![]() This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 1099-MISC

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 1099-MISC

for the current year.

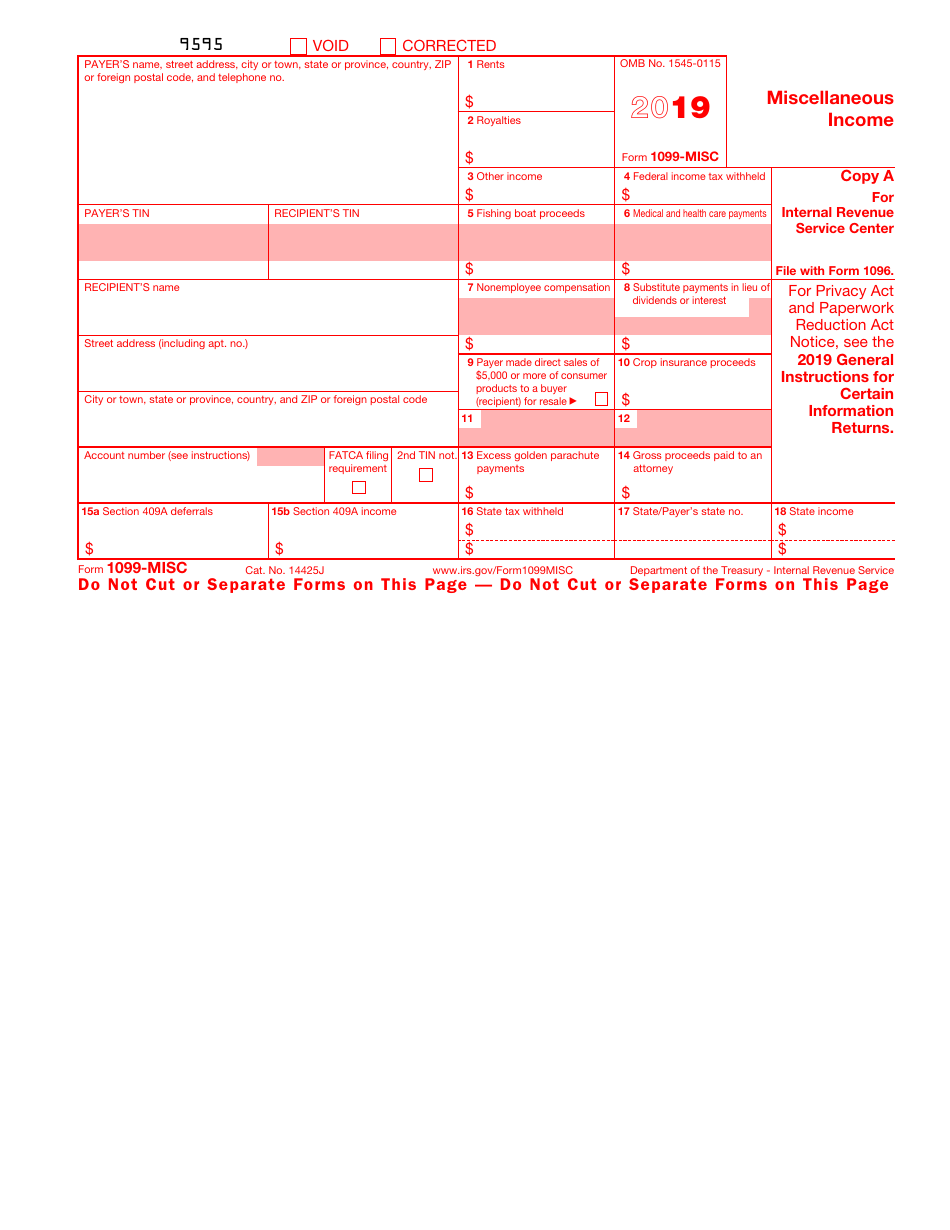

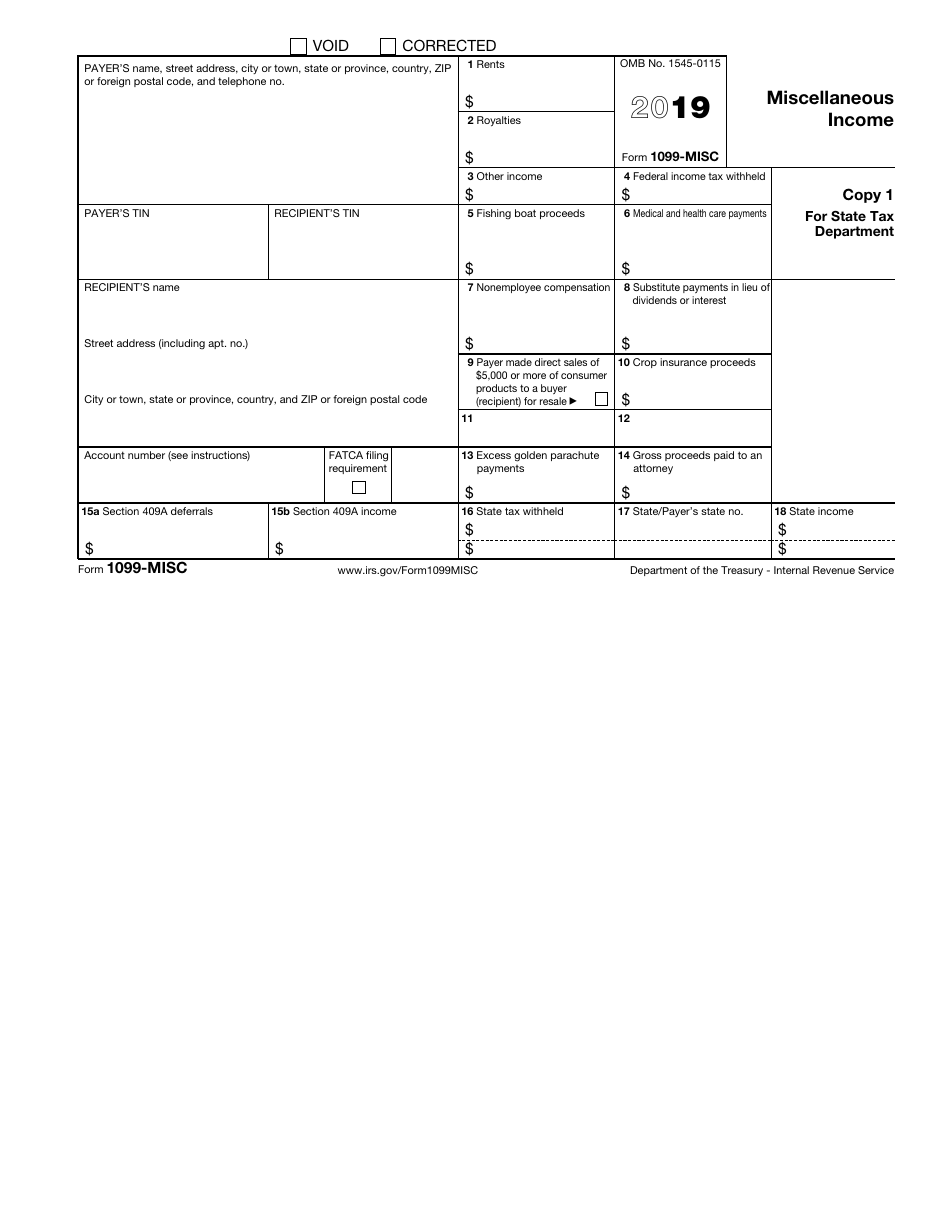

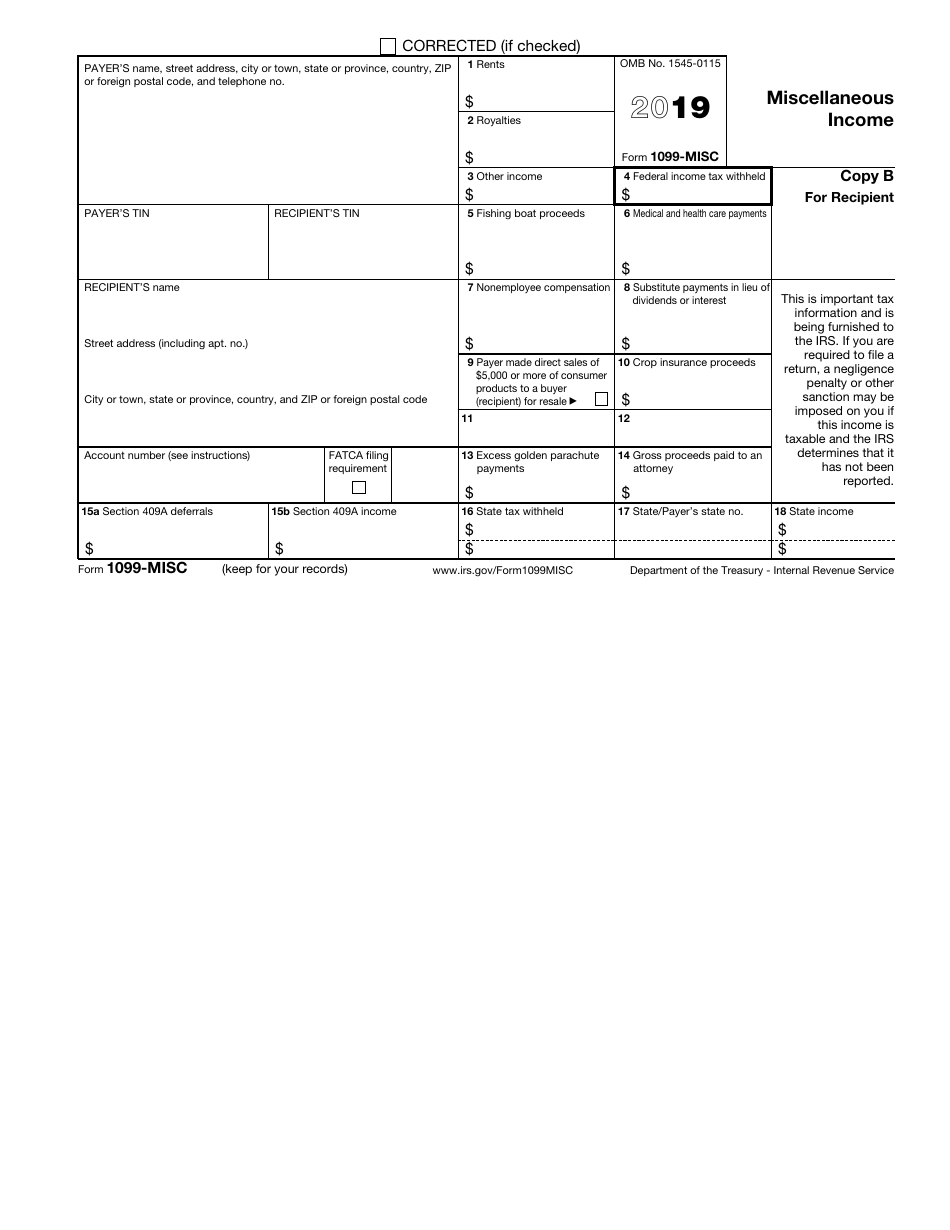

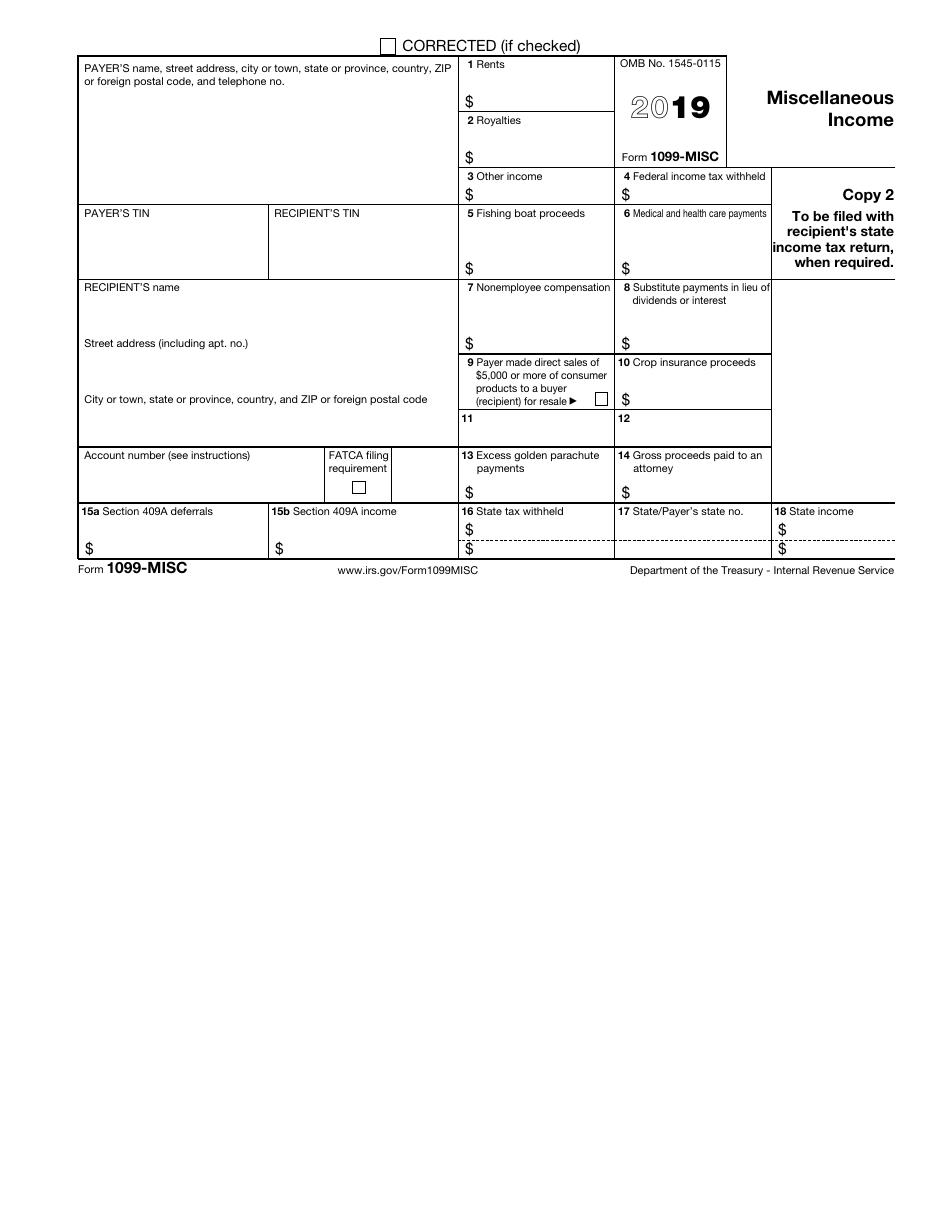

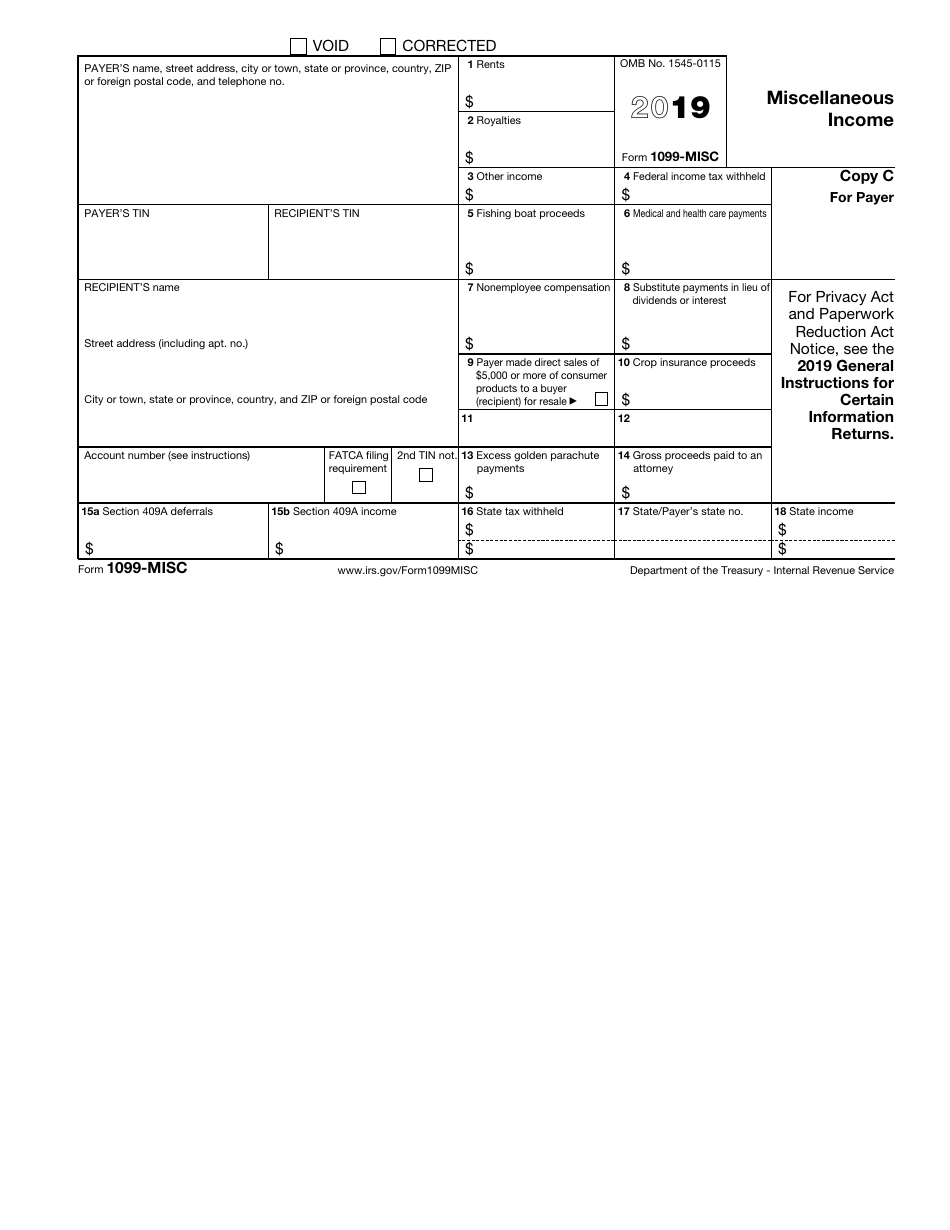

IRS Form 1099-MISC Miscellaneous Income

What Is IRS Form 1099-MISC?

IRS Form 1099-MISC, Miscellaneous Income , is a fiscal document used by organizations that