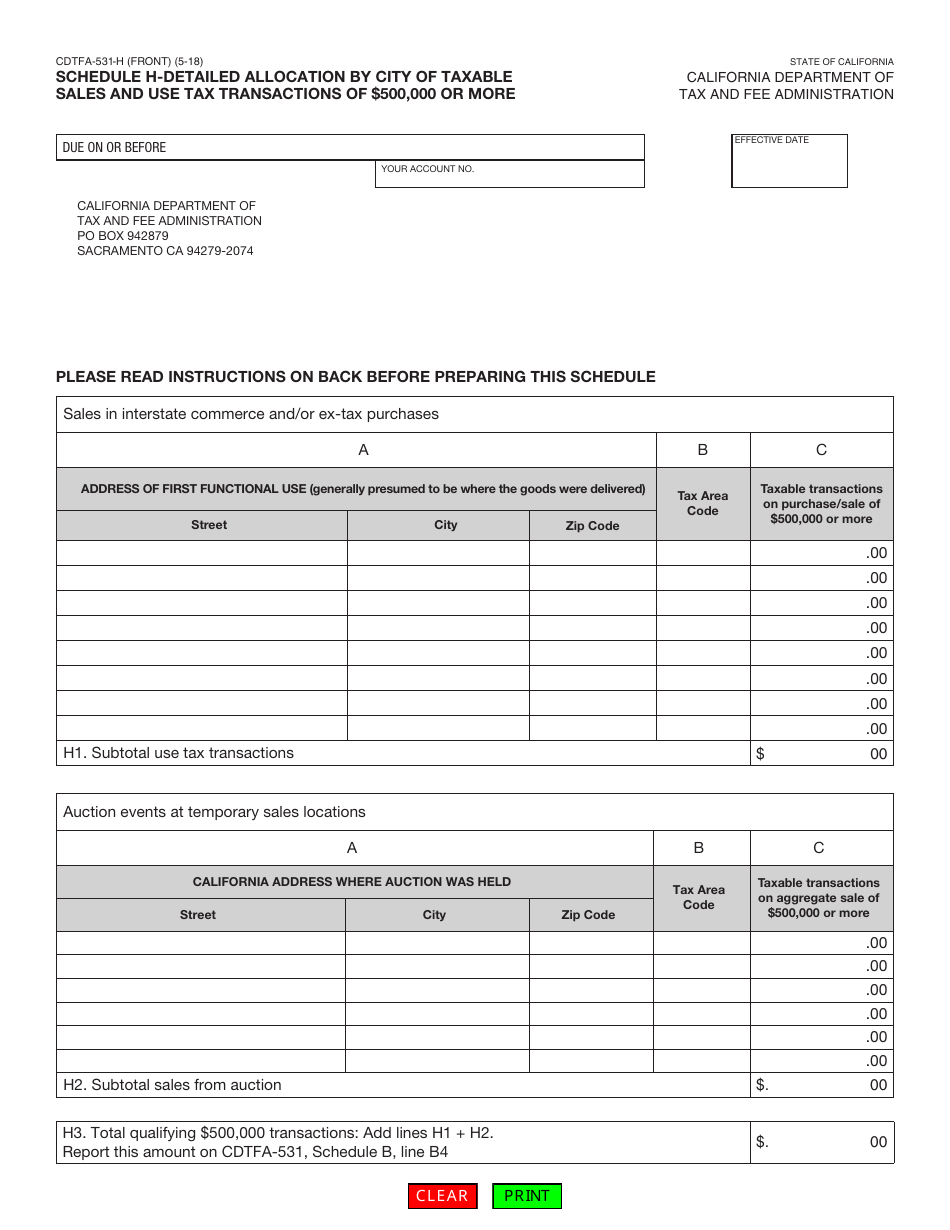

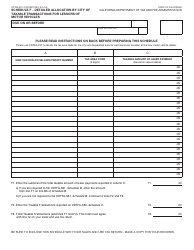

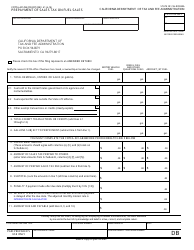

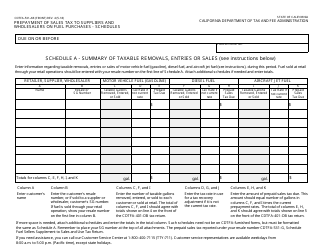

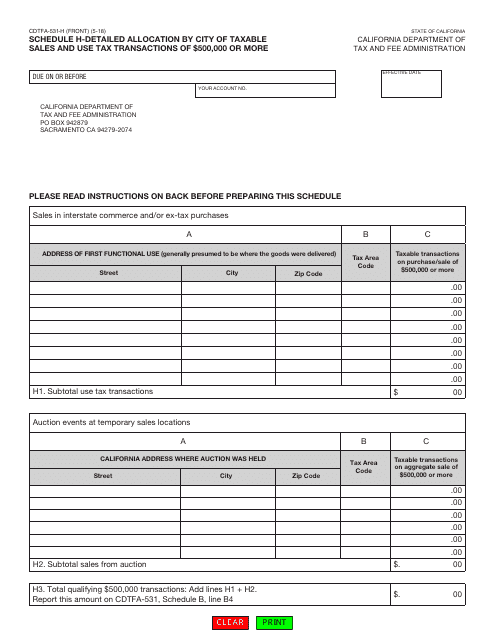

Form CDTFA-531-H Schedule H Detailed Allocation by City of Taxable Sales and Use Tax Transactions of $500,000 or More - California

What Is Form CDTFA-531-H Schedule H?

