![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form DR-7

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form DR-7

for the current year.

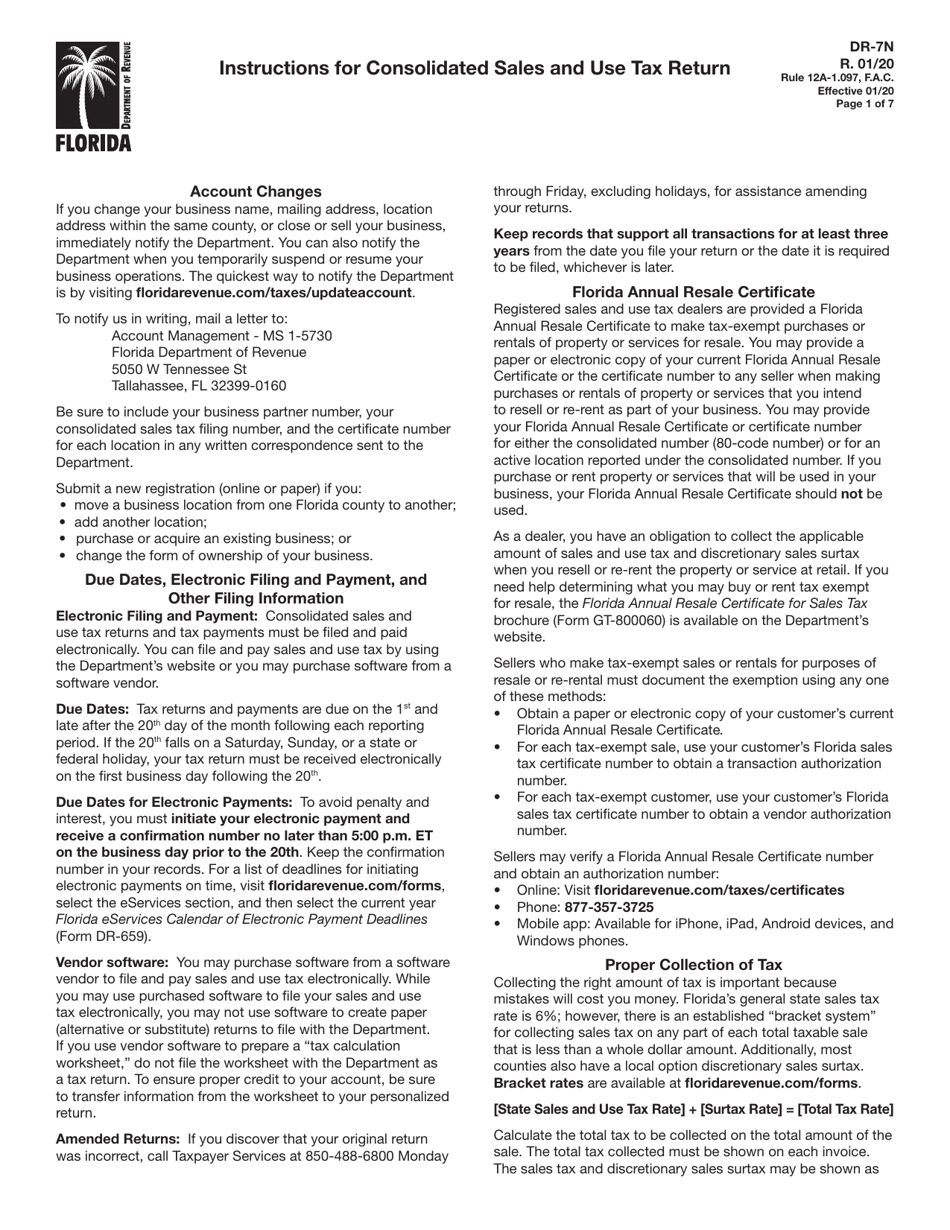

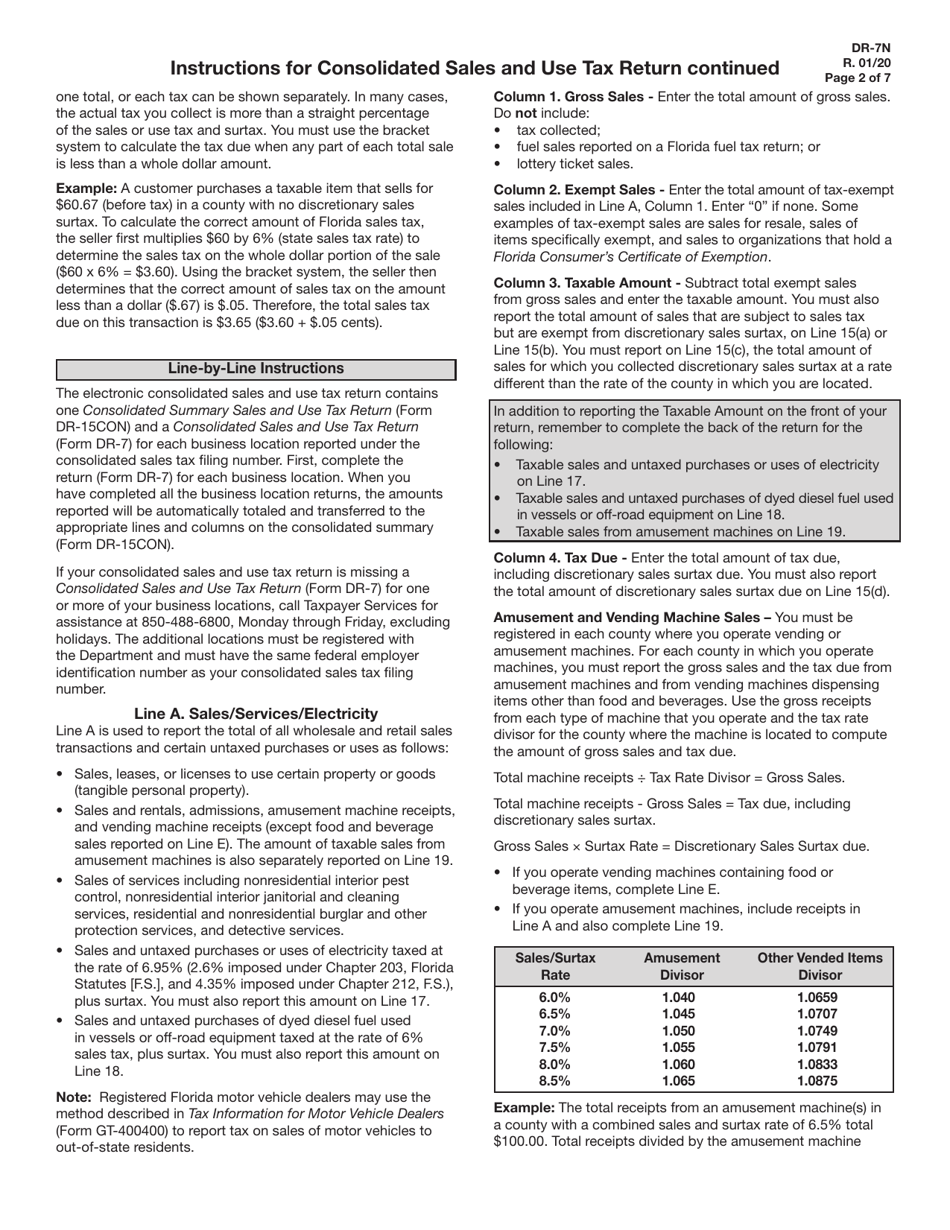

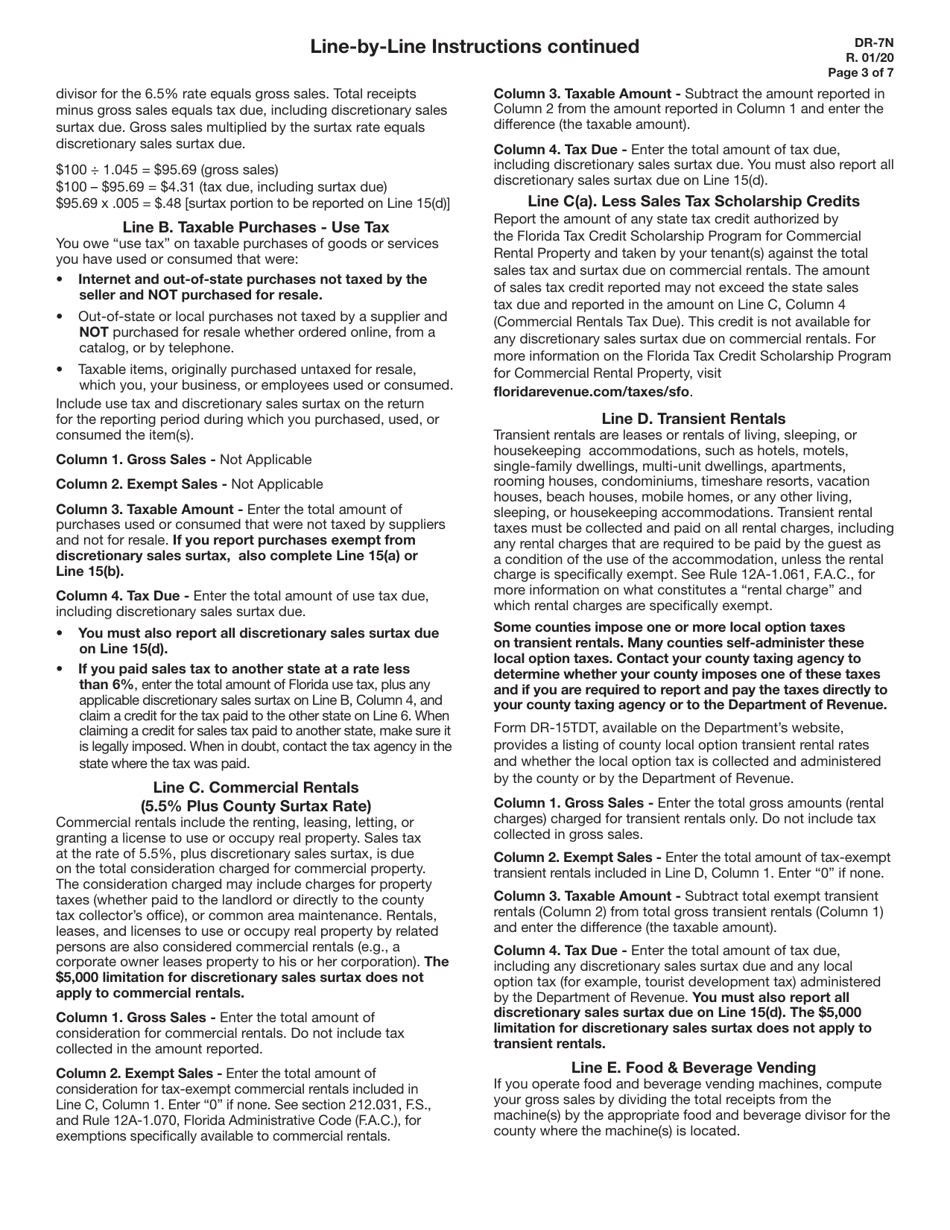

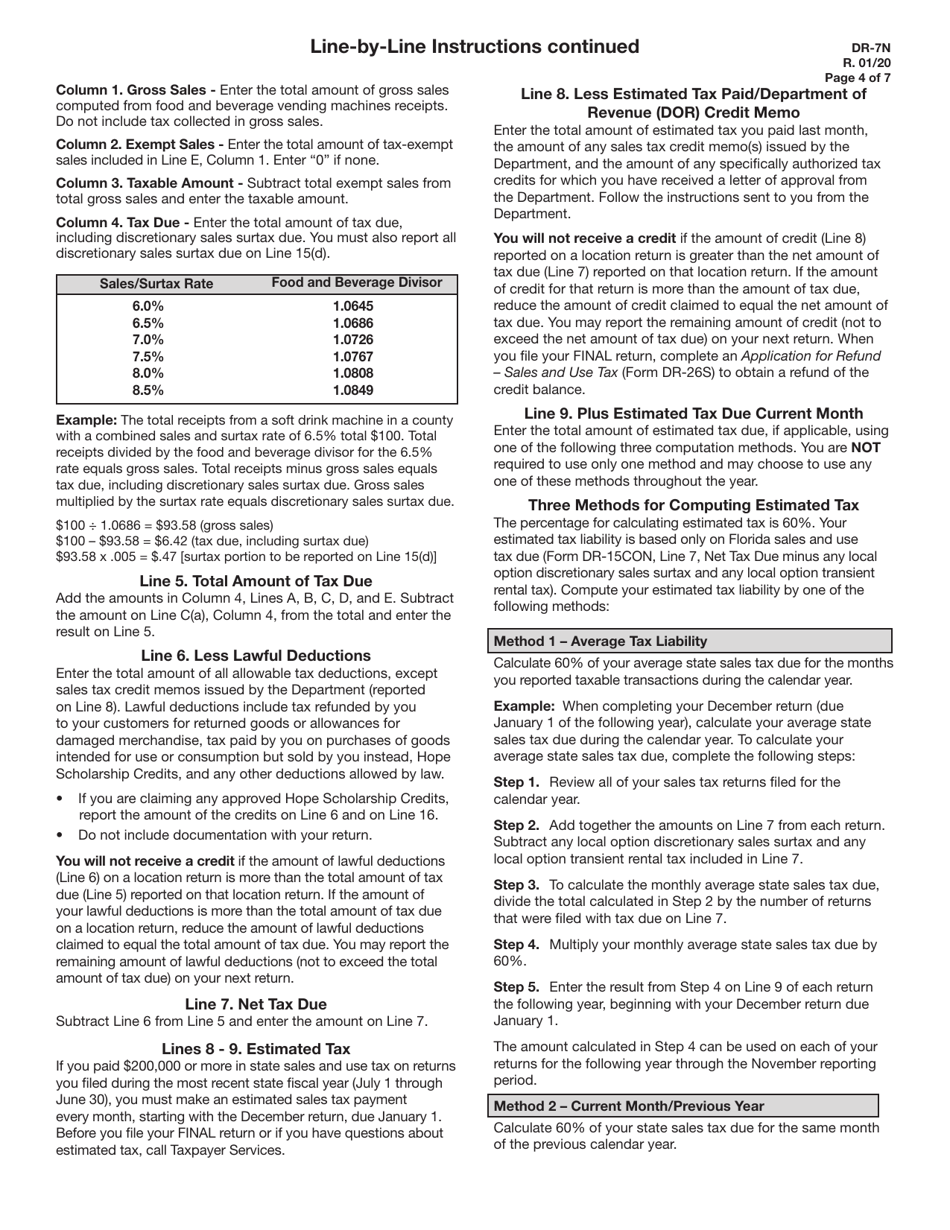

Instructions for Form DR-7 Consolidated Sales and Use Tax Return - Florida

This document contains official instructions for Form DR-7 , Consolidated Sales and Use Tax Return - a form released and collected by the Florida Department of Revenue.

FAQ

Q: What is Form DR-7?

A: Form DR-7 is the Consolidated Sales and Use Tax Return in Florida.

Q: What is the purpose of Form DR-7?

A: Form DR-7 is used to report and remit sales and use tax collected by a business in Florida.

Q: Who needs to file Form DR-7?

A: Businesses registered to collect sales and use tax in Florida must file Form DR-7.

Q: When is Form DR-7 due?

A: Form DR-7 is due on or before the 20th day of the month following the end of the reporting period.

Q: What information do I need to complete Form DR-7?

A: You will need to provide details about your business, as well as the sales and use tax collected during the reporting period.

Q: Are there any penalties for late filing of Form DR-7?

A: Yes, there are penalties for late filing of Form DR-7, including a late filing fee and interest on any unpaid tax.

Q: Can I request an extension to file Form DR-7?

A: Yes, you can request an extension by contacting the Florida Department of Revenue.

Instruction Details:

- This 7-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Florida Department of Revenue.

1

2

3

4

5

6

7