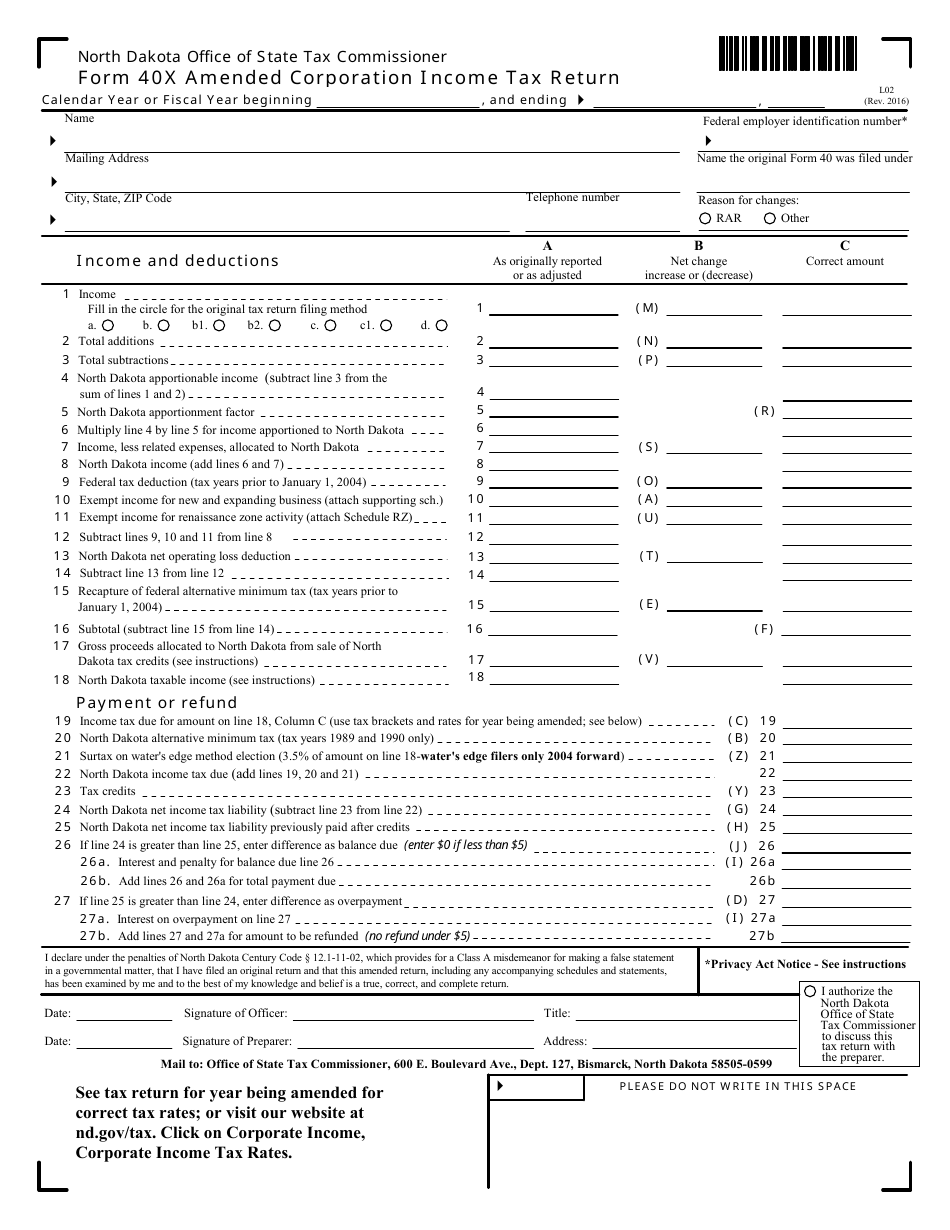

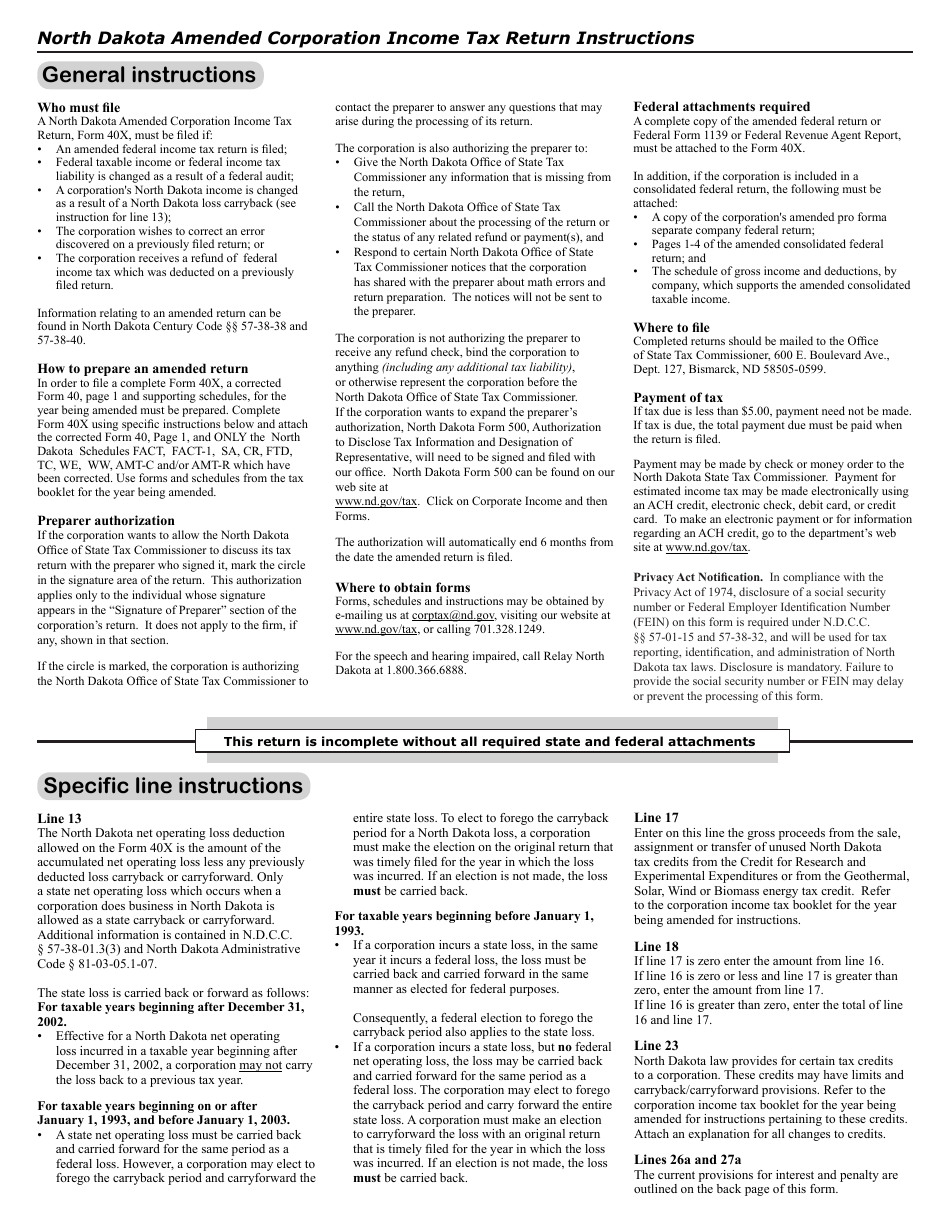

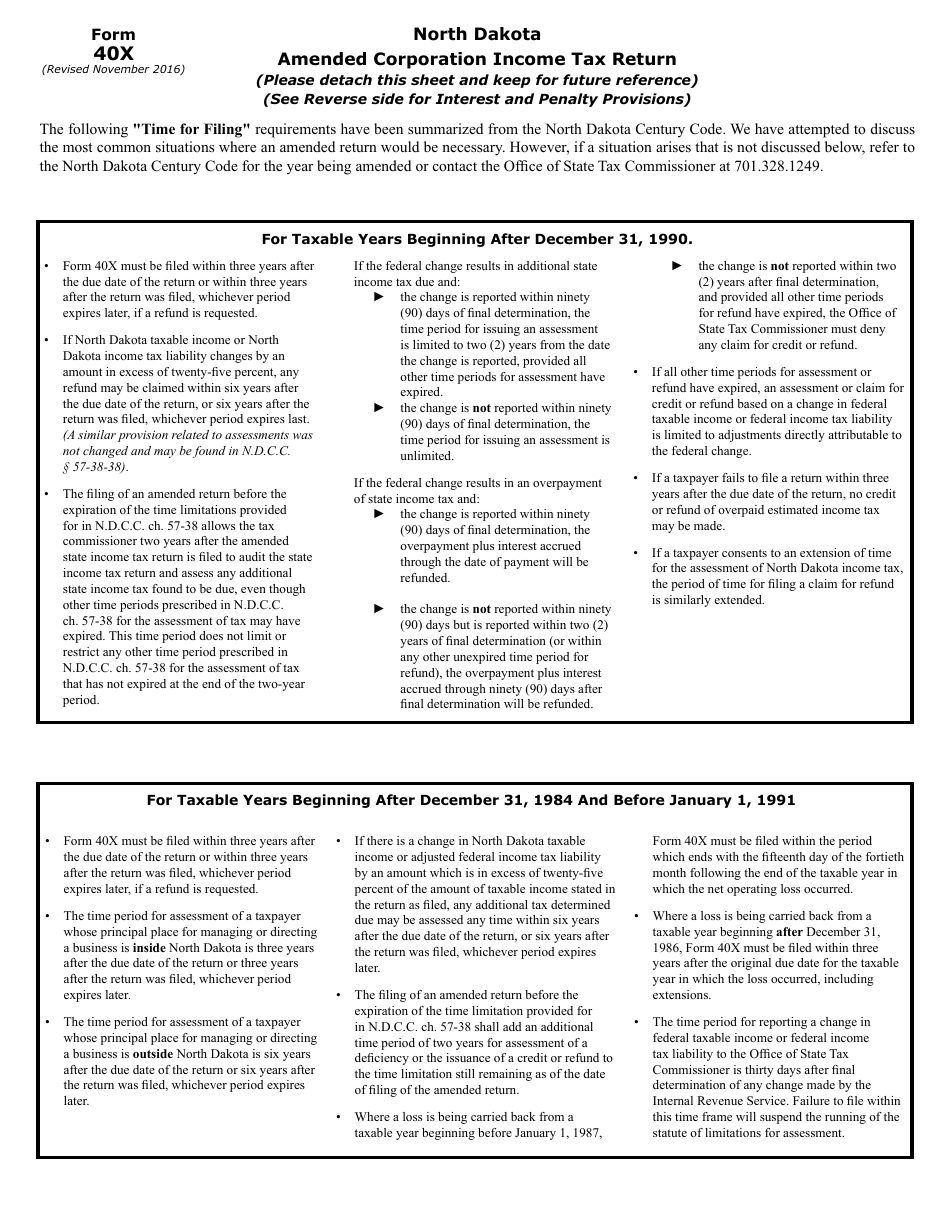

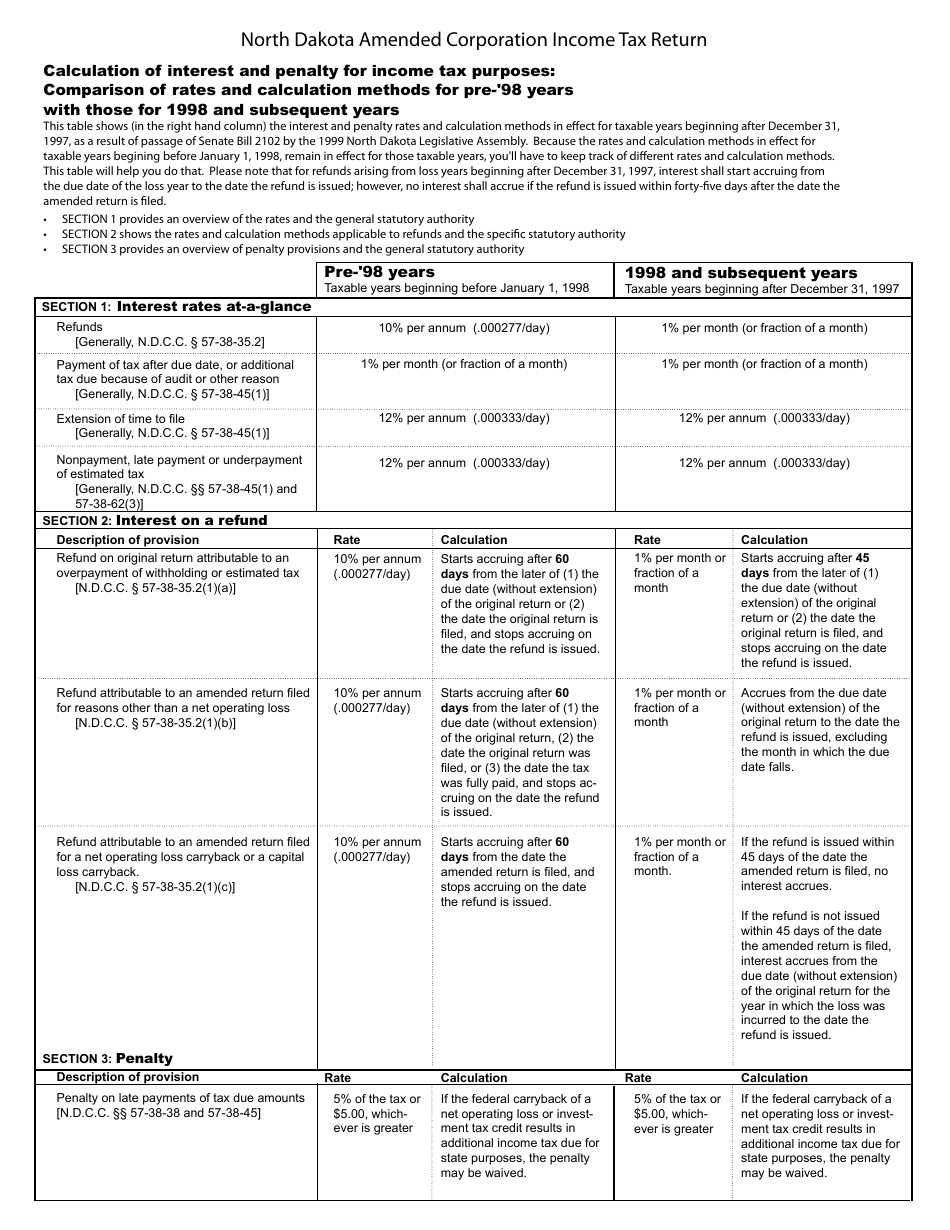

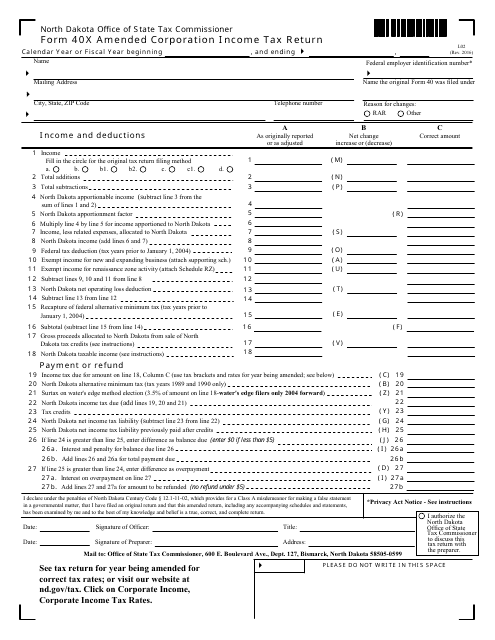

Form L02 (40X) Amended Corporation Income Tax Return - North Dakota

What Is Form L02 (40X)?

This is a legal form that was released by the North Dakota Office of State Tax Commissioner - a government authority operating within North Dakota. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form L02 (40X)?A: Form L02 (40X) is the Amended Corporation Income Tax Return for North Dakota.

Q: Who should file Form L02 (40X)?A: Corporations that need to amend their original North Dakota Corporation Income Tax Return should file Form L02 (40X).

Q: What information do I need to complete Form L02 (40X)?A: You will need the information from your original North Dakota Corporation Income Tax Return, as well as any additional information related to the amendments being made.

Q: Are there any special instructions for completing Form L02 (40X)?A: Yes, there may be special instructions depending on the nature of the amendments being made. It is important to carefully read the instructions provided with the form.

Q: Is there a deadline for filing Form L02 (40X)?A: Yes, the deadline for filing Form L02 (40X) is generally the same as the deadline for filing the original North Dakota Corporation Income Tax Return.

Q: What should I do if I have additional questions about Form L02 (40X)?A: If you have additional questions about Form L02 (40X), you should contact the North Dakota Office of State Tax Commissioner for assistance.

Form Details:

- Released on November 1, 2016;

- The latest edition provided by the North Dakota Office of State Tax Commissioner;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form L02 (40X) by clicking the link below or browse more documents and templates provided by the North Dakota Office of State Tax Commissioner.

Download Form L02 (40X) Amended Corporation Income Tax Return - North Dakota

1

2

3

4