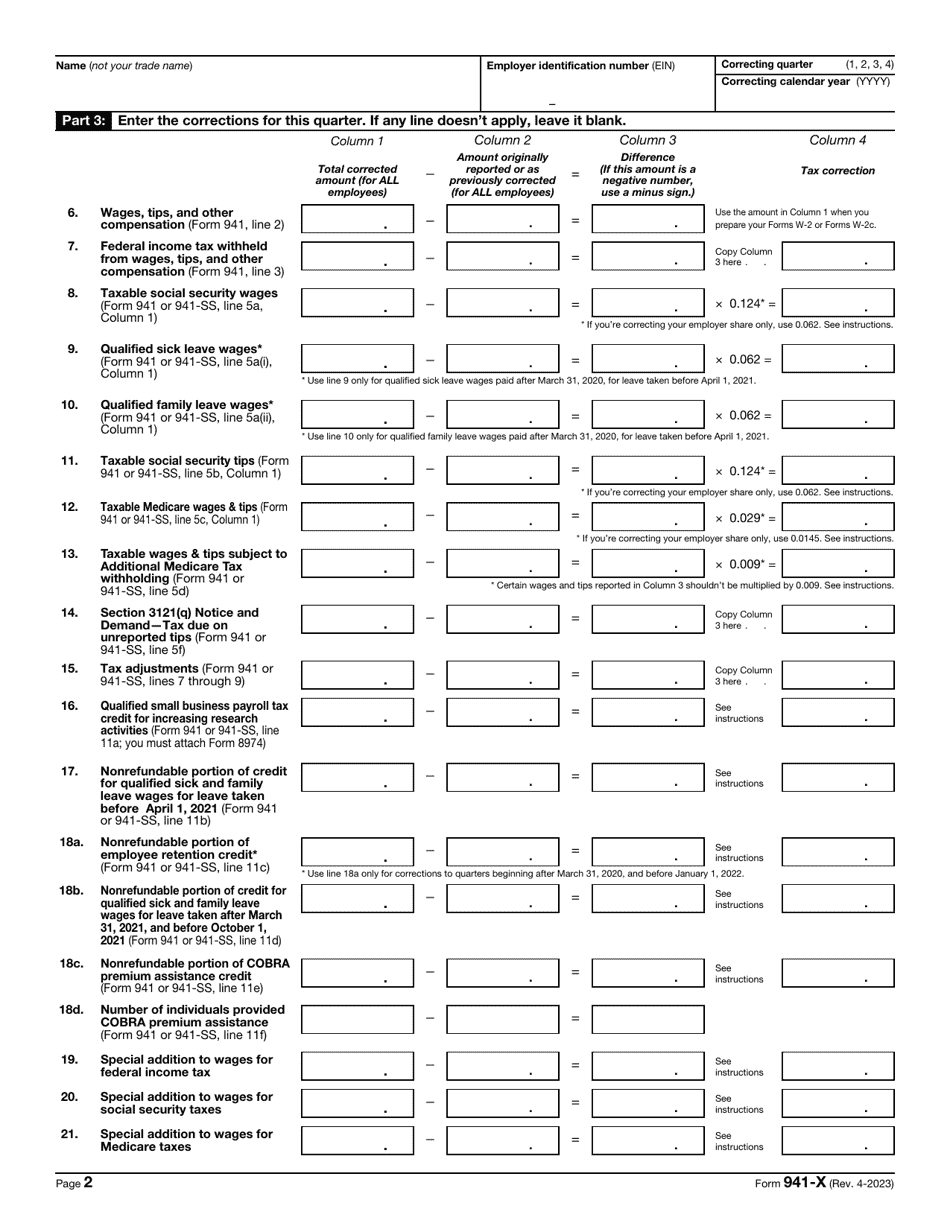

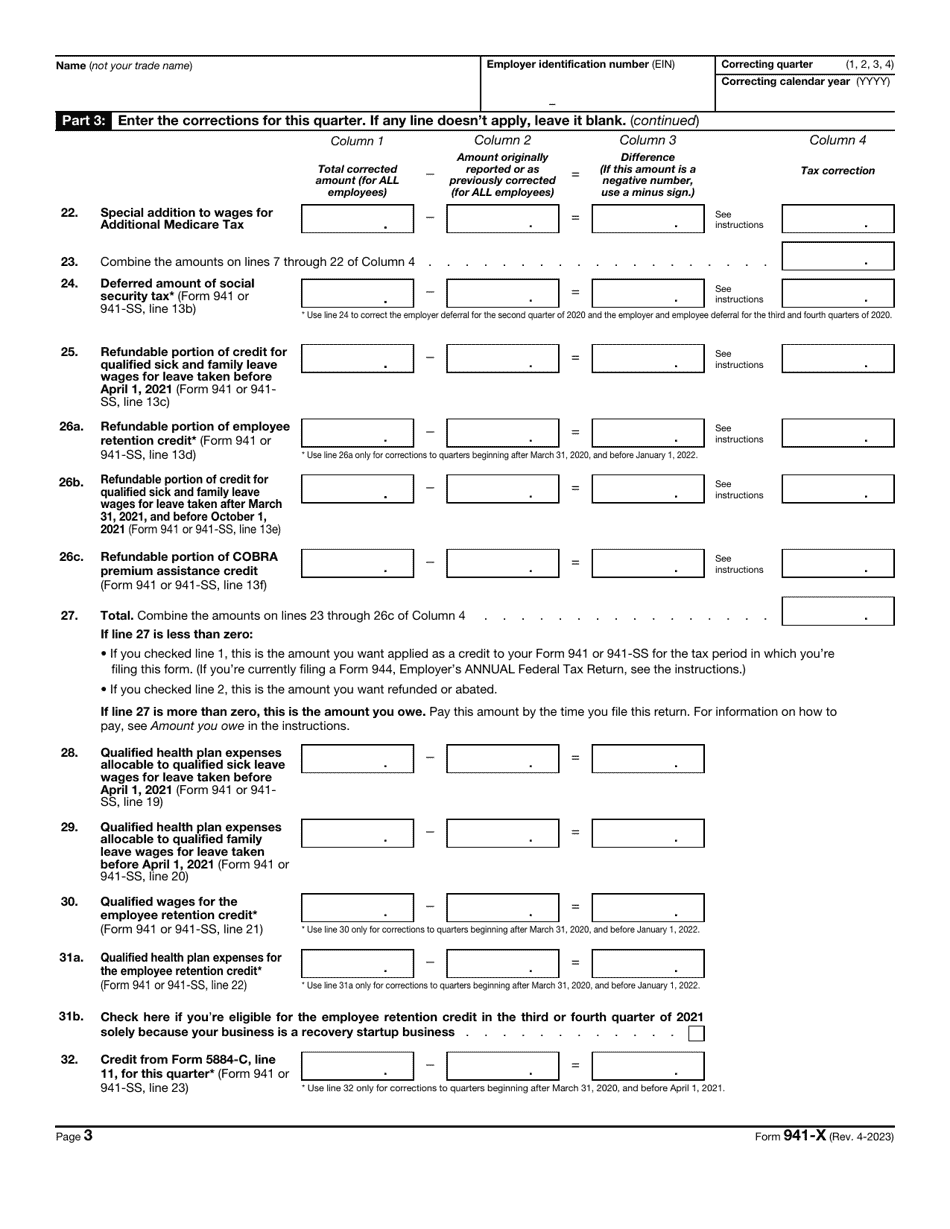

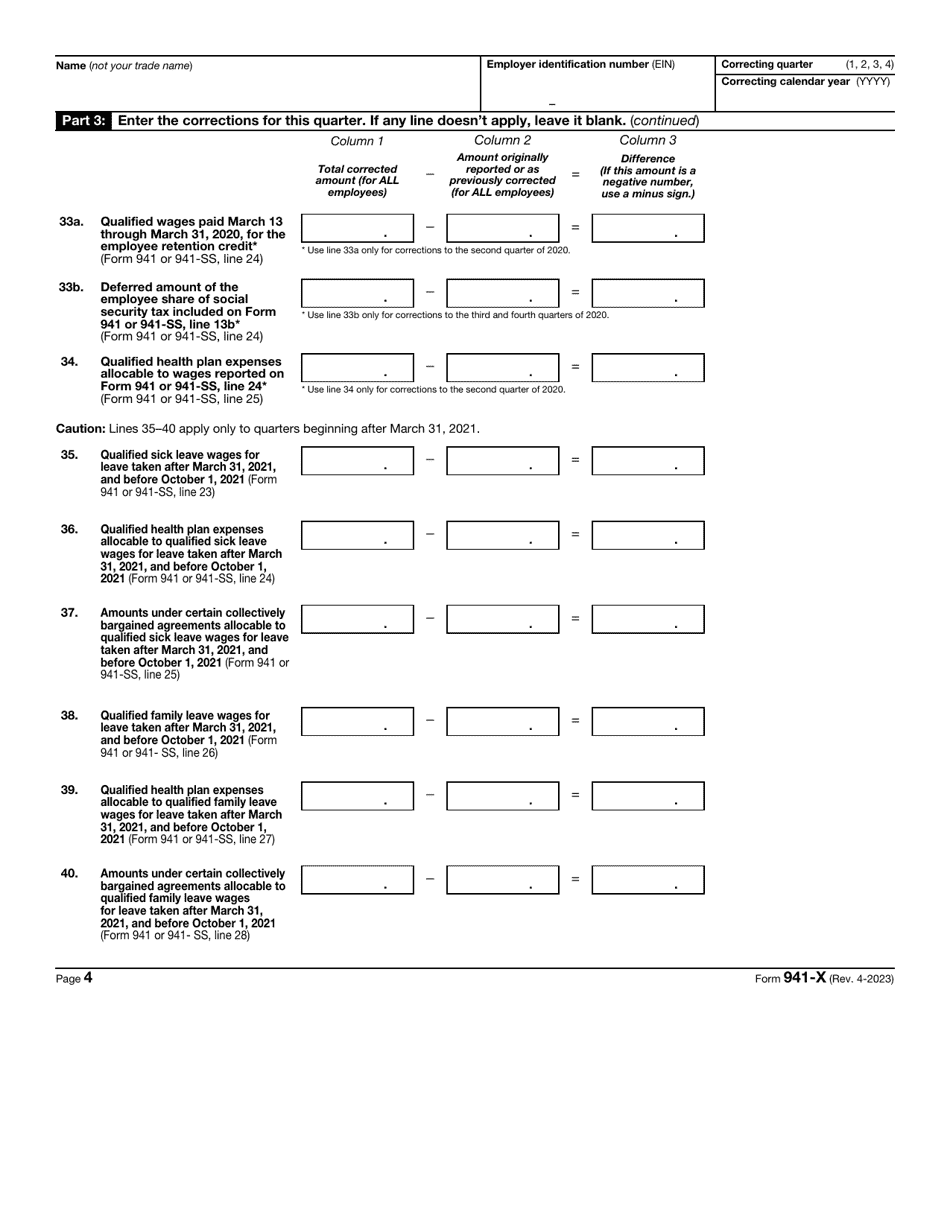

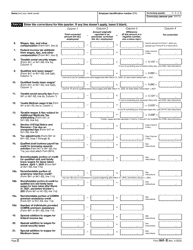

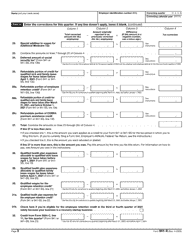

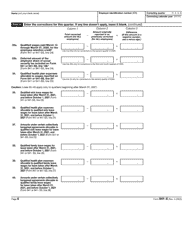

Proceed with corrections . You will have to indicate the mistake and calculate the difference between the amounts you submitted earlier. Skip the fields that do not apply to you even if the purpose of the form is to fix only one error.

