![]() This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form W-8BEN-E

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form W-8BEN-E

for the current year.

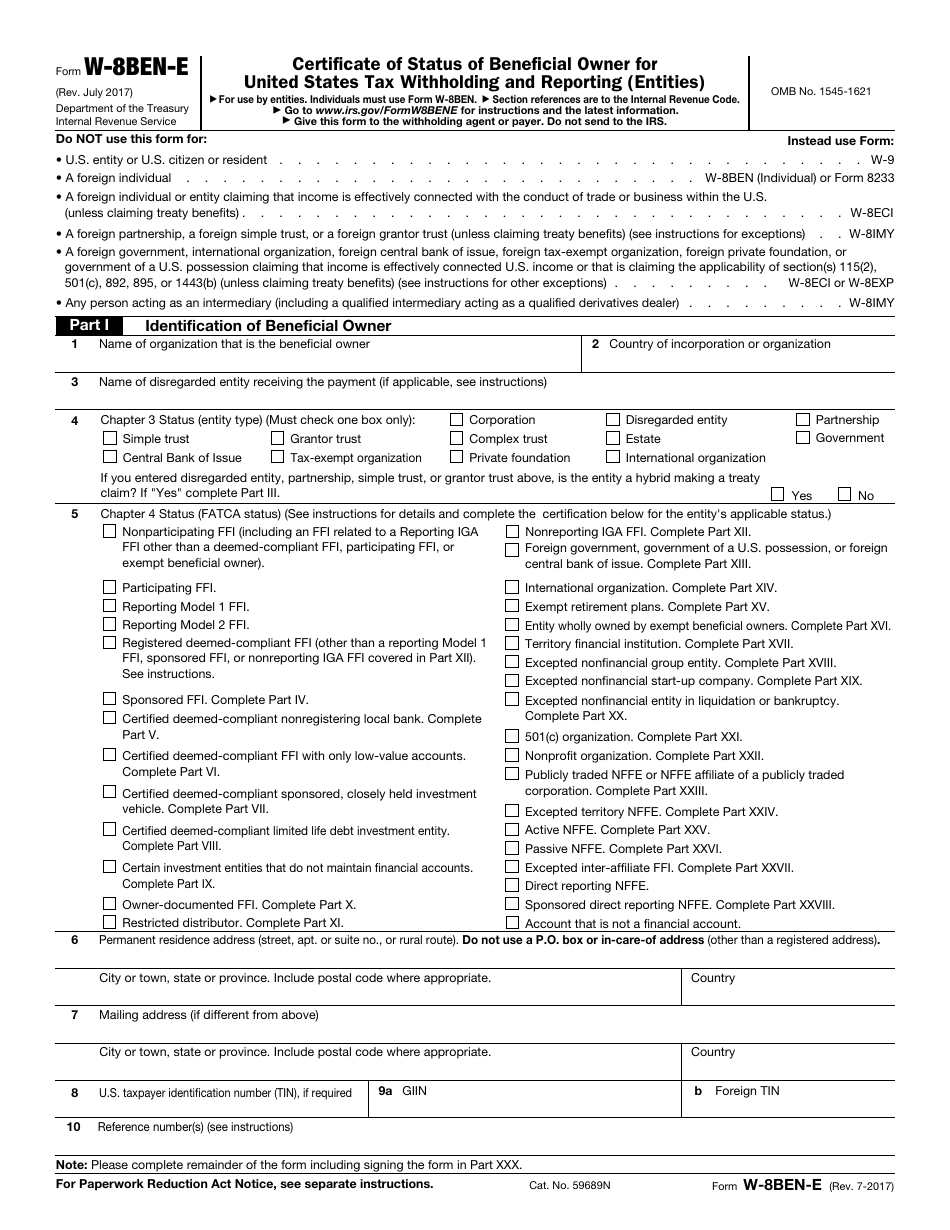