made payments to individuals and companies that were not treated as employees over the course of the tax year.

Alternate Name:

- Tax Form 1099-MISC.

If you manage a business and you had to deal with health care expenses, royalties, or prizes you paid to other parties, you have the responsibility to report these payments as well as the taxes you have deducted.

This statement was issued by the Internal Revenue Service (IRS) in 2019 - previous editions of the instrument are now obsolete. An IRS Form 1099-MISC fillable version is available for download below.

Check out the 1099 Series of form to see more IRS documents in this series.

What Is a 1099-MISC Form Used For?

Complete and submit Form 1099-MISC to inform tax organzations about different types of compensation you have paid over the calendar year whether you paid rent to the owner of your office or storage facility or had legal expenses paid to an attorney. These payments are not reported on other returns which is why it is necessary to keep track of all the payments over twelve months and confirm they meet the reporting thresholds. Additionally, this document must be sent to the individual or entity that received the payment to remind them about the extra income they have earned during the year.

Make sure you send two copies of the form to the recipient of your payments by January 31 - they will need time to prepare their own tax documentation. Form 1099-MISC deadline for filing with fiscal authorities is February 28 if you opt for a paper return - those who submit the information electronically will have extra time to handle the paperwork and will have to file the form by April 1.

When to Use 1099-MISC?

At the end of the year, if you are an independent contractor or self-employed individual, you should receive this form from each client who hired and paid you at least $600 throughout the calendar year, and you may attach the form to your tax return. The IRS requires that you report all of your income and pay income tax on it, and you must do so even if you did not receive a 1099-MISC form or earn $600.

How to Use 1099-MISC Form?

