![]() This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 2210

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 2210

for the current year.

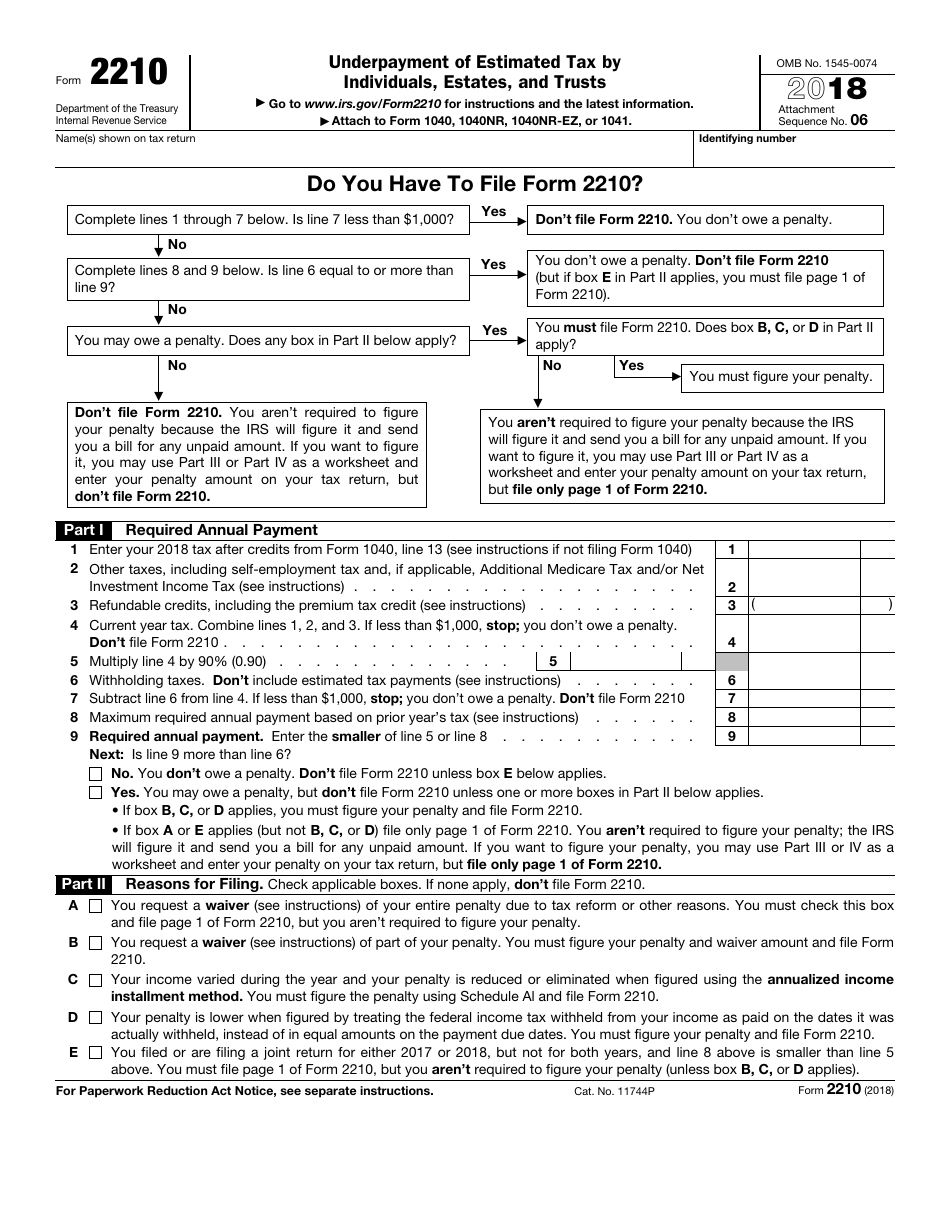

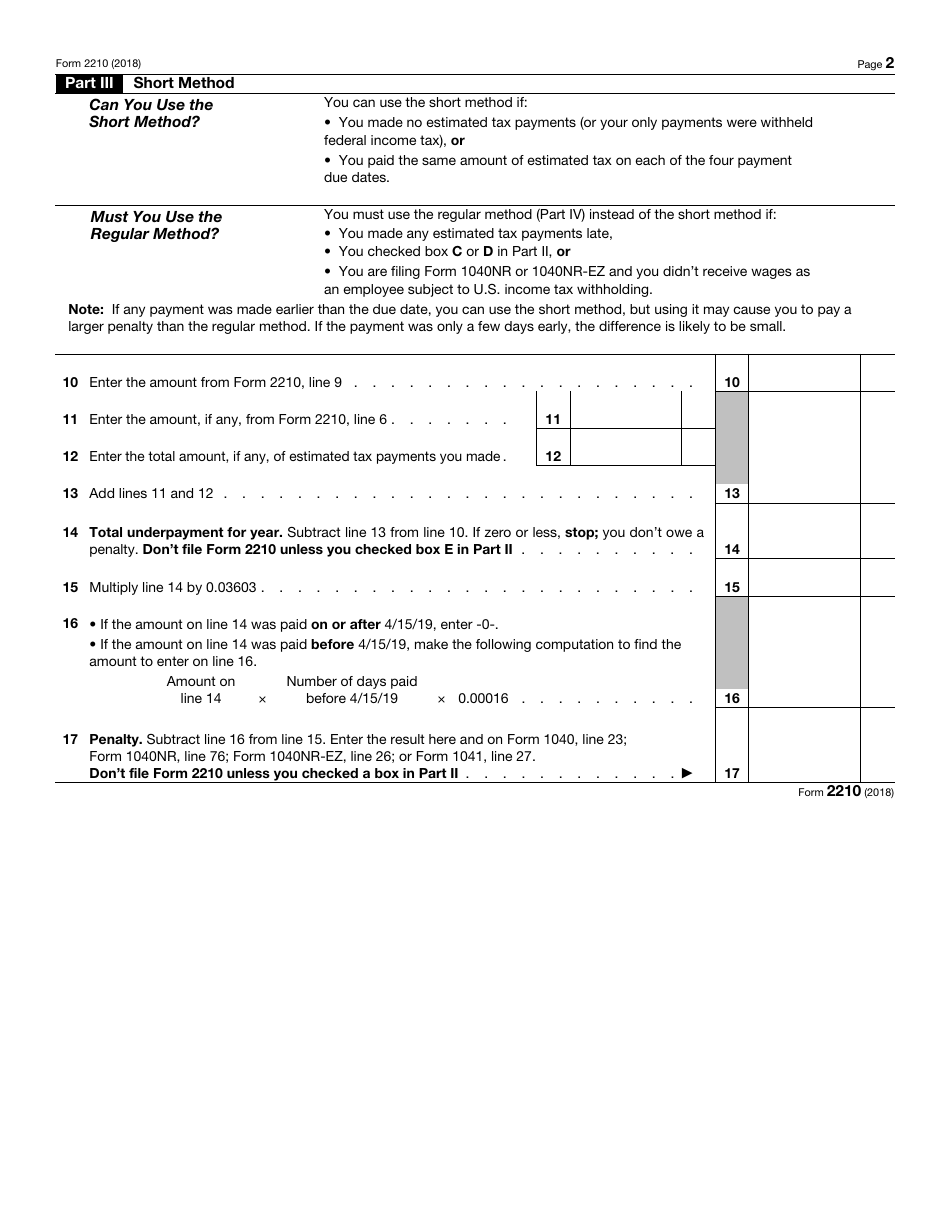

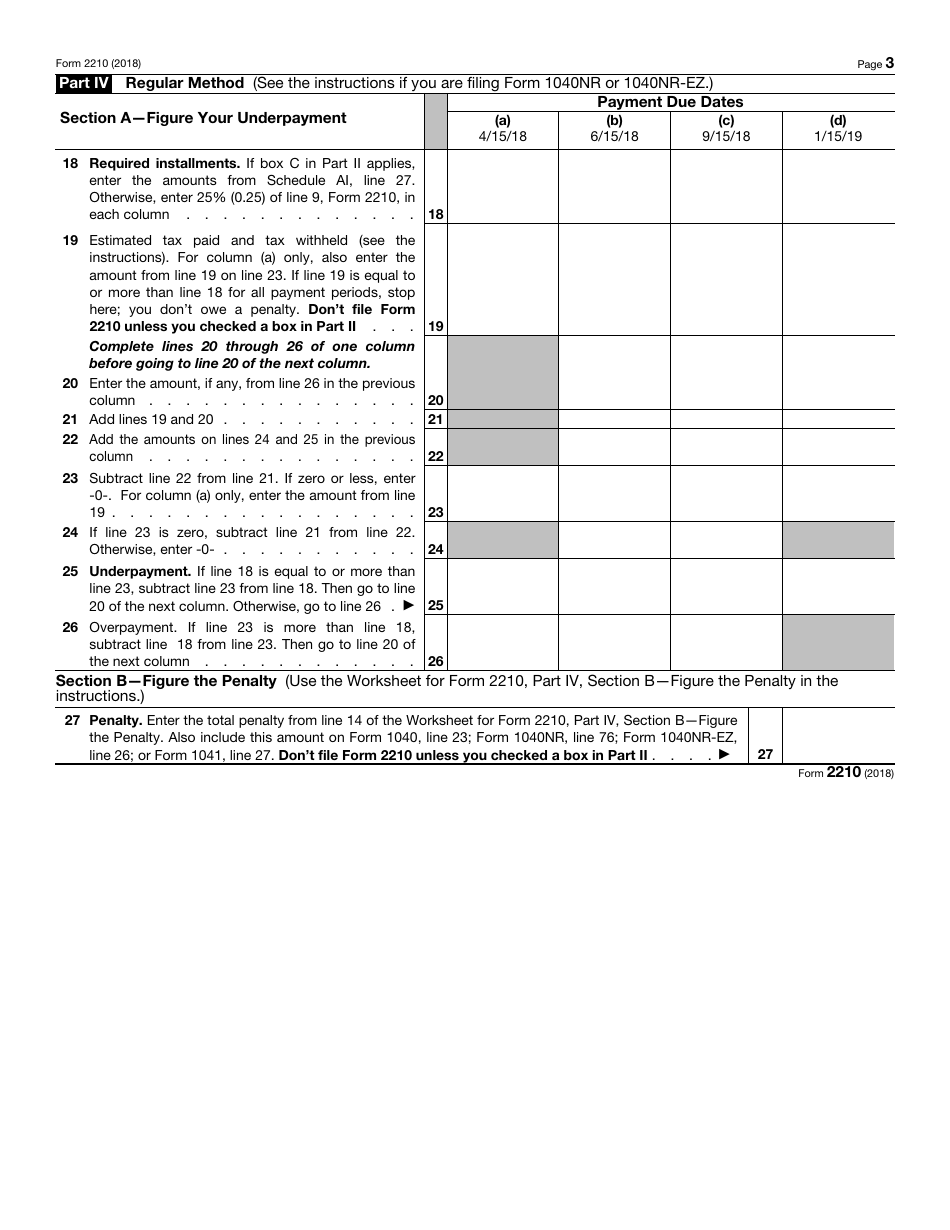

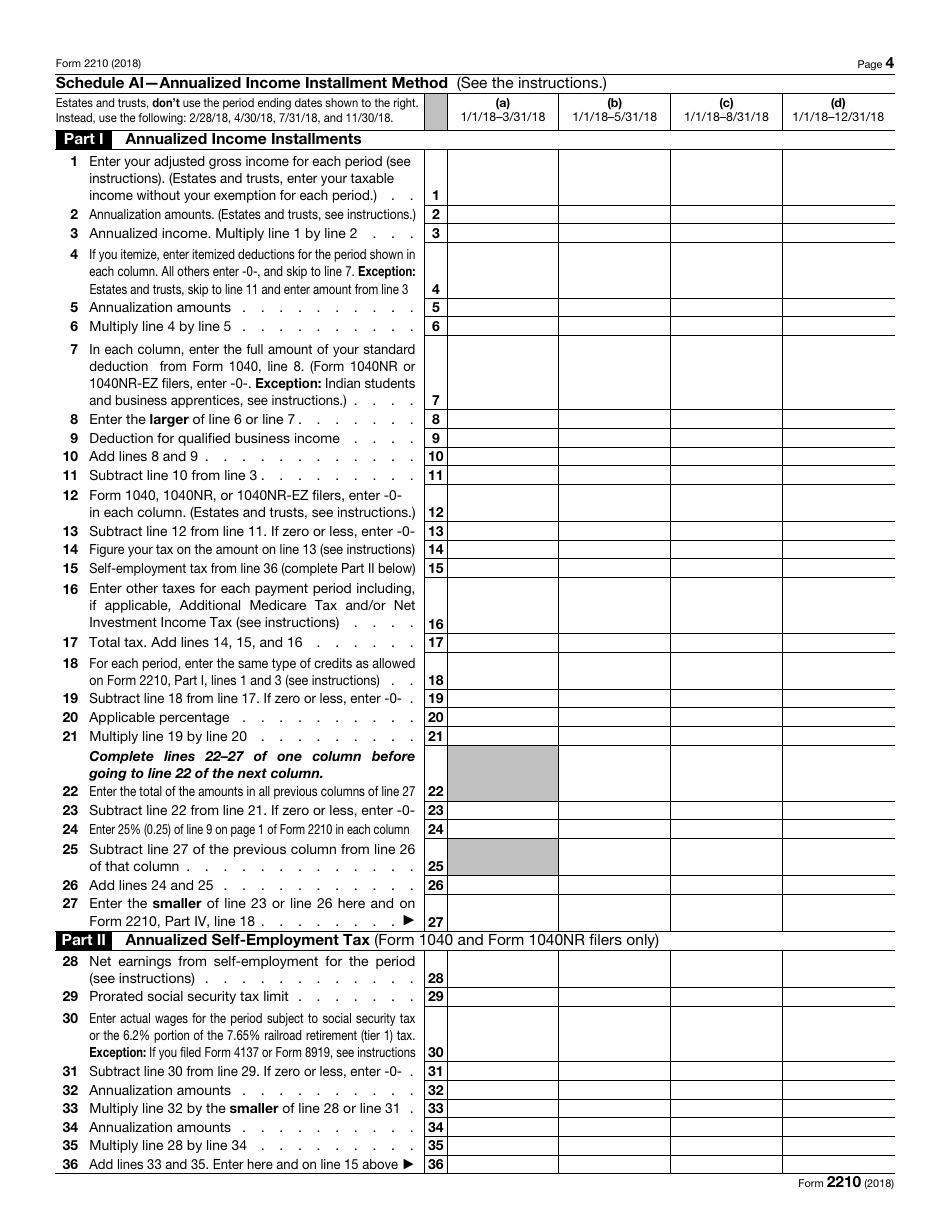

IRS Form 2210 Underpayment of Estimated Tax by Individuals, Estates, and Trusts

What Is IRS Form 2210?

