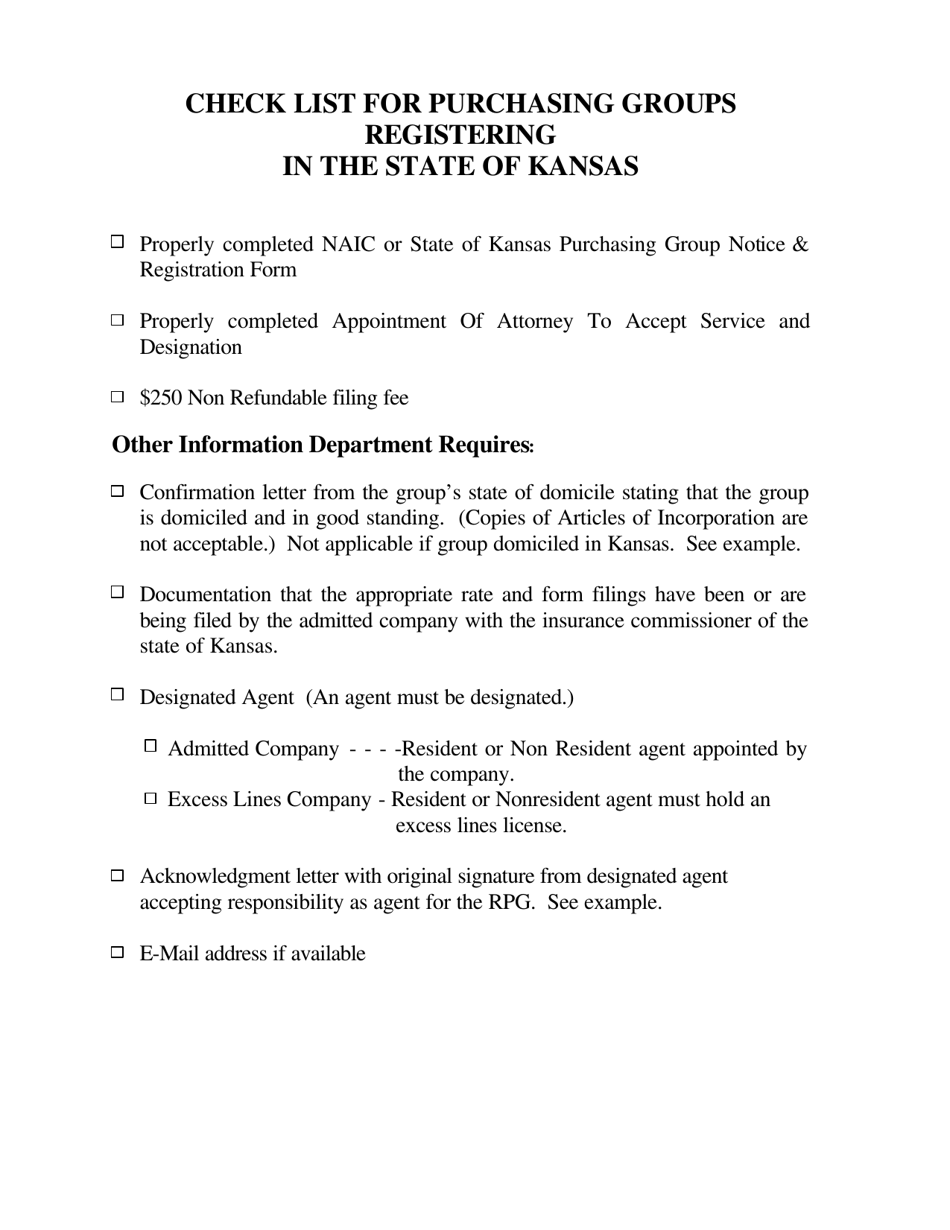

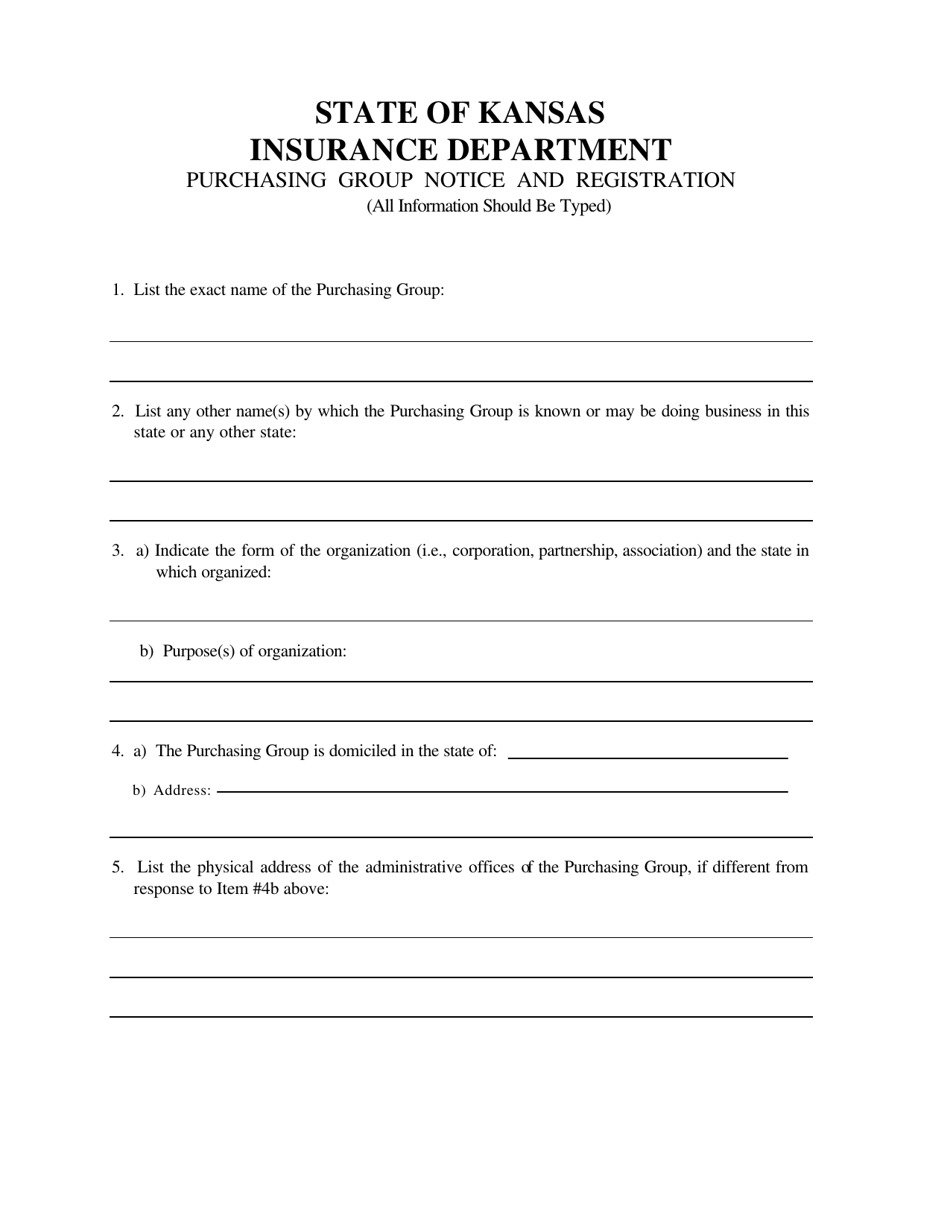

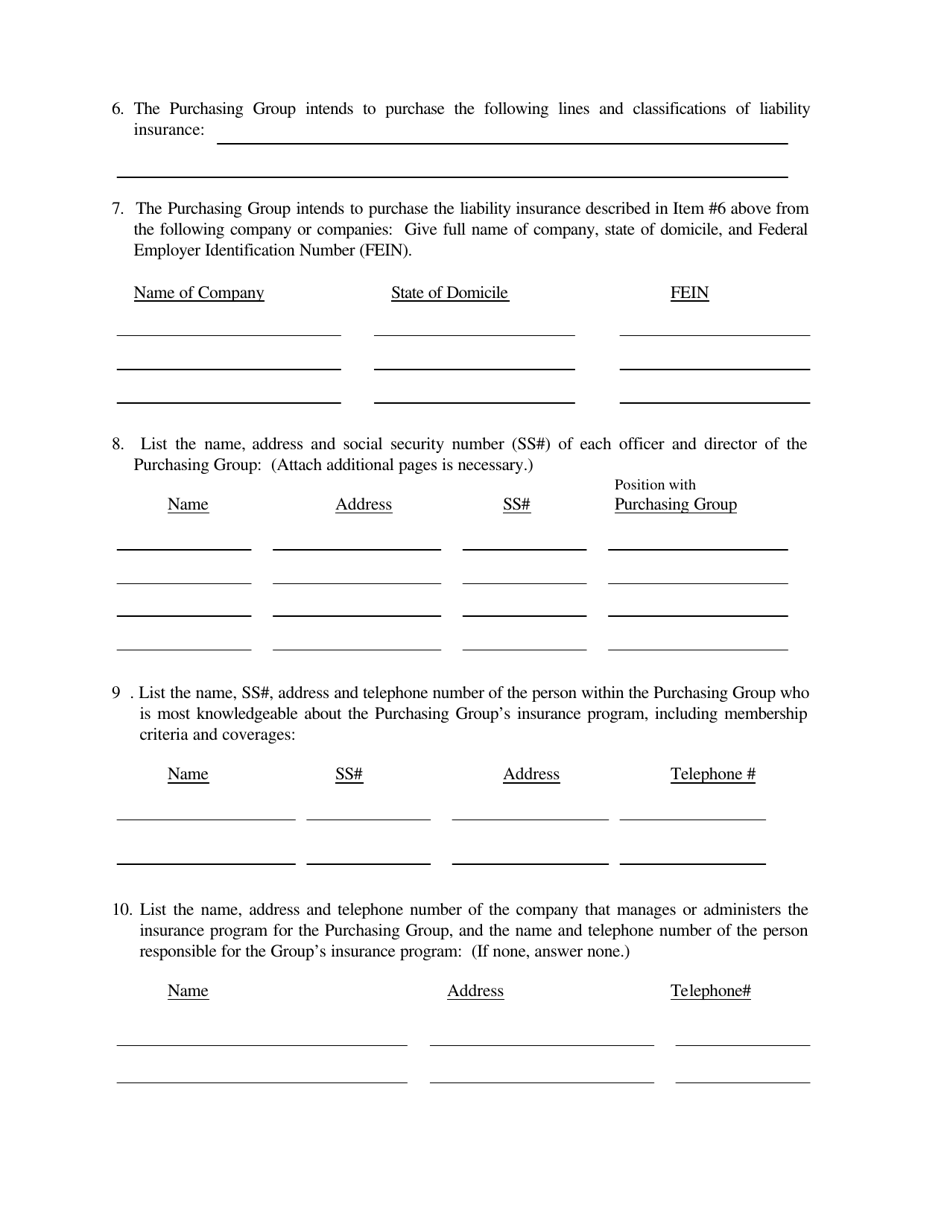

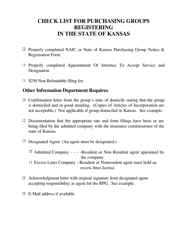

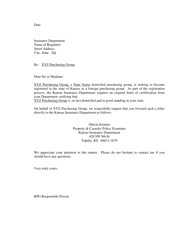

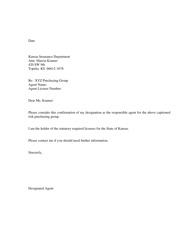

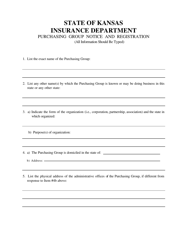

Purchasing Group Notice and Registration - Kansas

Purchasing Group Notice and Registration is a legal document that was released by the Kansas Insurance Department - a government authority operating within Kansas.

FAQ

Q: What is a Purchasing Group in Kansas?

A: A Purchasing Group in Kansas is an entity that is created to obtain liability insurance for its members.

Q: What is the purpose of registering a Purchasing Group in Kansas?

A: Registering a Purchasing Group in Kansas is necessary in order to comply with the state's laws and regulations regarding liability insurance coverage.

Q: Who is required to register a Purchasing Group in Kansas?

A: Any entity that meets the definition of a Purchasing Group and wants to obtain liability insurance for its members must register in Kansas.

Q: How can a Purchasing Group register in Kansas?

A: A Purchasing Group can register in Kansas by submitting the required application and fees to the Kansas Insurance Department.

Q: What are the consequences of operating an unregistered Purchasing Group in Kansas?

A: Operating an unregistered Purchasing Group in Kansas can result in legal penalties and may also affect the ability to obtain liability insurance coverage.

Form Details:

- The latest edition currently provided by the Kansas Insurance Department;

- Ready to use and print;

- Easy to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a printable version of the form by clicking the link below or browse more documents and templates provided by the Kansas Insurance Department.

Download Purchasing Group Notice and Registration - Kansas

1

2

3

4

5

6

7

8

9

10

11

12