-

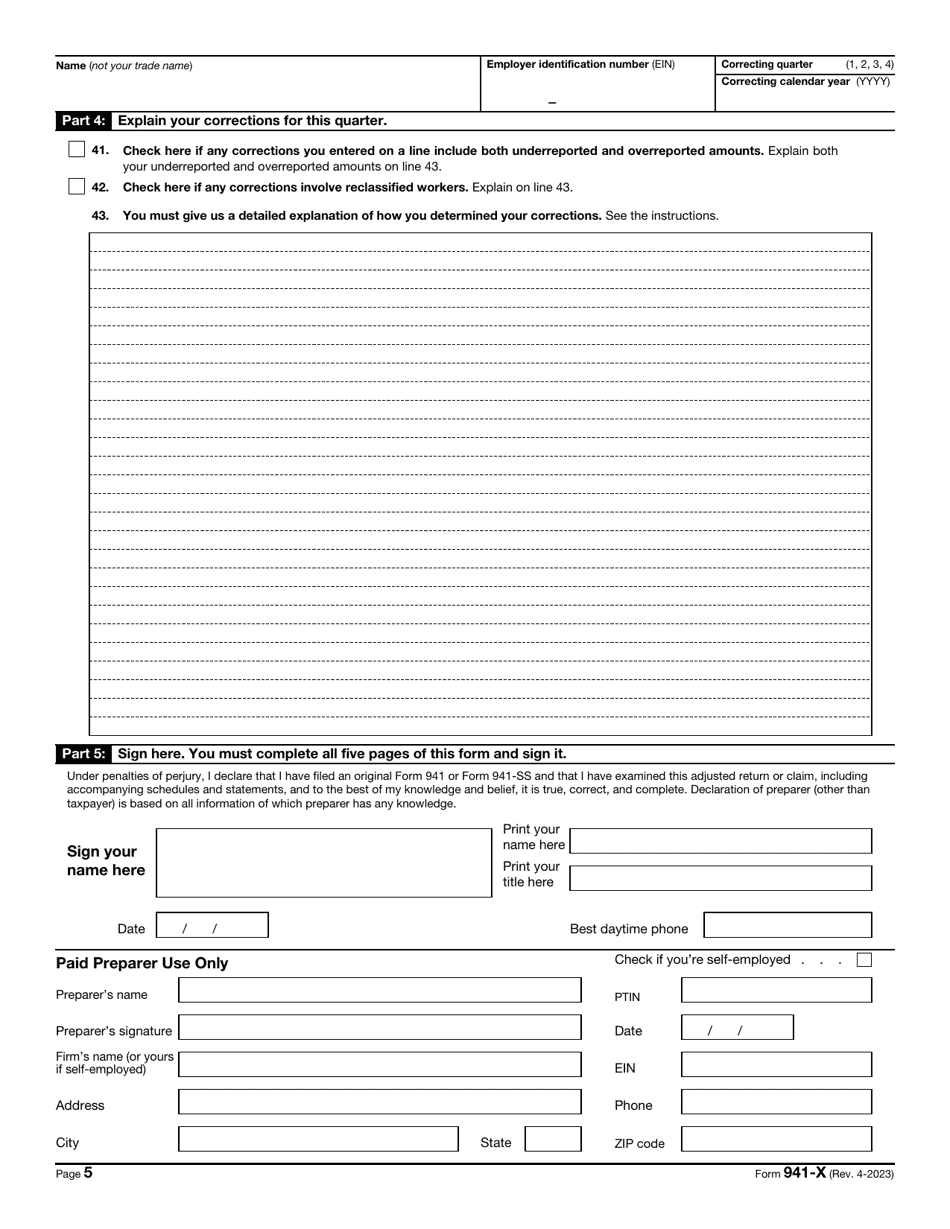

Put a tick in the appropriate box to inform fiscal authorities about both overreported and underreported amounts as well as to certify the modifications affect reclassified workers . Use the remarks section to provide a comprehensive explanation of your amendments to the statement you previously sent. It is possible you run out of space clarifying the issue - it is allowed to enclose extra sheets of paper if they are properly identified as an essential part of this document.

-

Certify the paperwork - add your name, title, and telephone number, enter the actual date, and sign the form . You may hire a tax professional to assist you with completing Form 941-X - in this case, they are obliged to provide their personal details and signature once the instrument is filled out.

To request a refund or abatement of arrested interest or penalties, an employer should use IRS Form 843, Claim for Refund and Request for Abatement. IRS Form 941-X cannot be used for these purposes.

When Is 941-X Due?