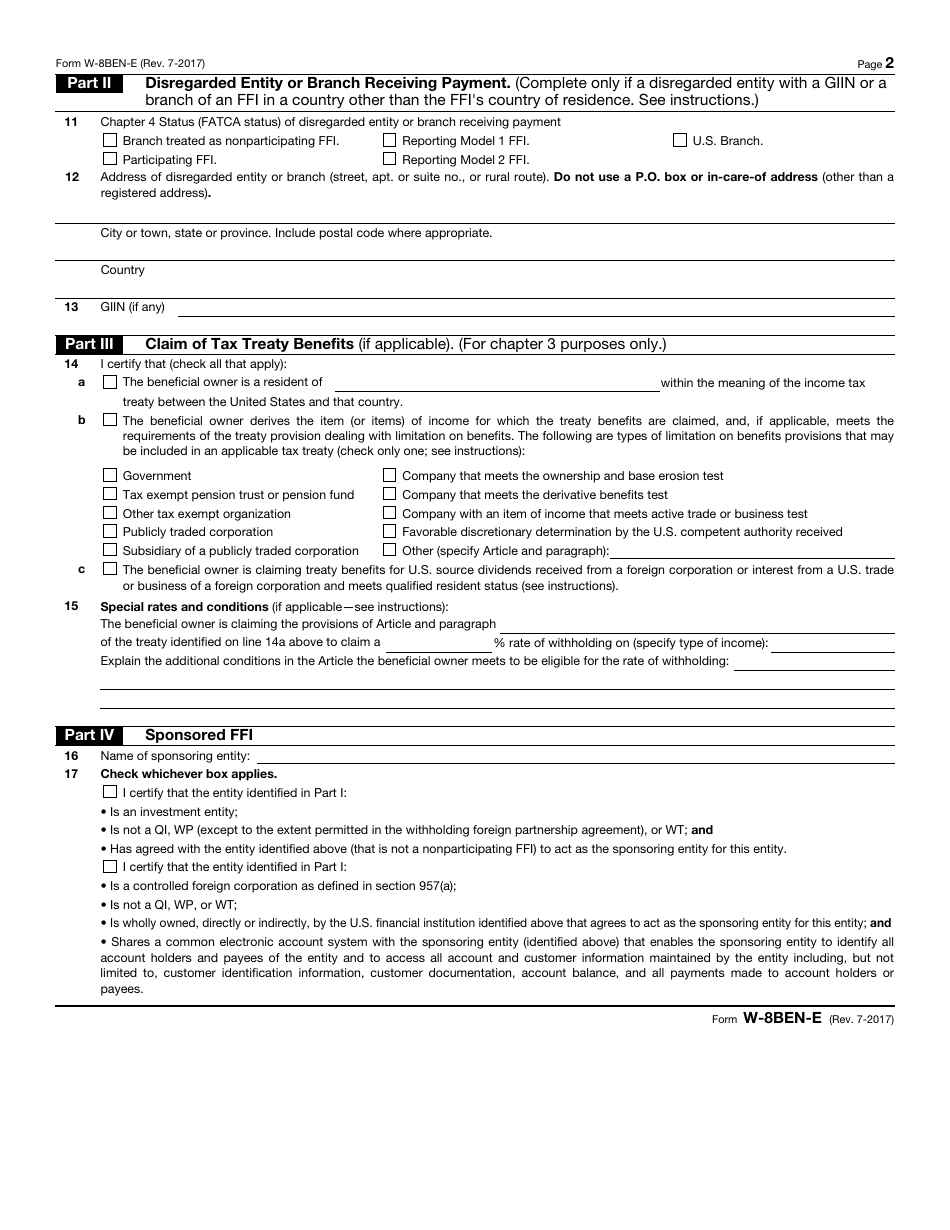

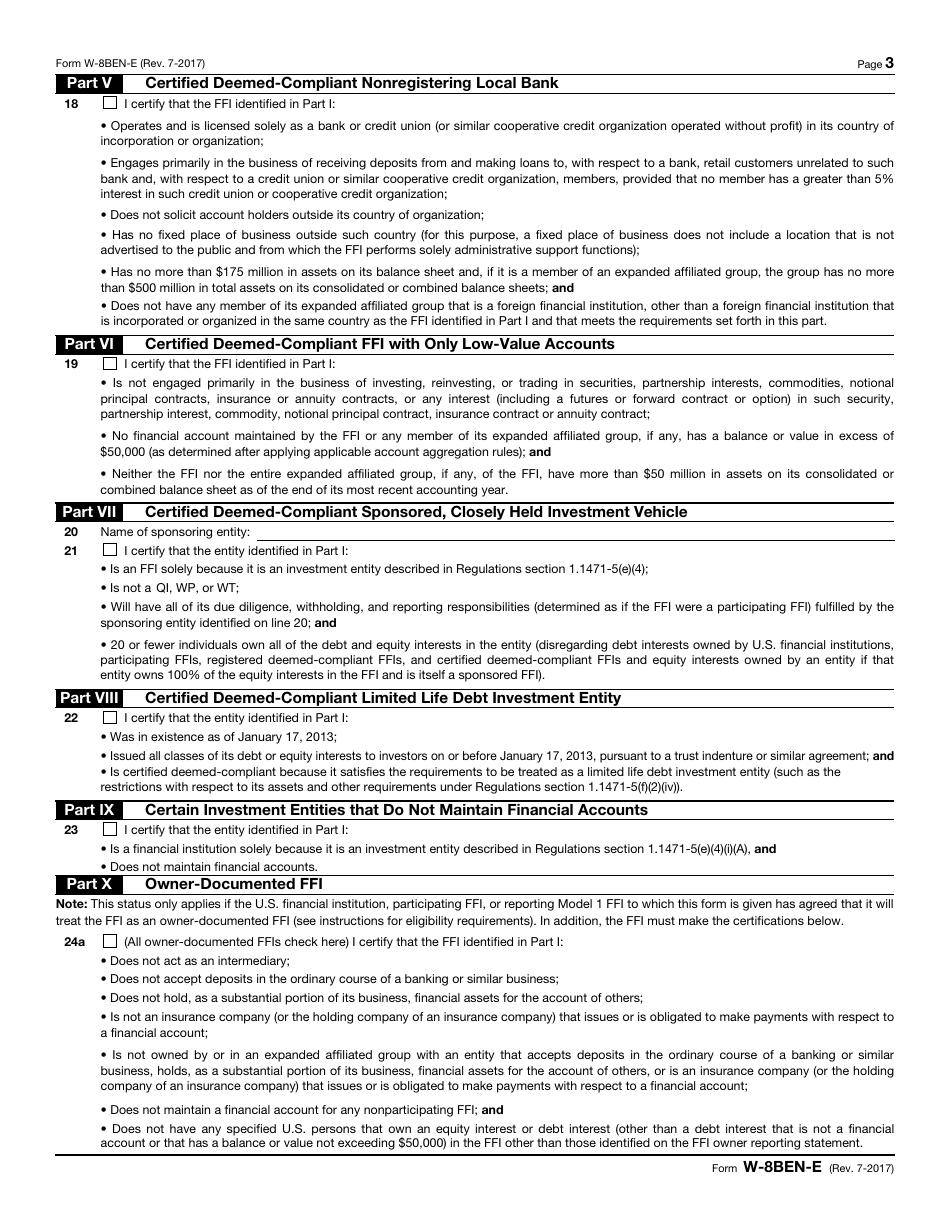