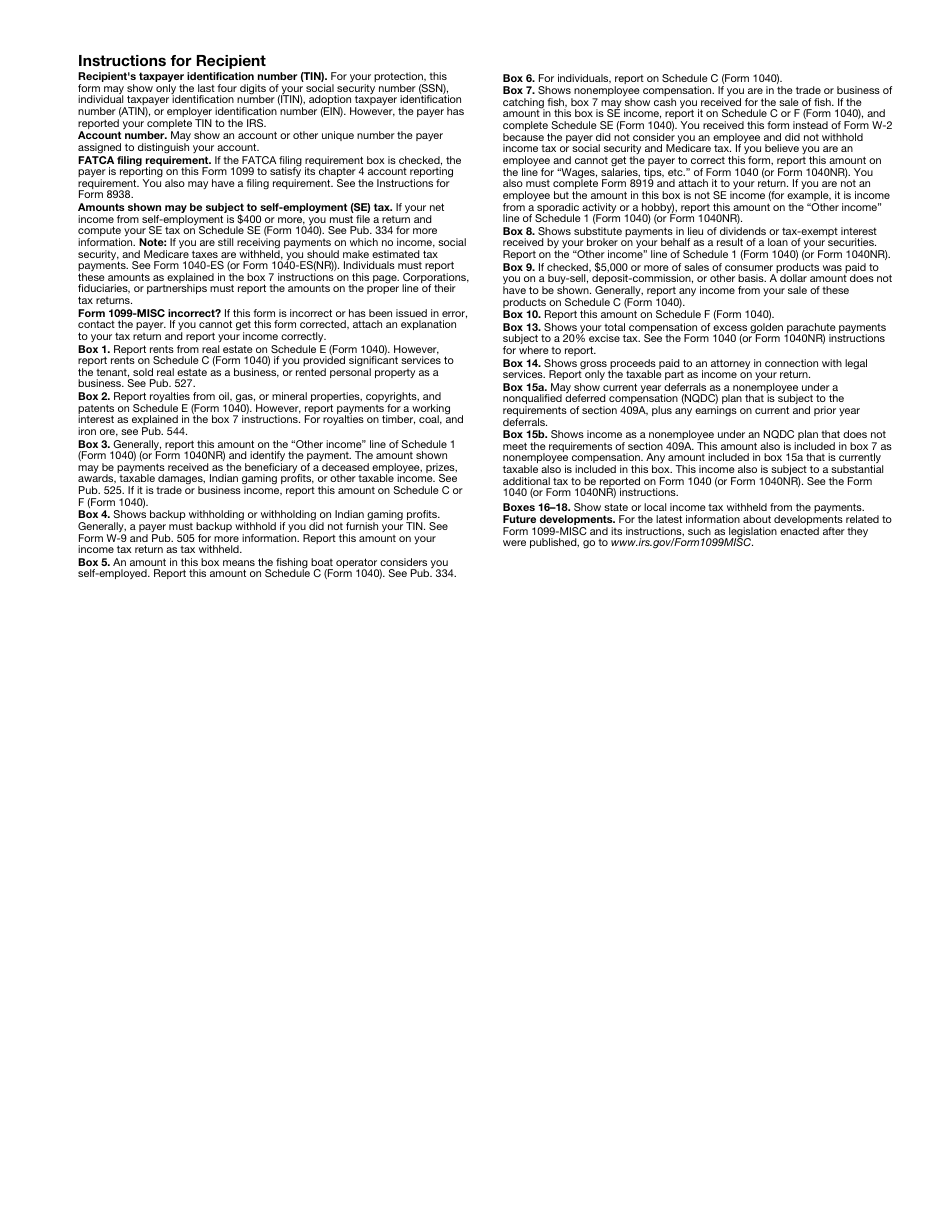

The IRS provides separate Instructions for Form 1099-MISC. The IRS Form 1099-MISC instructions are as follows:

The four black parts of the form must be completed and printed when reporting miscellaneous income:

- Copy 1 is sent to the recipient's state tax department;

- Copy B must be retained by the recipient;

- Copy 2 must be attached to the recipient's state tax return; and

- Copy C is kept by the payer.

The form 1099-MISC fillable version is available on the IRS website.

When Is Form 1099-MISC Due?

The IRS Form 1099-MISC due date is January 31, 2020, if you are reporting nonemployee compensation (NEC) payments in box 7, whether the filing is done on paper or electronically. For all other reported payments, Form 1099-MISC must be filed by February 28, 2020, if filed on paper, or by March 31, 2020, if filed electronically.

