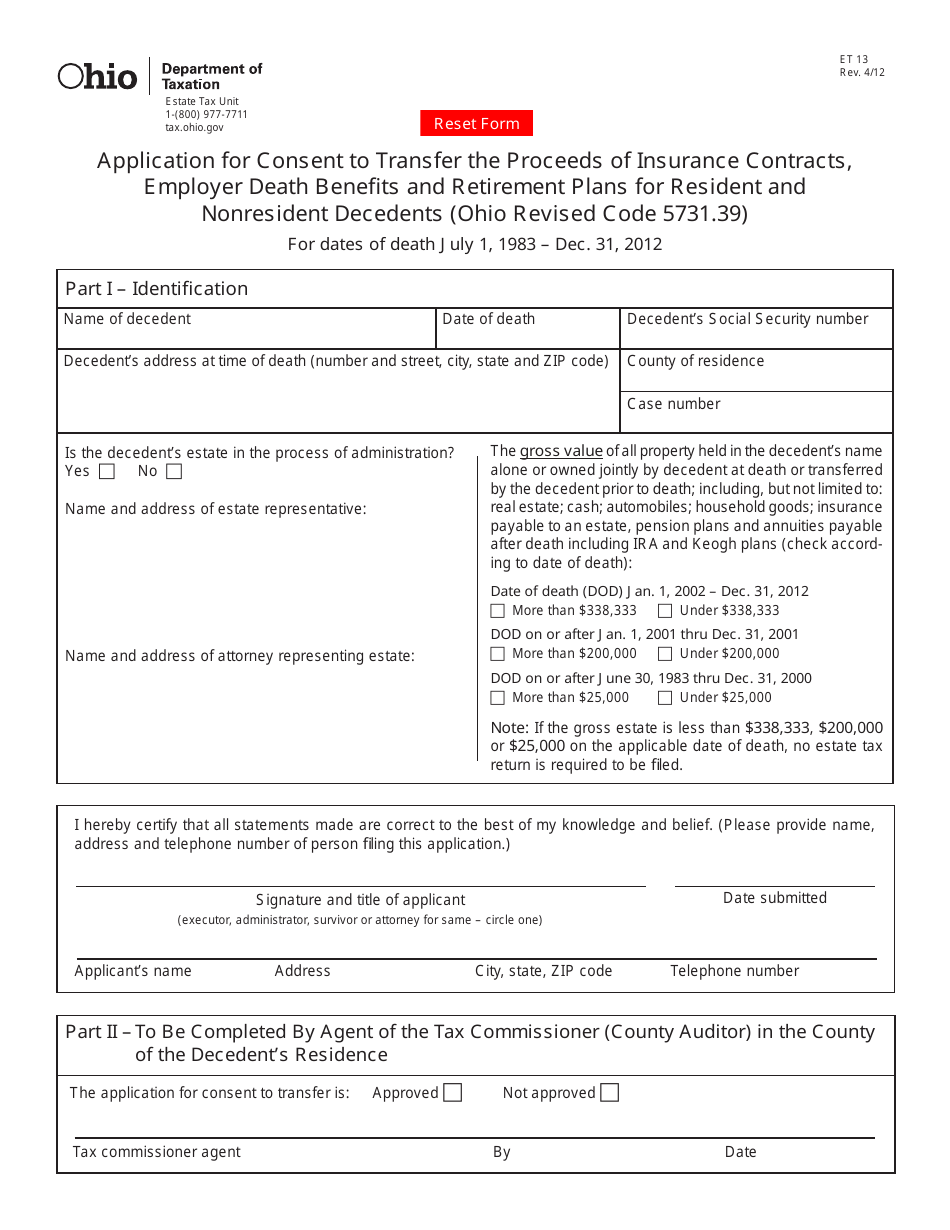

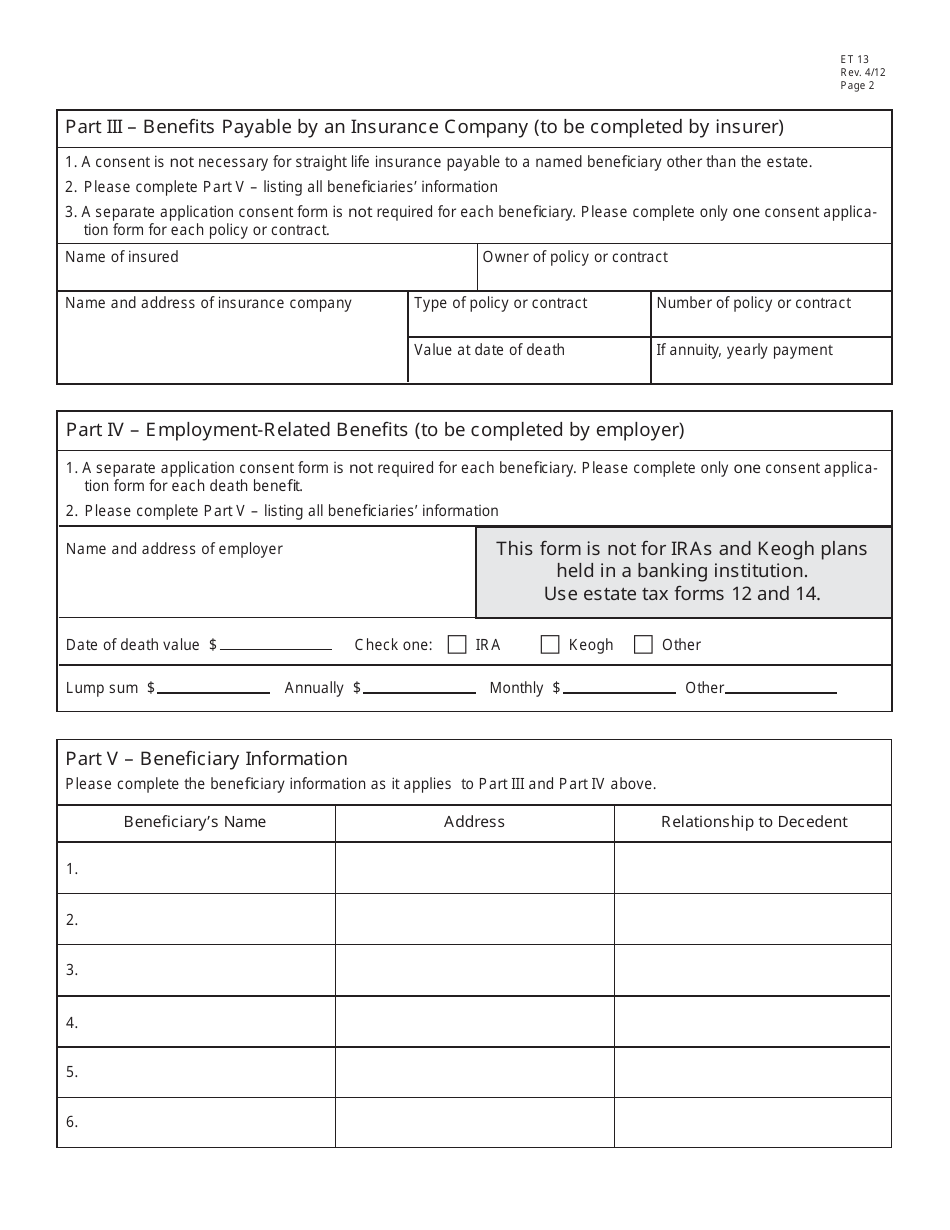

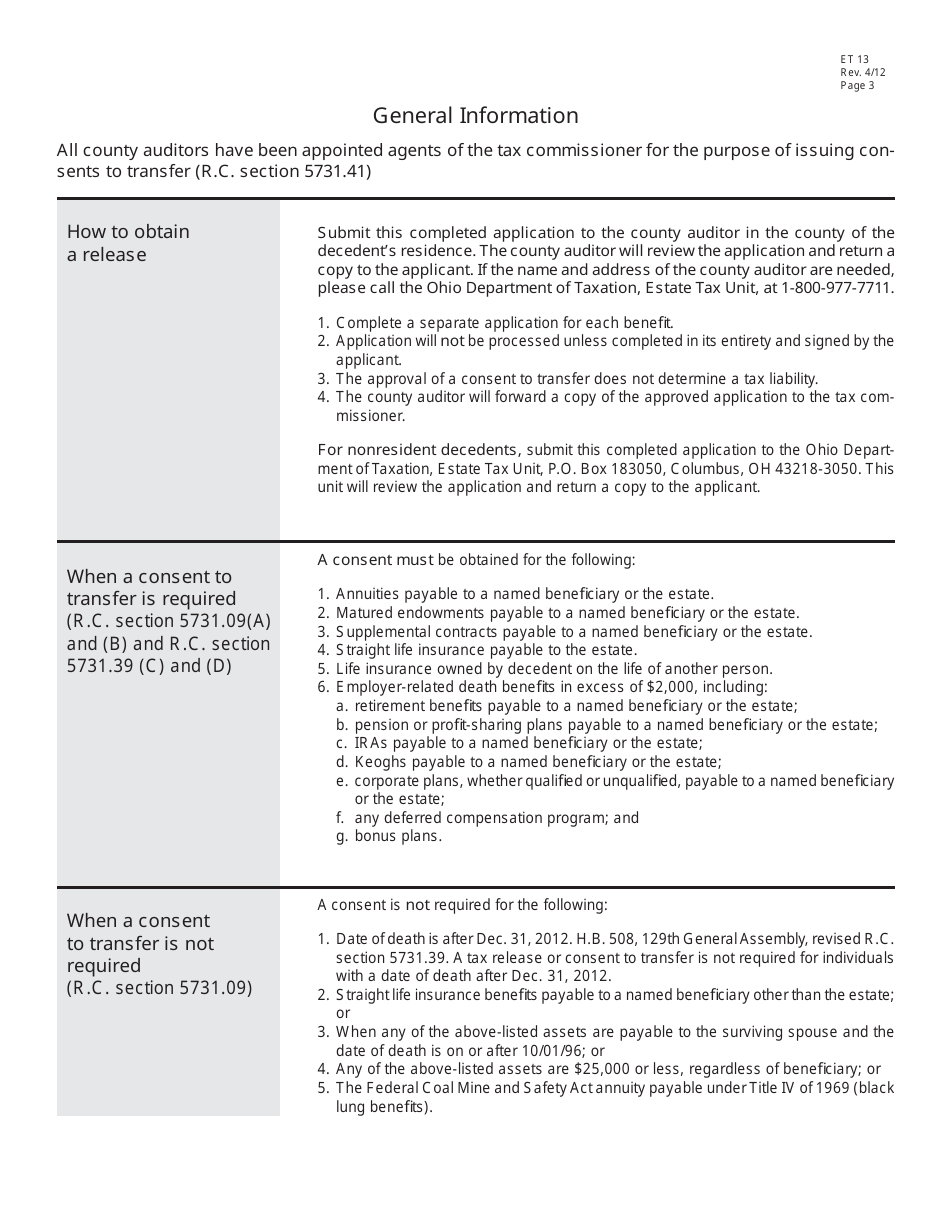

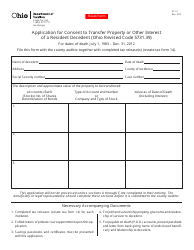

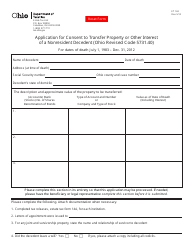

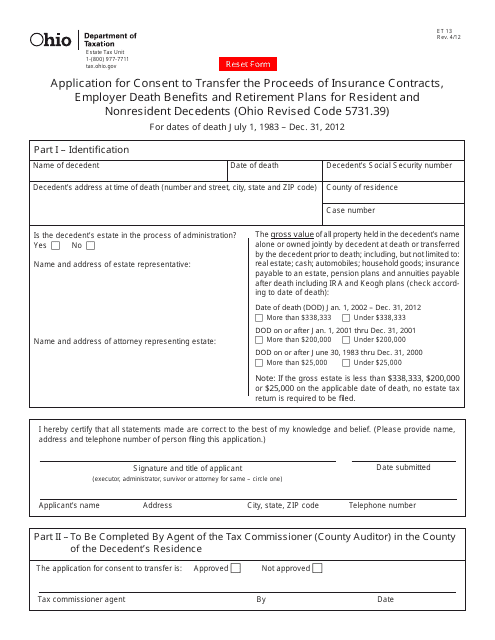

Form ET13 Application for Consent to Transfer the Proceeds of Insurance Contracts, Employer Death Benefits and Retirement Plans for Resident and Nonresident Decedents - Ohio

What Is Form ET13?

This is a legal form that was released by the Ohio Department of Taxation - a government authority operating within Ohio. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form ET13?

A: Form ET13 is an application for consent to transfer the proceeds of insurance contracts, employer death benefits, and retirement plans for resident and nonresident decedents in Ohio.