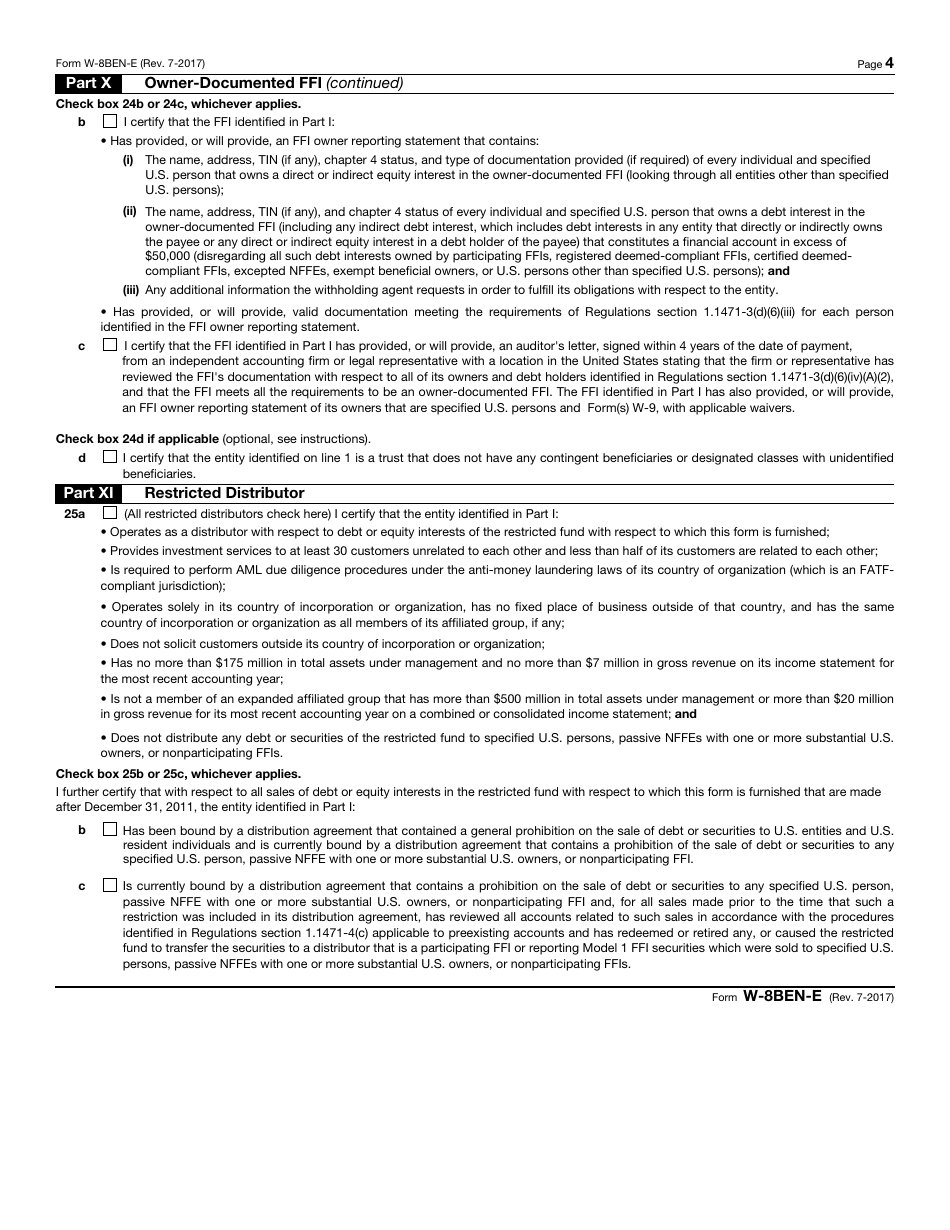