The due date for furnishing statements to recipients (if amounts are reported in box 8 or 14) is February 18, 2020.

IRS 1099-MISC Related Forms:

Apart from the IRS 1099-MISC Form, the IRS Form 1099 series comprises of the following 19 variants:

- 1099-A, Acquisition or Abandonment of Secured Property. Use this form to provide information on the acquisition or abandonment of the property serving as security for the debt where you are the lender. There are no limits as regards to the amount.

- 1099-B, Proceeds from Broker and Barter Exchange Transactions. This form is used to report sales or redemptions of securities, commodities, futures transactions, and barter exchange transactions in all amounts.

- 1099-C, Cancellation of Debt. This form is filed by the lender and is used to report a $600 minimum in the cancellation of a debt owed to a financial institution, the federal government, a credit union, a military department, the U.S. Postal Service, or any organization having a significant money-lending trade or business. The IRS treats the debt cancellation as income, which may be taxable to the debtor.

- 1099-CAP, Changes in Corporate Control and Capital Structure. This form is filed by the corporation and is used to report information about cash, stock, or any other property obtained through the acquisition of control, or to declare a substantial change in the capital structure of a corporation. Only amounts over $1,000 are to be reported.

- 1099-DIV, Dividends and Distributions. An investment fund company uses this form to report their distributions and dividends that were paid on stock and liquidation distributions during the year. These payments are different than the income earned by the company from selling stocks; it is a payment of the corporation's earnings directly to shareholders. The minimum amount to be reported is $10, and $600 for liquidations.

- 1099-G, Certain Government Payments. This form is filed by a government agency and is used to report at least $10 in compensations for unemployment, state and local income tax refunds, taxable grants, and agricultural payments made during the year.

- 1099-H, Health Coverage Tax Credit (HCTC) Advance Payments. This form is used to report health insurance premiums that were paid on behalf of certain individuals.

- 1099-INT, Interest Income. This form is used to report interest payments. Taxpayers receive this form from the government, financial institutions, or banks where they have interest-bearing accounts. In some cases, the minimum amount to be reported is $10, and others $600.

- 1099-K, Payment Card and Third Party Network Transactions. Banks and other payment processors use this form to report payment card transactions in any amount, and third party network transactions of at least $20,000 and a minimum of 200 transactions.

- 1099-LS, Reportable Life Insurance Sale. This form is used to report amounts paid in a reportable policy sale in any amount.

- 1099-LTC, Long-Term Care and Accelerated Death Benefits. This form is used to report payments made in compliance with a long-term care insurance contract and accelerated death benefits paid in compliance of a life insurance contract or by a viatical settlement provider, in any amount.

- 1099-OID, Original Issue Discount. The issuer of the debt instrument or broker uses this form to report a minimum $10 original issue discount (the issuer of the debt instrument or broker uses this form to report a minimum $10 original issue discount, which is a form of interest).

- 1099-PATR, Taxable Distributions Received From Cooperatives. This form is used to report at least $10 in distributions from cooperatives.

- 1099-Q, Payments from Qualified Education Programs. This form is used to report earnings from qualified tuition programs and Coverdell Education Savings Accounts.

- 1099-QA, Distributions from ABLE Accounts. This form is used to report the distributions from Achieving a Better Life Experience (ABLE) accounts, in any amount.

- 1099-R, Distributions from Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc. This form is used to report the distributions obtained from retirement or profit-sharing plans, any Individual Retirement Arrangement (IRA), insurance contract, and IRA recharacterization, in at least $10 amount.

- 1099-S, Proceeds from Real Estate Transactions. This form is used to report at least $600 in gross proceeds from sales or exchanges of real estate and certain royalty payments.

- 1099-SA, Distributions from an HSA, Archer MSA, or Medicare Advantage MSA. This form is used to report any amount of distributions from a Health Savings Account or an Archer or Medicare Advantage Medical Savings Account.

- 1099-SB, Seller's Investment in Life Insurance Contract. The issuer of a life insurance contract uses this to report the seller's investment in the contract, in any amount.

Download IRS Form 1099-MISC Miscellaneous Income

1

2

3

4

5

6

7

8