![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 8804-W

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for IRS Form 8804-W

for the current year.

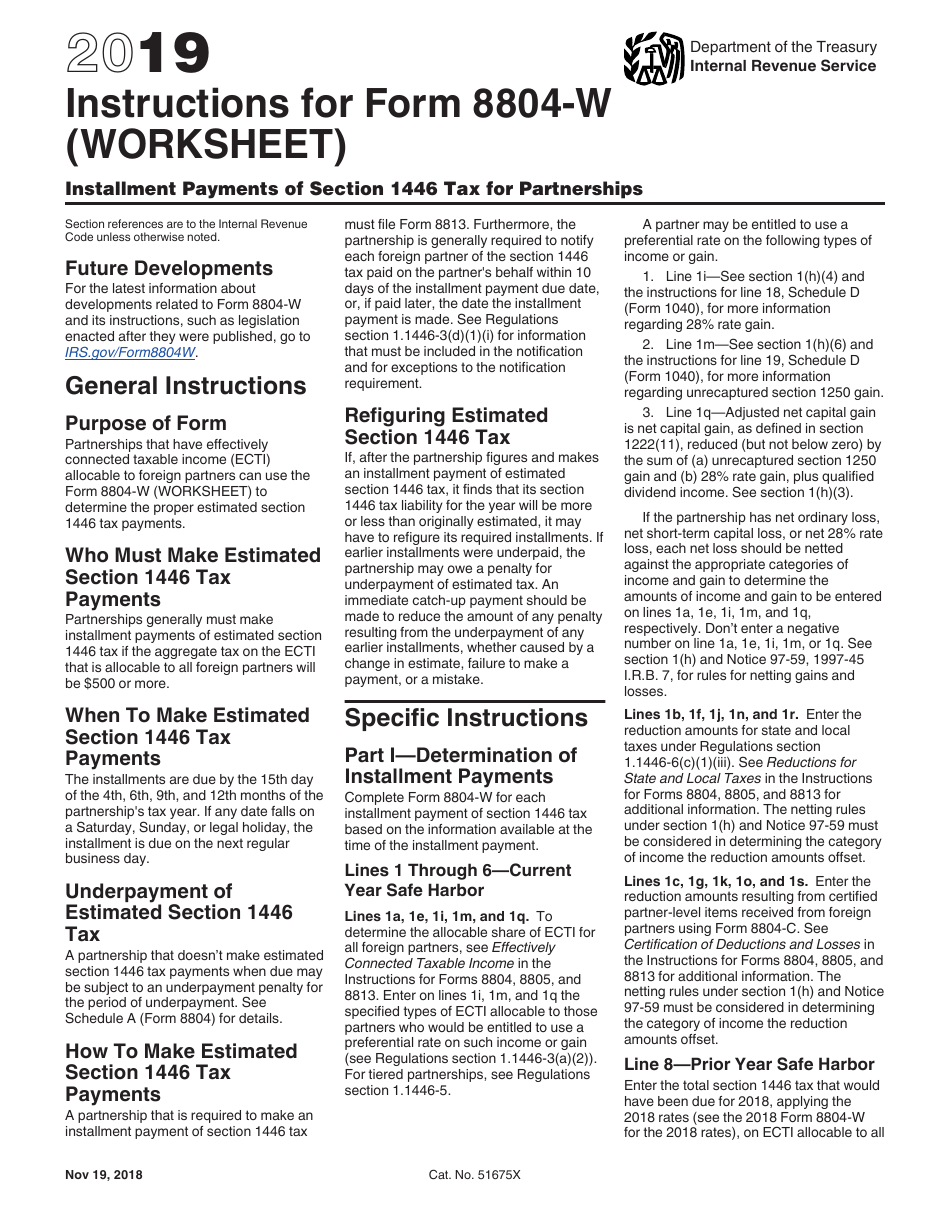

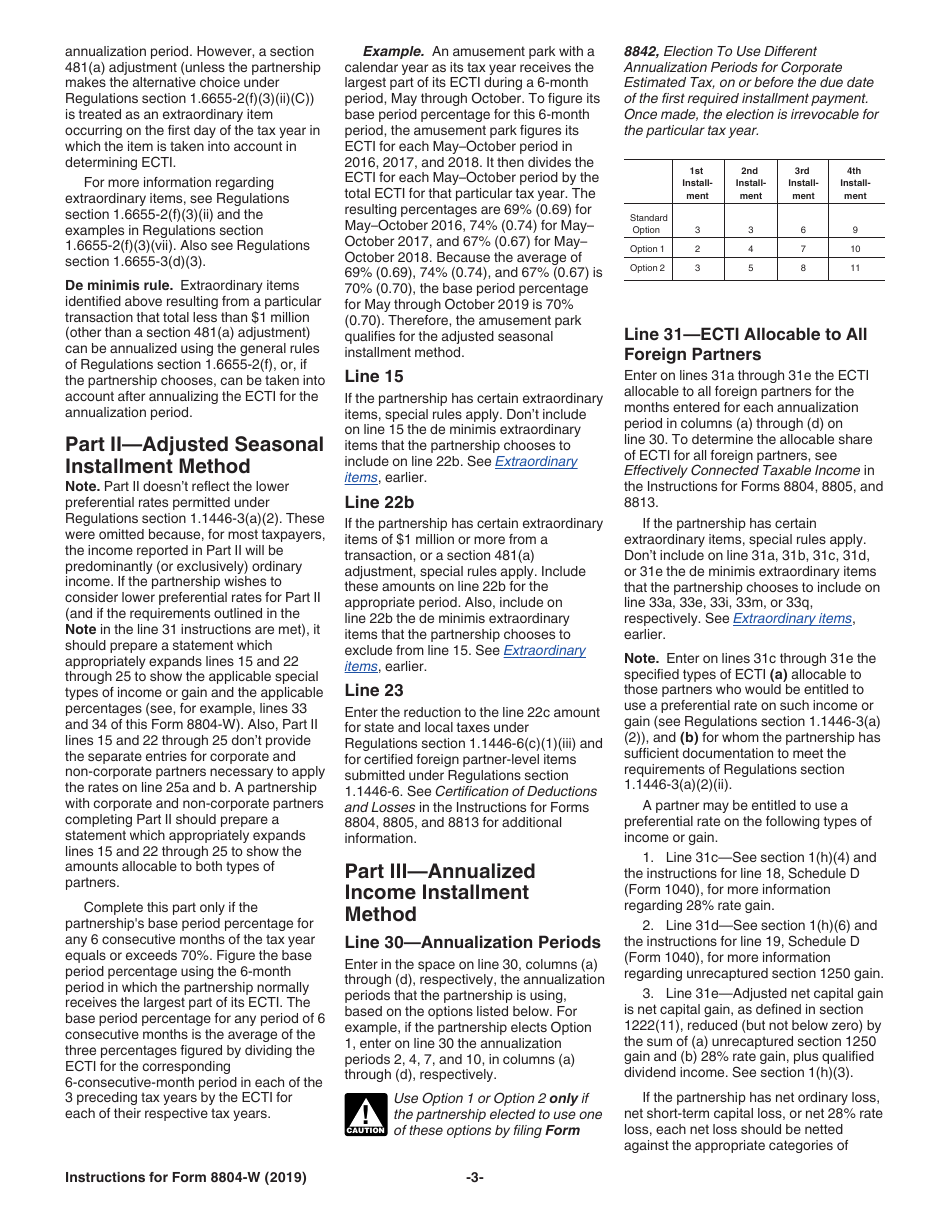

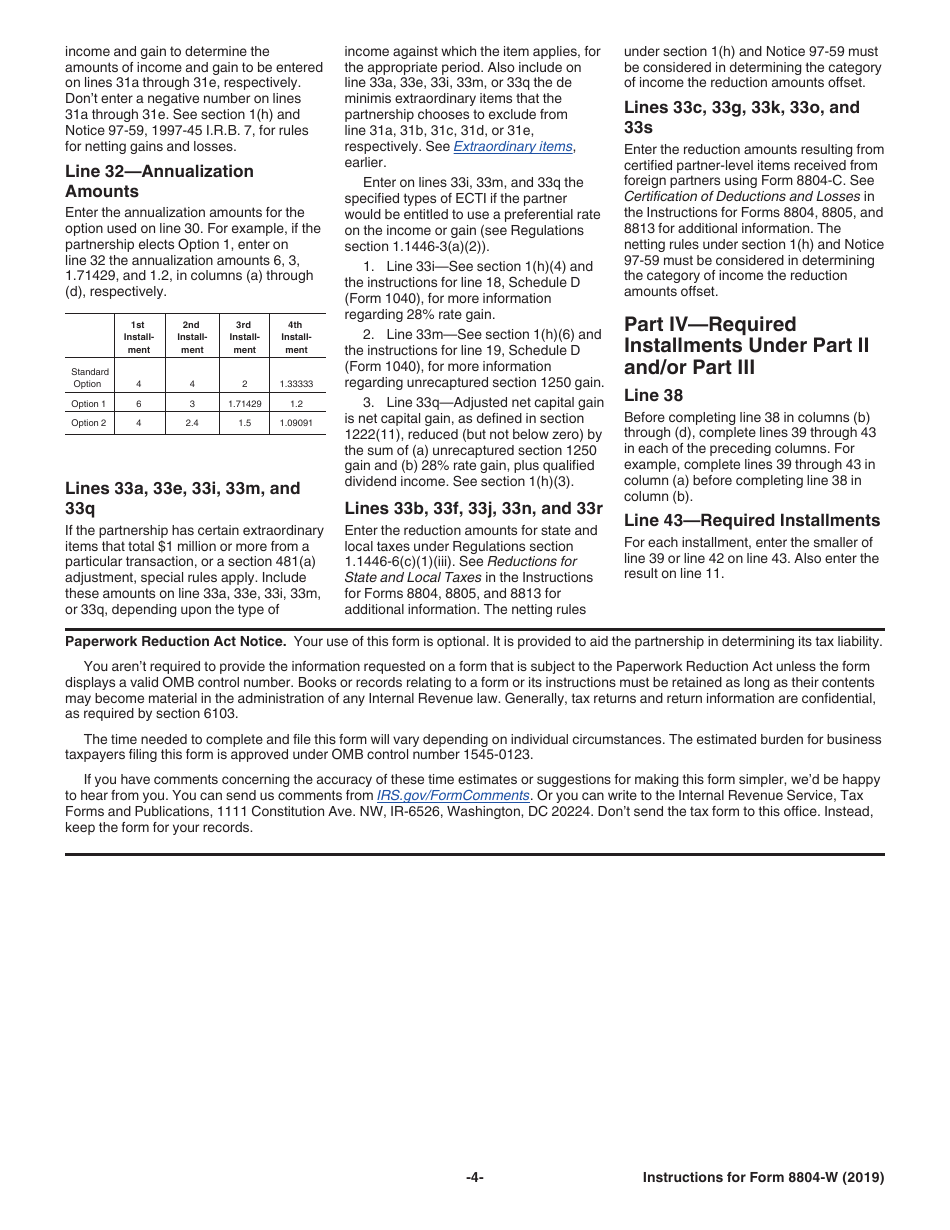

Instructions for IRS Form 8804-W Installment Payments of Section 1446 Tax for Partnerships

This document contains official instructions for IRS Form 8804-W , Installment Payments of Section 1446 Tax for Partnerships - a tax form released and collected by the Internal Revenue Service (IRS), a subdivision of the U.S. Department of the Treasury. An up-to-date fillable IRS Form 8804-W is available for download through this link.

FAQ

Q: What is IRS Form 8804-W?

A: IRS Form 8804-W is a form used by partnerships to make installment payments of Section 1446 tax.