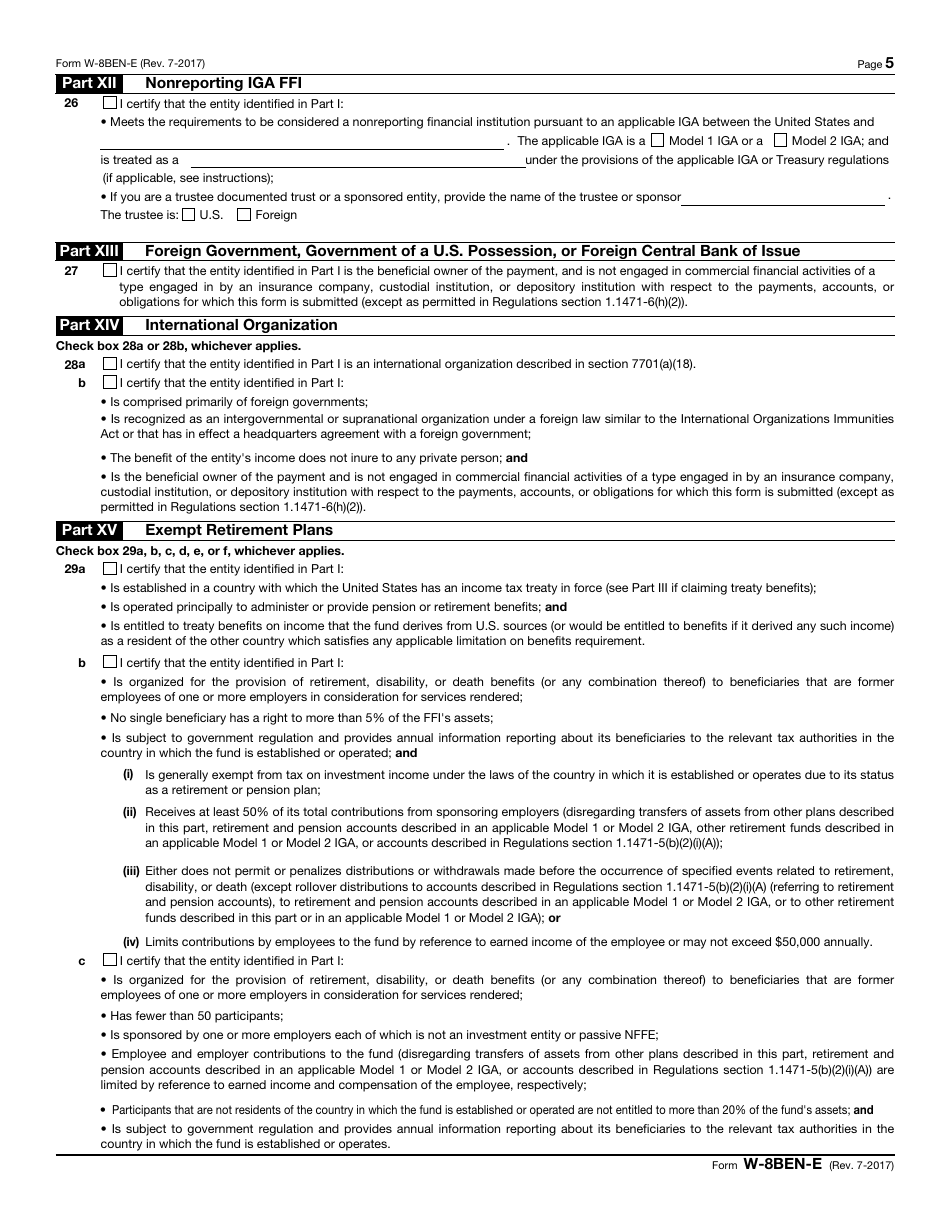

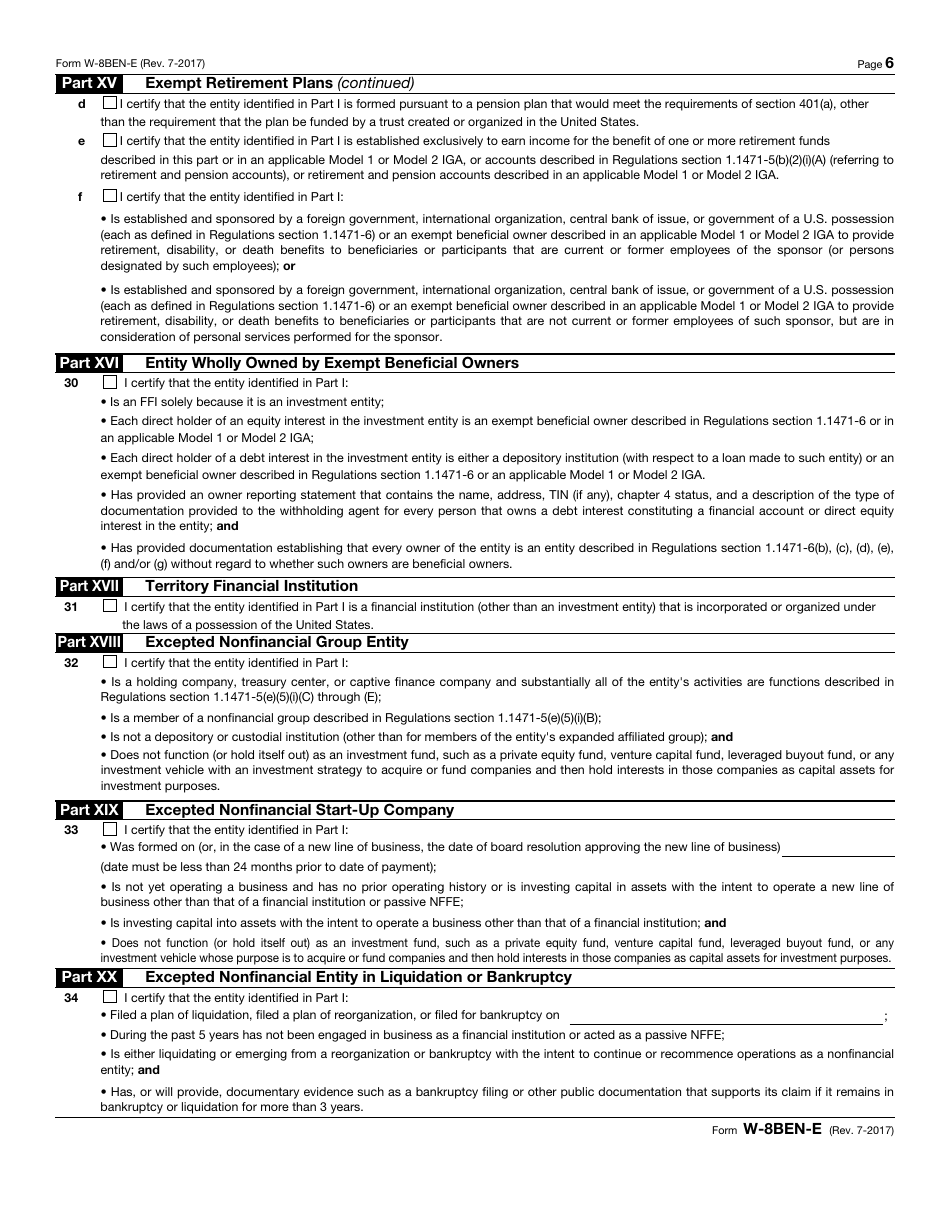