This is a tax form that was released by the Internal Revenue Service (IRS) - a subdivision of the U.S. Department of the Treasury. Check the official IRS-issued instructions before completing and submitting the form.

FAQ

Q: What is IRS Form 2210?

A: IRS Form 2210 is used to calculate any underpayment of estimated tax by individuals, estates, and trusts.

Q: Who needs to fill out IRS Form 2210?

A: Individuals, estates, and trusts who have underpaid their estimated tax for the year may need to fill out IRS Form 2210.

Q: Why would someone need to fill out IRS Form 2210?

A: If someone didn't pay enough tax throughout the year, they may be subject to penalties. IRS Form 2210 helps calculate any potential underpayment penalties.

Q: How do I fill out IRS Form 2210?

A: To fill out IRS Form 2210, you need to follow the instructions provided on the form and accurately calculate any potential underpayment penalties.

Form Details:

- A 4-page form available for download in PDF;

- This form cannot be used to file taxes for the current year. Choose a more recent version to file for the current tax year;

- Editable, printable, and free;

- Fill out the form in our online filing application.

Download a fillable version of IRS Form 2210 through the link below or browse more documents in our library of IRS Forms.

Download IRS Form 2210 Underpayment of Estimated Tax by Individuals, Estates, and Trusts

1

2

3

4