Q: What is Section 1446 tax?

A: Section 1446 tax is a withholding tax requirement for foreign partners in a partnership.

Q: Who needs to file IRS Form 8804-W?

A: Partnerships that have foreign partners and are subject to Section 1446 tax withholding requirements need to file Form 8804-W.

Q: What are installment payments?

A: Installment payments are partial payments made over a period of time rather than paying the full tax amount upfront.

Q: How often do I need to make installment payments?

A: Installment payments for Section 1446 tax are typically made on a quarterly basis.

Q: What information is required on Form 8804-W?

A: Form 8804-W requires information about the partnership, the amount of tax to be withheld, and the installment payment schedule.

Q: Are there any penalties for not filing Form 8804-W?

A: Yes, there can be penalties for failure to file or pay the Section 1446 tax.

Q: Can I file Form 8804-W electronically?

A: Yes, you can file Form 8804-W electronically using the IRS's e-file system.

Q: Can I make changes to my installment payment schedule?

A: Yes, you can make changes to your installment payment schedule by filing an amended Form 8804-W.

Instruction Details:

- This 4-page document is available for download in PDF;

- Not applicable for the current tax year. Choose a more recent version to file this year's taxes;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of IRS-released tax documents.

Download Instructions for IRS Form 8804-W Installment Payments of Section 1446 Tax for Partnerships

1

2

3

4