Q: Who needs to file Form ET13?

A: Anyone who needs to transfer the proceeds of insurance contracts, employer death benefits, and retirement plans for a deceased person in Ohio.

Q: What is the purpose of Form ET13?

A: The purpose of Form ET13 is to obtain consent from the Ohio Department of Taxation for the transfer of these proceeds.

Q: Are there any fees associated with filing Form ET13?

A: Yes, there may be fees associated with filing Form ET13. You should consult the instructions or contact the Ohio Department of Taxation for more information.

Q: What supporting documents are required with Form ET13?

A: The specific supporting documents required may vary depending on the situation. You should refer to the instructions provided with Form ET13 or contact the Ohio Department of Taxation for guidance.

Q: What is the deadline for filing Form ET13?

A: The deadline for filing Form ET13 may vary depending on the circumstances. You should consult the instructions or contact the Ohio Department of Taxation for specific deadlines.

Form Details:

- Released on April 1, 2012;

- The latest edition provided by the Ohio Department of Taxation;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form ET13 by clicking the link below or browse more documents and templates provided by the Ohio Department of Taxation.

Download Form ET13 Application for Consent to Transfer the Proceeds of Insurance Contracts, Employer Death Benefits and Retirement Plans for Resident and Nonresident Decedents - Ohio

1

2

3