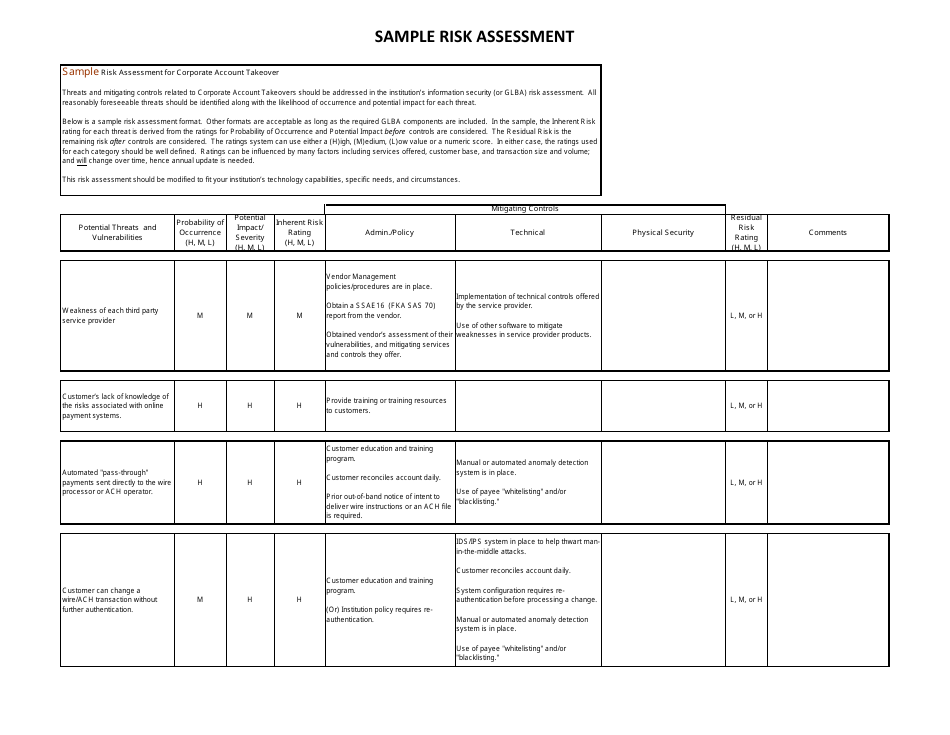

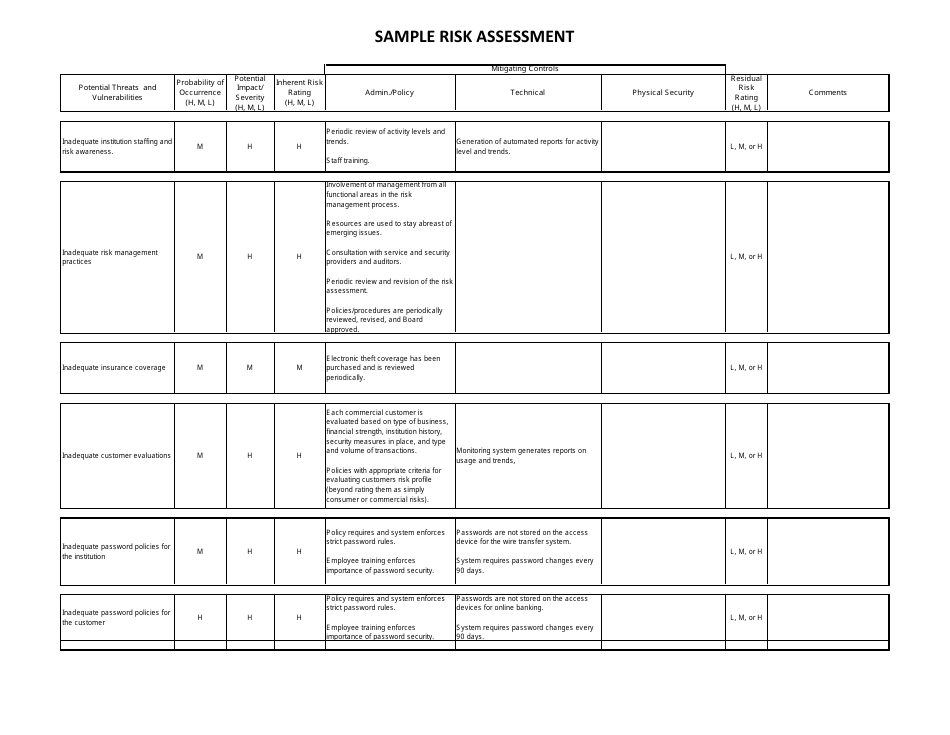

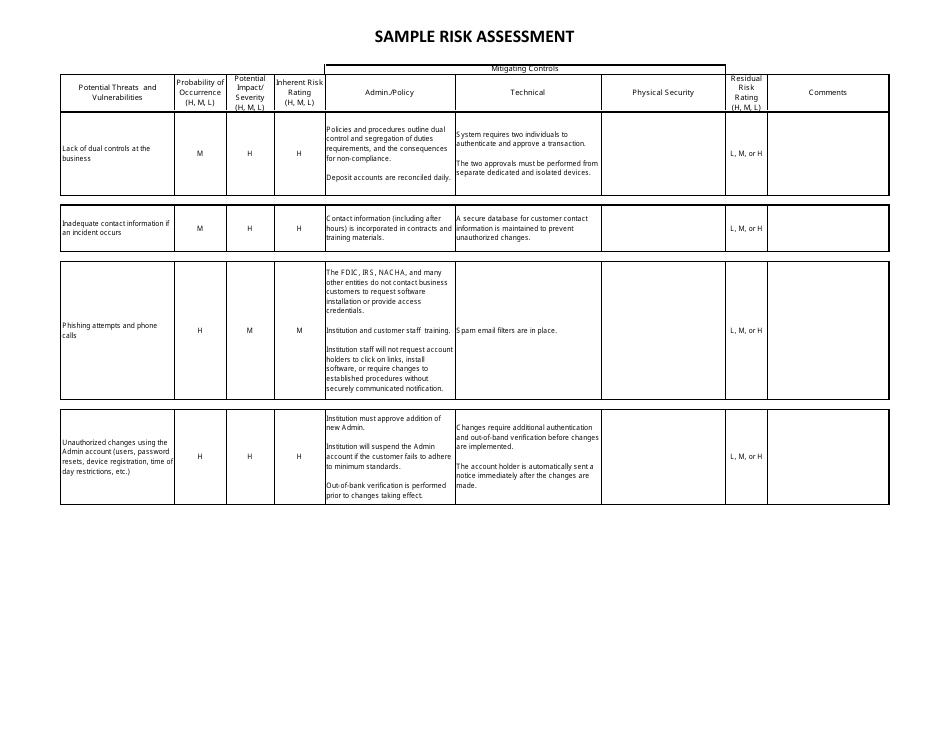

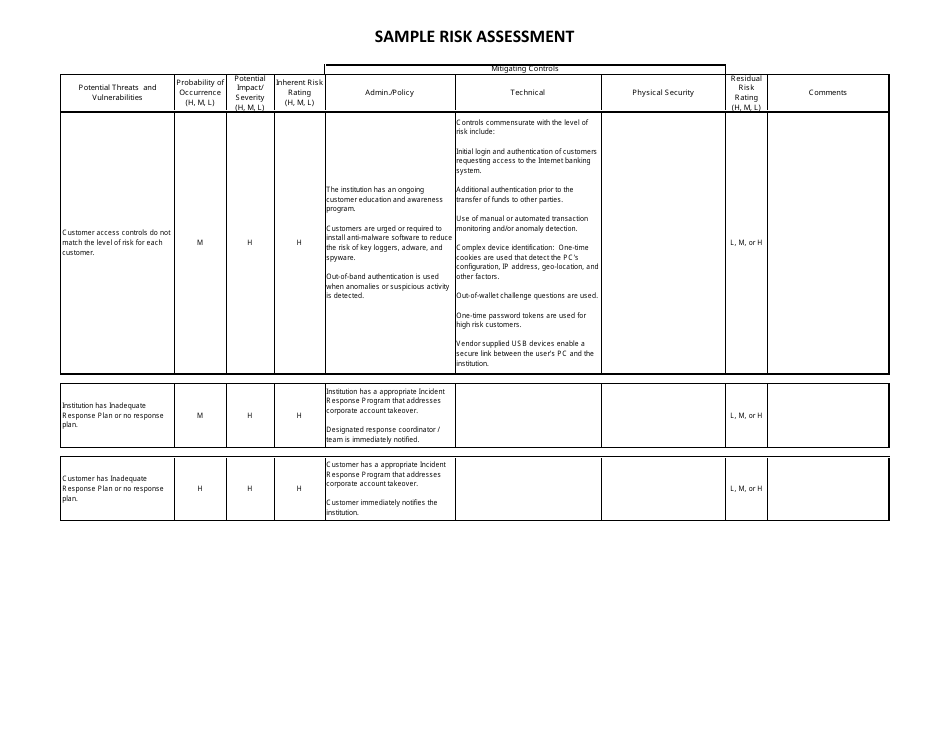

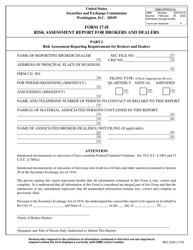

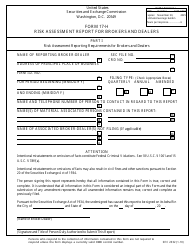

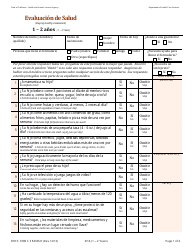

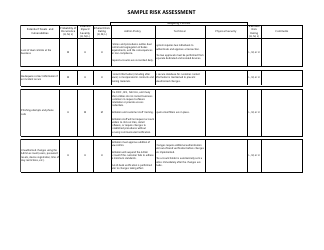

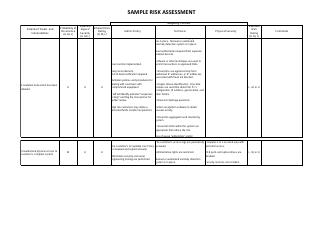

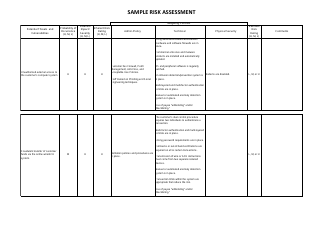

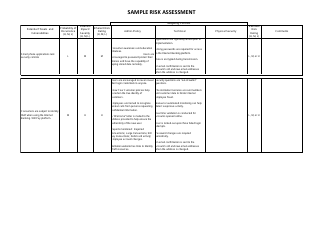

Sample Risk Assessment Form - California

Risk Assessment Form is a legal document that was released by the California Department of Financial Protection and Innovation - a government authority operating within California.

FAQ

Q: What is a risk assessment form?

