![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 1040 Schedule D

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 1040 Schedule D

for the current year.

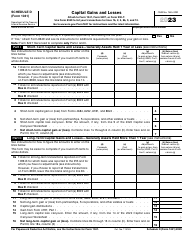

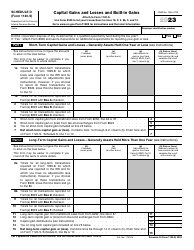

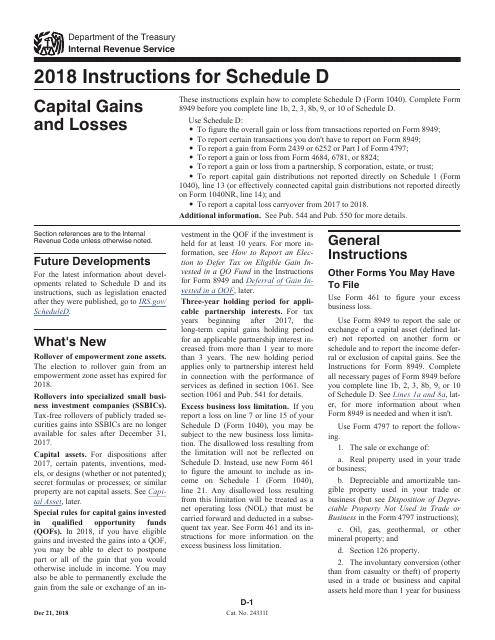

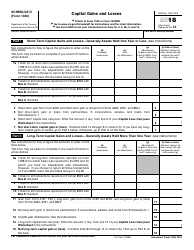

Instructions for IRS Form 1040 Schedule D Capital Gains and Losses

This document contains official instructions for IRS Form 1040 Schedule D, Capital Gains and Losses - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 1040 Schedule D is available for download through this link.

FAQ

Q: What is IRS Form 1040 Schedule D?

A: IRS Form 1040 Schedule D is a tax form used to report capital gains and losses.

Q: What are capital gains and losses?

A: Capital gains are the profits made from the sale of assets like stocks, real estate, or mutual funds. Capital losses occur when you sell these assets for less than their original purchase price.

Q: When do I need to file Schedule D?

A: You need to file Schedule D if you have any capital gains or losses during the tax year.

Q: How do I fill out Schedule D?

A: You will need to provide information about your capital asset sales and calculate your capital gains or losses. The form includes sections for short-term and long-term transactions.

Q: What are short-term and long-term capital gains?

A: Short-term capital gains are profits from the sale of assets held for one year or less. Long-term capital gains are profits from the sale of assets held for more than one year.

Q: Are there any exceptions or special rules for reporting capital gains and losses?

A: Yes, there are some exceptions and special rules, such as the wash sale rule and the 0% capital gains tax rate for certain low-income taxpayers. Consult the IRS instructions for more details.

Q: Are there any penalties for not filing Schedule D or reporting capital gains and losses?

A: Yes, failing to file Schedule D or accurately reporting capital gains and losses can result in penalties and interest charges. It's important to accurately report your gains and losses.

Q: Can I e-file Schedule D?

A: Yes, you can e-file Schedule D using tax software or through a professional tax preparer.

Q: Do I need to include supporting documents with Schedule D?

A: You generally do not need to include supporting documents when filing Schedule D. However, you should keep all necessary records and documents in case of an IRS audit.

Instruction Details:

- This 17-page document is available for download in PDF;

- Not applicable for the current tax year. Choose a more recent version to file this year's taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17