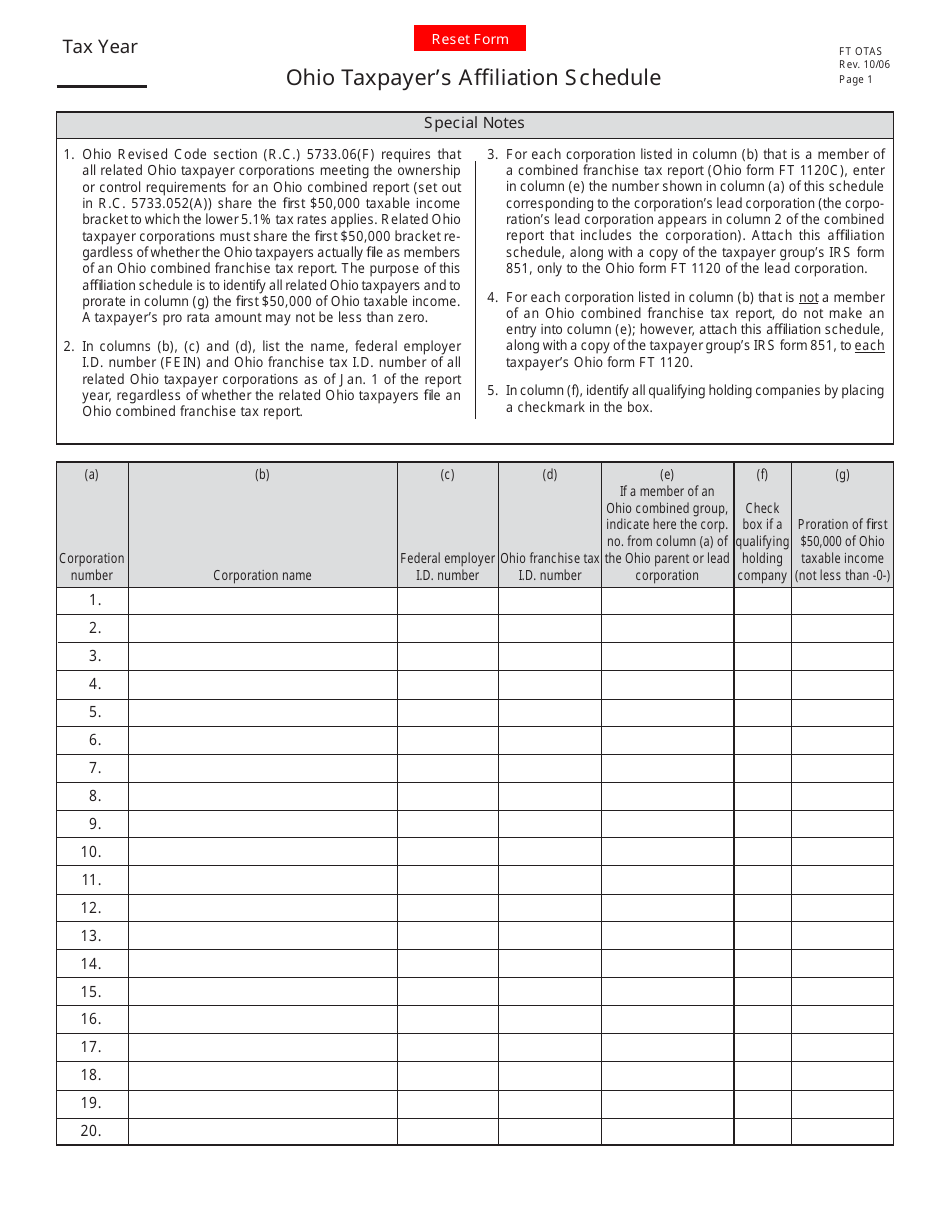

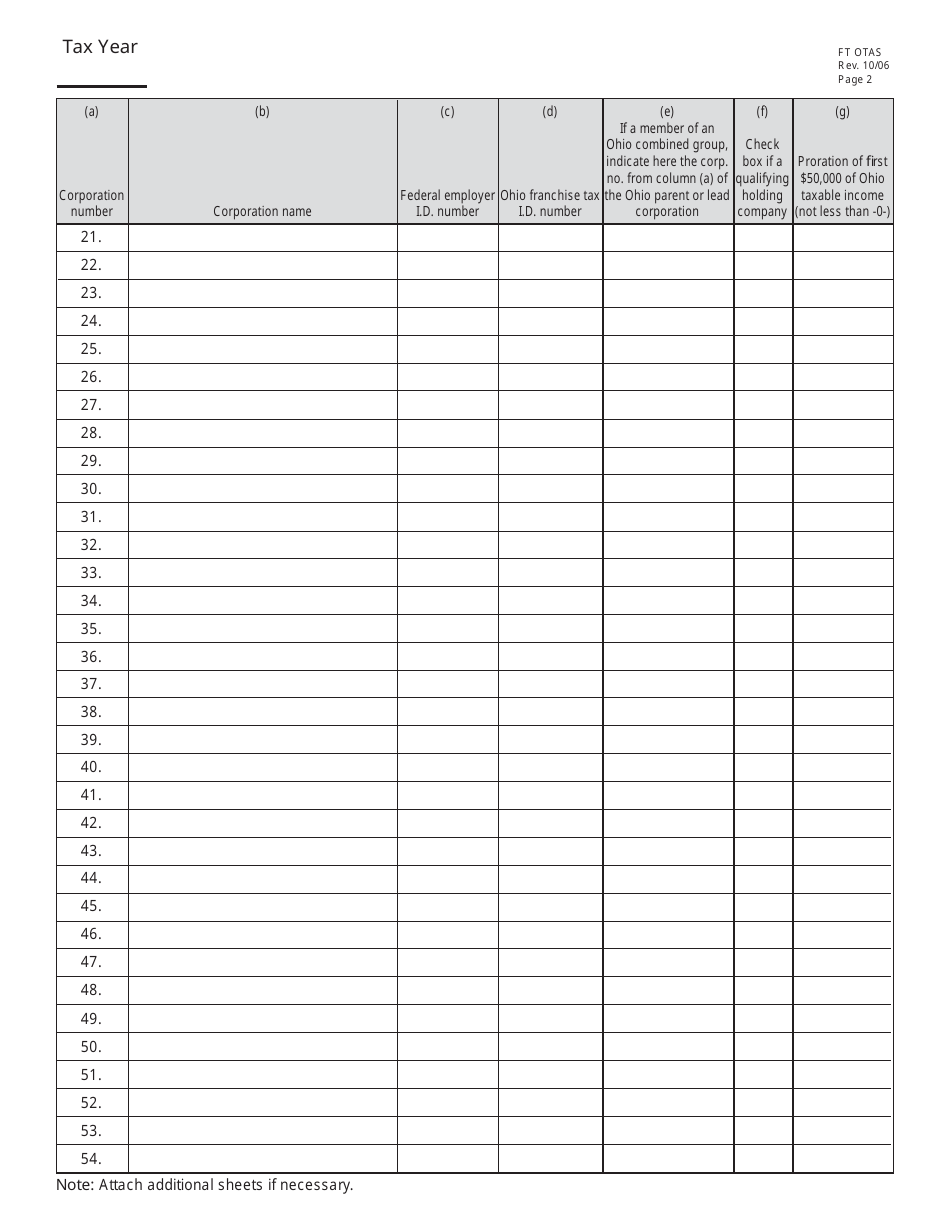

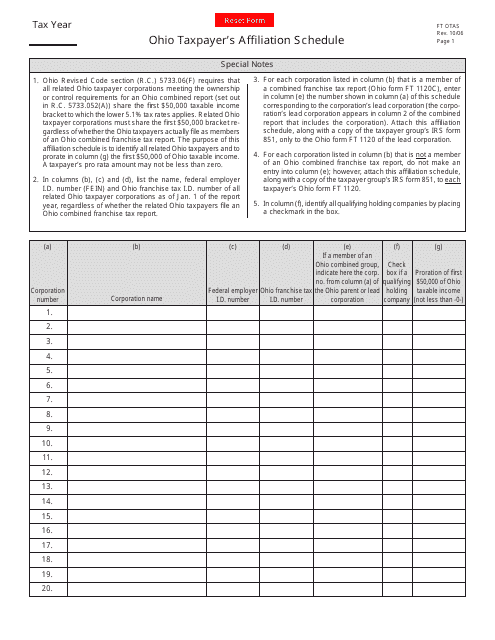

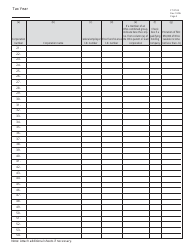

Form FT OTAS Ohio Taxpayer's Affiliation Schedule - Ohio

What Is Form FT OTAS?

This is a legal form that was released by the Ohio Department of Taxation - a government authority operating within Ohio. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is the FT OTAS Ohio Taxpayer's Affiliation Schedule?

A: The FT OTAS Ohio Taxpayer's Affiliation Schedule is a form used by Ohio taxpayers to report their business affiliations.

Q: Who needs to file the FT OTAS Ohio Taxpayer's Affiliation Schedule?

A: Ohio taxpayers who have business affiliations that need to be reported must file this form.

Q: What information is required on the FT OTAS Ohio Taxpayer's Affiliation Schedule?

A: The form requires information about the taxpayer's business affiliations, including the name and address of the affiliate and the percentage of ownership.

Q: When is the deadline for filing the FT OTAS Ohio Taxpayer's Affiliation Schedule?

A: The deadline for filing the form is the same as the deadline for filing your Ohio income tax return, usually April 15th.

Q: What happens if I don't file the FT OTAS Ohio Taxpayer's Affiliation Schedule?

A: Failure to file the form or providing incomplete or inaccurate information may result in penalties and interest charges.

Form Details:

- Released on October 1, 2006;

- The latest edition provided by the Ohio Department of Taxation;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form FT OTAS by clicking the link below or browse more documents and templates provided by the Ohio Department of Taxation.

Download Form FT OTAS Ohio Taxpayer's Affiliation Schedule - Ohio

1

2