A: A risk assessment form is a document used to identify and evaluate potential risks and hazards in a specific situation or area.

Q: Why is a risk assessment form important?

A: A risk assessment form is important because it helps minimize risks, prevent accidents, and ensure the safety of individuals and the environment.

Q: Who uses a risk assessment form?

A: A risk assessment form is used by individuals, businesses, and organizations to assess and manage risks.

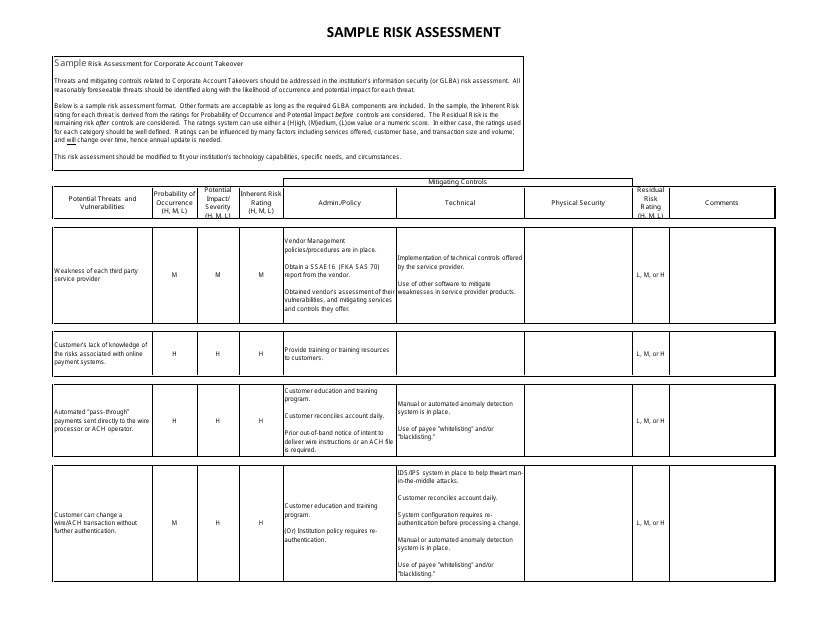

Q: What are the components of a risk assessment form?

A: A risk assessment form typically includes sections for identifying hazards, evaluating risks, implementing control measures, and monitoring and reviewing the effectiveness of those measures.

Q: How often should a risk assessment form be reviewed?

A: A risk assessment form should be reviewed regularly, especially when there are changes to the situation or environment that may introduce new risks.

Q: Is a risk assessment form required by law?

A: In some cases, a risk assessment form may be required by law, particularly in certain industries or for specific activities that involve potential hazards.

Form Details:

- The latest edition currently provided by the California Department of Financial Protection and Innovation;

- Ready to use and print;

- Easy to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of the form by clicking the link below or browse more documents and templates provided by the California Department of Financial Protection and Innovation.

Download Sample Risk Assessment Form - California

1

2

3

4

5

6

7

8