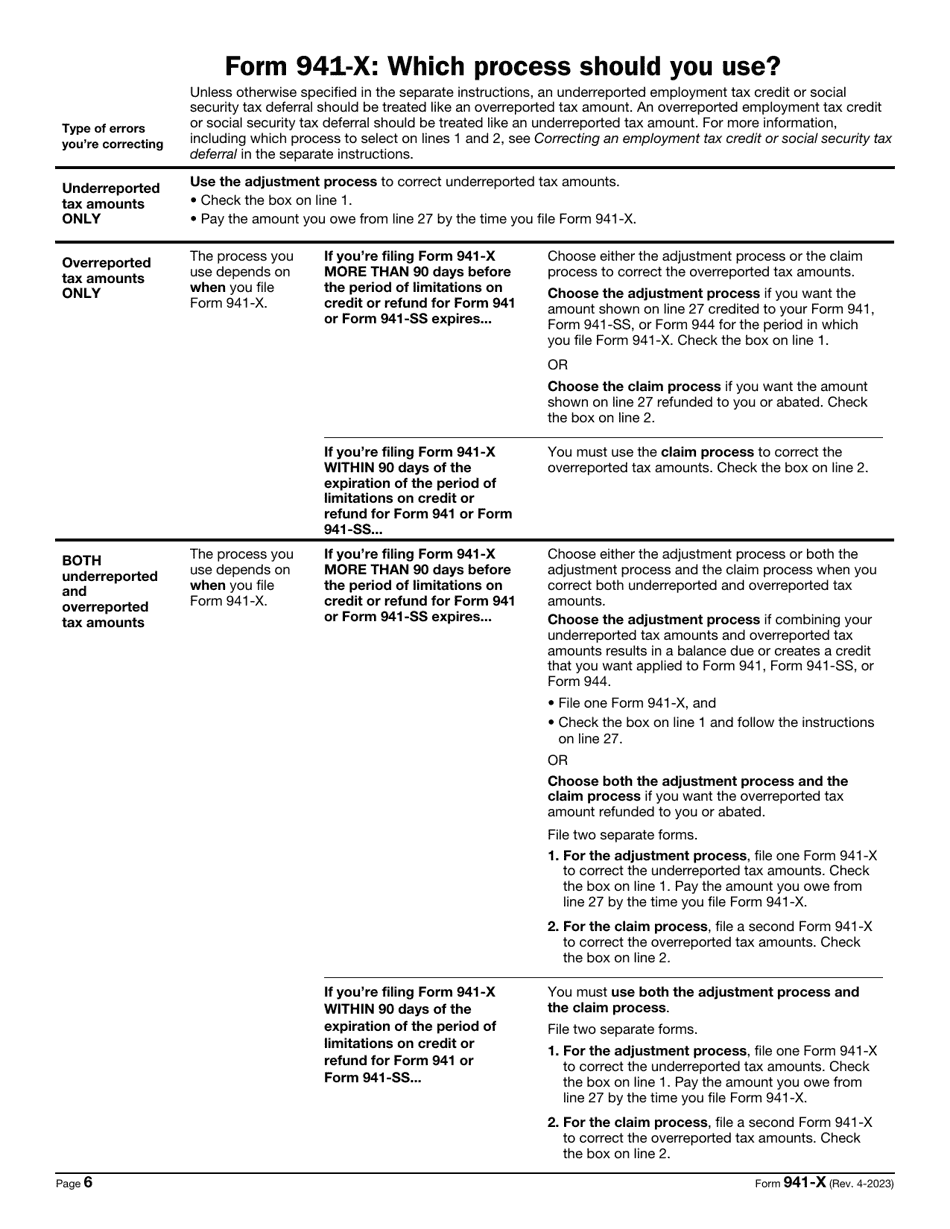

Over-reported taxes can be corrected within 2 years from the date when the over-reported taxes were paid or within 3 years from filing the form. Under-reported taxes should be corrected before the form due date for that quarter and the tax must be paid by the time the form is filed.

If the document is filed on time, under-reported taxes are paid by the time of filing, the grounds for corrections are explained in details and the date of error discovery is provided, the employer will not be subject to failure-to-pay penalties.

Where to Mail Form 941-X?

Employers must choose the correct 941-X Form mailing address - it depends on the status of the entity, the location of the filer, and the filing method:

-

If you are located in Alabama, Alaska, Arizona, Arkansas, California, Colorado, Hawaii, Idaho, Iowa, Kansas, Louisiana, Minnesota, Mississippi, Missouri, Montana, Nebraska, Nevada, New Mexico, North Dakota, Oklahoma, Oregon, South Dakota, Texas, Utah, Washington, or Wyoming, mail the documentation to the Department of the Treasury, Internal Revenue Service, Ogden, UT 84201-0005 .

-

Submit the form to the Department of the Treasury, Internal Revenue Service, Cincinnati, OH 45999-0005 in case you conduct your business in Connecticut, Delaware, District of Columbia, Florida, Georgia, Illinois, Indiana, Kentucky, Maine, Maryland, Massachusetts, Michigan, New Hampshire, New Jersey, New York, North Carolina, Ohio, Pennsylvania, Rhode Island, South Carolina, Tennessee, Vermont, Virginia, West Virginia, or Wisconsin.

-

Employers that do not have a main place of business established anywhere are supposed to file the paperwork with the Internal Revenue Service, P.O. Box 409101, Ogden, UT 84409 .

-

In case you prepare the instrument on behalf of a governmental entity or exempt organization, no matter where you are located, send the documentation to the Department of the Treasury, Internal Revenue Service, Ogden, UT 84201-0005 .

-

Taxpayers that prefer to use a private delivery service have to mail the form to the Ogden - Internal Revenue Submission Processing Center, 1973 Rulon White Blvd., Ogden, UT 84201 .

How to Correct Form 941-X?

If you discovered a mistake on your form, file another one, correcting the same form and mail it before the due date.

IRS 941-X Related Forms

- IRS Form 941, Employer's Quarterly Federal Tax Return is a form used to report Medicare, social security and income taxes withheld from the employee's paychecks and pay the employer's share of Medicare and social security taxes. This form is filed four times a year.

- IRS Form 941-SS, Employer's Quarterly Federal Tax Return - American Samoa, Guam, the Commonwealth of the Northern Mariana Islands, and the U.S. Virgin Islands is a form used for the same purpose as IRS Form 941, but is used by employers, located in the above-mentioned territories.

Download IRS Form 941-X Adjusted Employer's Quarterly Federal Tax Return or Claim for Refund

1

2

3

4

5

6