IRS 5500 Forms and Instructions

What Are 5500 Forms?

IRS 5500 Forms are used to report information about welfare and pension benefit plans, Direct Filing Entities, or DFEs (investment arrangements that manage funds from various plans), employee benefit plans, including one-participant plans and foreign plans. This series contains three forms:

-

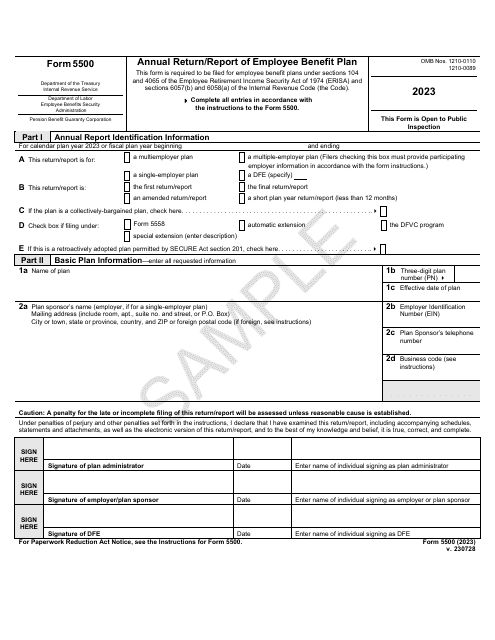

IRS Form 5500, Annual Return/Report of Employee Benefit Plan, is a document jointly released by the Internal Revenue Service (IRS) , the Department of Labor (DOL), and the Pension Benefit Guaranty Corporation (PBGC) and used by each sponsor or administrator of an employee benefit plan subject to the Employee Retirement Income Security Act of 1974 (ERISA) every year.

-

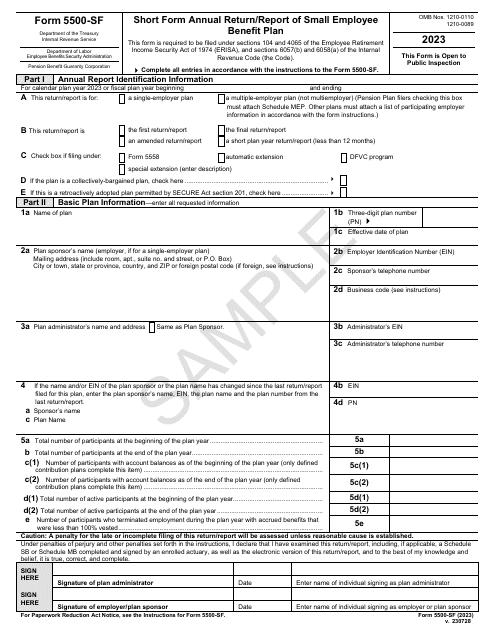

IRS Form 5500-SF, Short Form Annual Return/Report of Small Employee Benefit Plan, is a related simplified form issued by the IRS, the DOL, and the PBGC and used by certain welfare and pension benefit plans. There are several requirements for the plan to be eligible to use this form:

- Have fewer than 100 plan participants at the beginning of the year;

- Not hold employer securities;

- Not be a multiemployer plan;

- Not be required to file Form M-1, Report for Multiple Employer Welfare Arrangements (MEWAs) and Certain Entities Claiming Exception (ECEs); and

- Be exempt from the audit by an independent qualified public accountant.

-

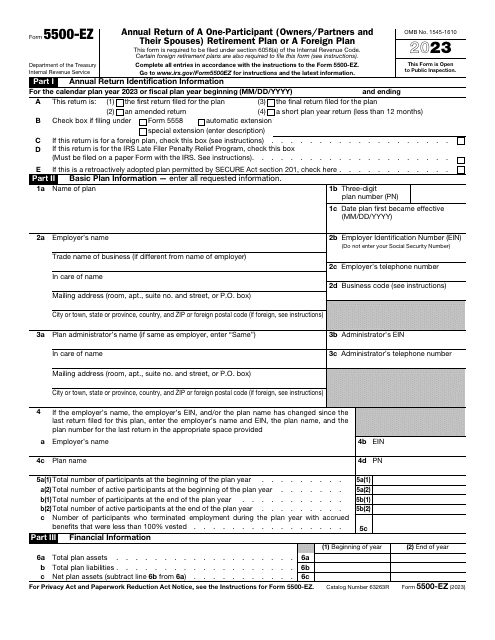

IRS Form 5500-EZ, Annual Return of a One-Participant (Owners/Partners and Their Spouses) Retirement Plan or A Foreign Plan, is a document issued by the IRS used by one-participant plans and foreign plans that have to file an annual return and do not file it electronically on a related Form 5500-SF.

Who Completes 5500 Forms?

Employee benefit plan tax returns must be completed by the employer maintaining the plan or the plan administrator of a welfare/pension benefit plan covered by ERISA. Form 5500-SF is filed when the plan has fewer than 100 participants. Form 5500-EZ is used for foreign plans and one-participant plans. A return must be filed every year for every welfare/pension benefit plan, and for every entity that files as the DFE.

When Are Forms 5500 Due?

Form 5500 and Form 5500-SF due date is the last day of the seventh month after the end of the plan year . Both forms cannot be filed by mail or another delivery service, they must be submitted and signed electronically. It is possible to extend the deadline by filing Form 5558, Application for Extension of Time to File Certain Employee Plan Returns, therefore, submitting the report of employee benefit plan 2,5 months later. There is a penalty for late filing from the IRS and the DOL: $25 per day and $1100 per day respectively.

Form 5500-EZ due date is also the last day of the seventh calendar month after the end of the plan year. The form must be filed on paper. The mailing address for the form: Department of Treasury, Internal Revenue Service, Ogden, UT 84201-0020. The IRS imposes a penalty of $25 per day for not filing this return.

Documents:

5

This form should be filled out by one-participant plans and by foreign plans. You are not required to file the form with attachments or schedules. File this form for an annual return if you do not file it electronically on a related Form 5500-SF.

This document was issued by the Internal Revenue Service (IRS), the Department of Labor (DOL), and the Pension Benefit Guaranty Corporation (PBGC). It is a formal instrument used by employers that manage the employee benefit program to inform the authorities about the qualifications of the plan, investments made to the plan, and financial details of the program.