This is a legal form that was released by the California Department of Tax and Fee Administration - a government authority operating within California. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form CDTFA-531-H?

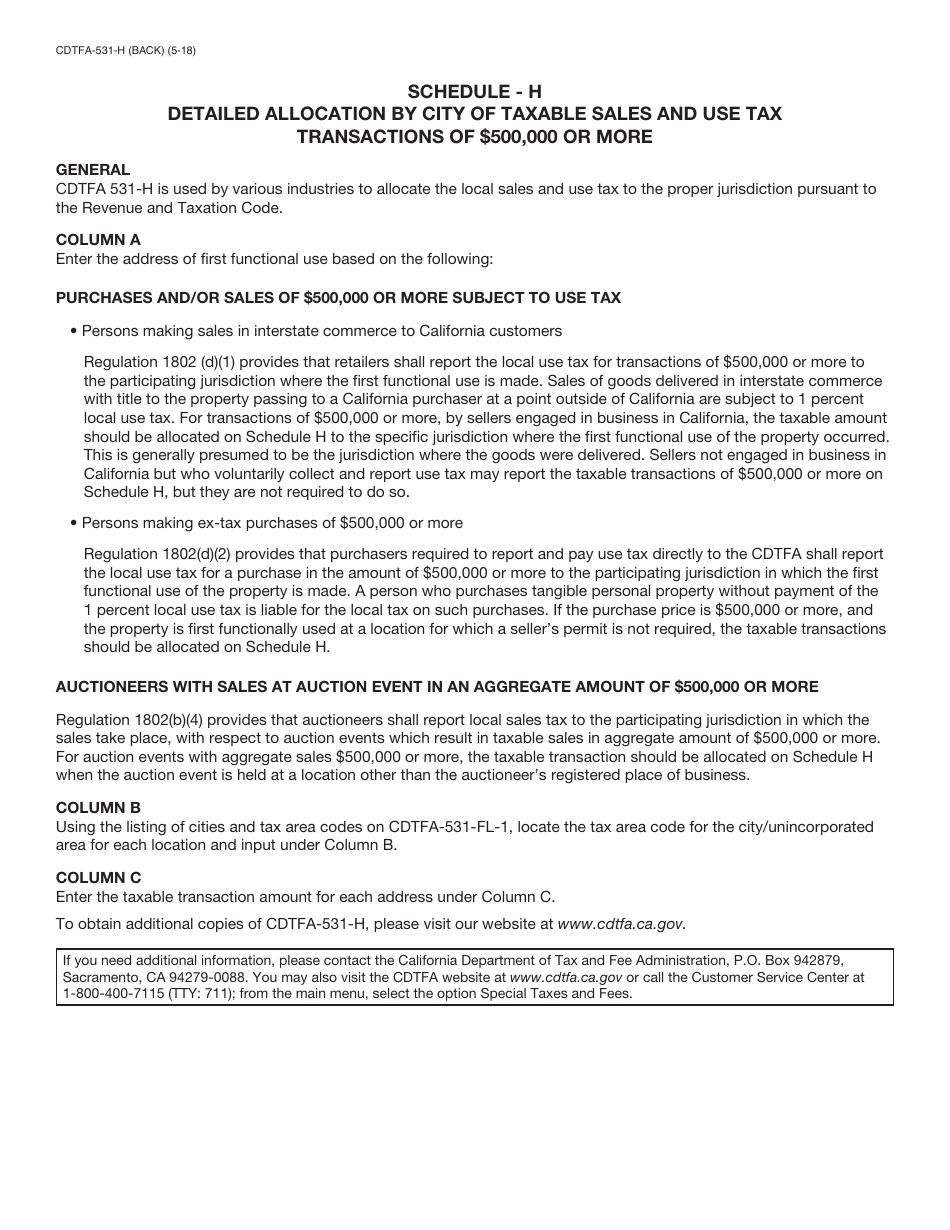

A: Form CDTFA-531-H is a form used to report detailed allocation by city of taxable sales and use tax transactions of $500,000 or more in California.

Q: Who is required to file Form CDTFA-531-H?

A: Any taxpayer who has taxable sales and use tax transactions of $500,000 or more in California is required to file Form CDTFA-531-H.

Q: What is the purpose of Form CDTFA-531-H?

A: The purpose of Form CDTFA-531-H is to provide a detailed breakdown of taxable sales and use tax transactions by city for large transactions.

Q: What information is required on Form CDTFA-531-H?

A: Form CDTFA-531-H requires taxpayers to provide detailed information about their taxable sales and use tax transactions, including the city where the transaction took place.

Q: When is Form CDTFA-531-H due?

A: Form CDTFA-531-H is due on or before the 25th day of the month following the reporting period.

Q: Are there any penalties for late filing of Form CDTFA-531-H?

A: Yes, there may be penalties for late filing of Form CDTFA-531-H. It is important to file the form on time to avoid any penalties or interest charges.

Form Details:

- Released on May 1, 2018;

- The latest edition provided by the California Department of Tax and Fee Administration;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form CDTFA-531-H Schedule H by clicking the link below or browse more documents and templates provided by the California Department of Tax and Fee Administration.

Download Form CDTFA-531-H Schedule H Detailed Allocation by City of Taxable Sales and Use Tax Transactions of $500,000 or More - California

1

2