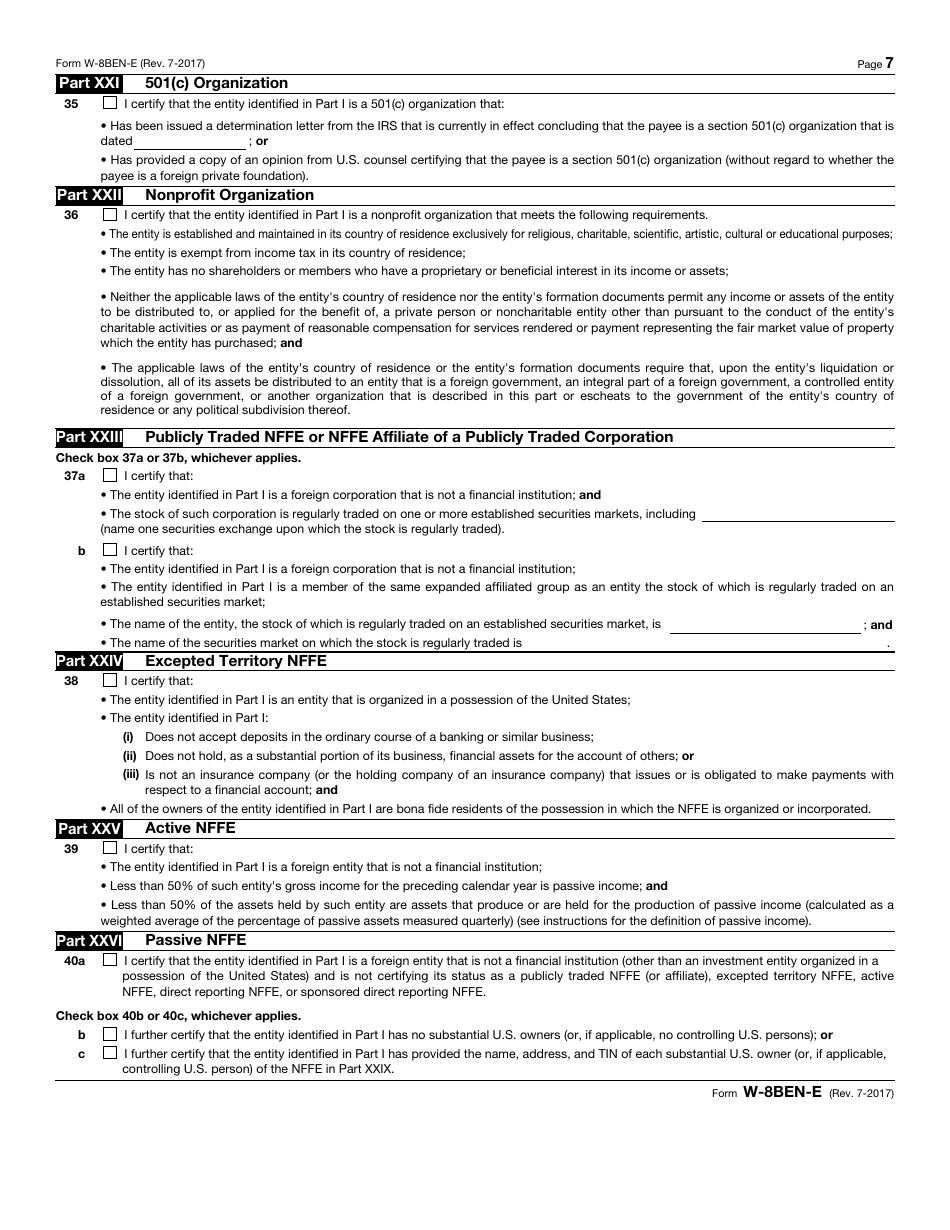

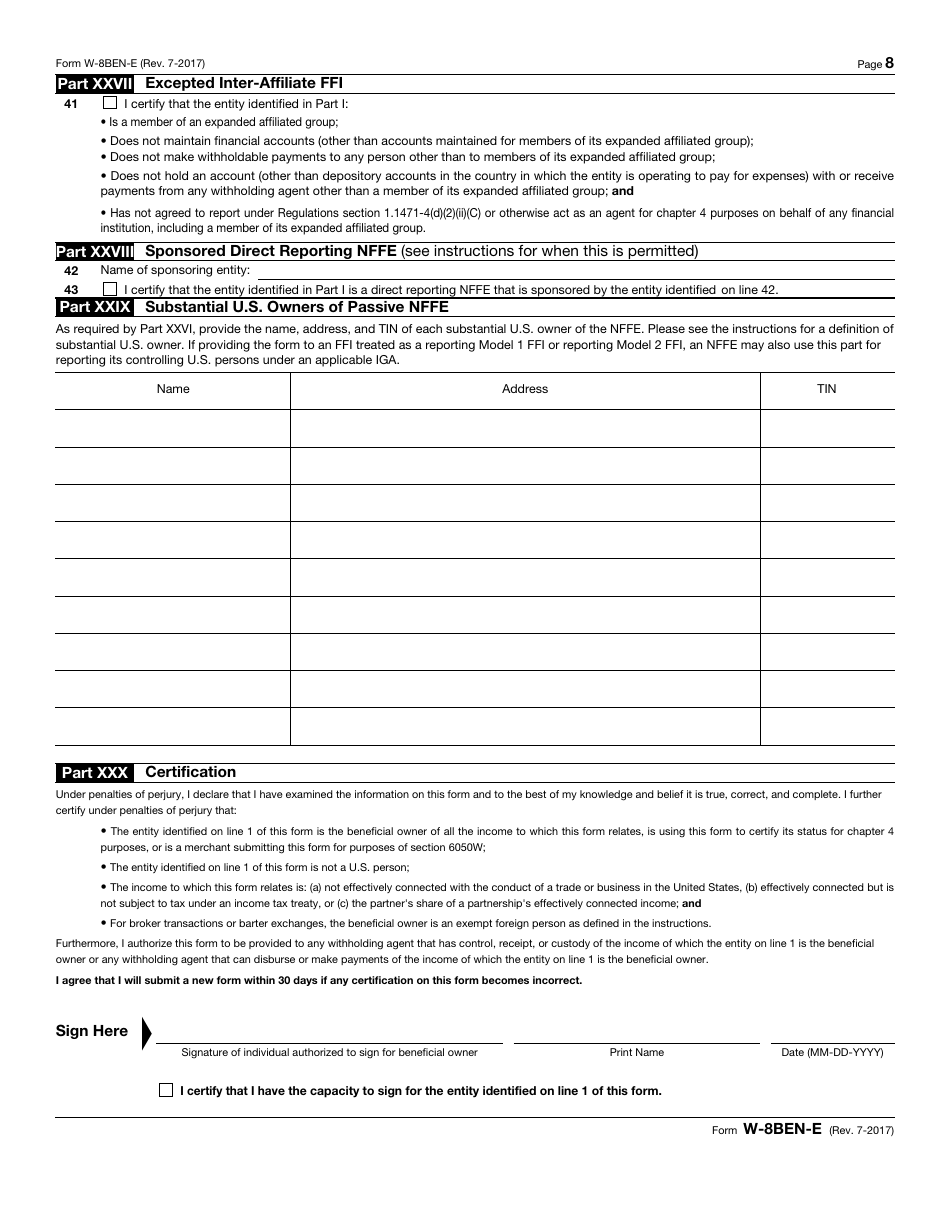

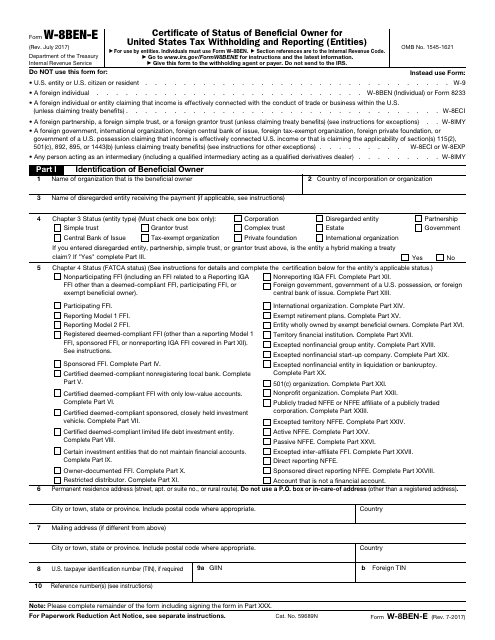

IRS Form W-8BEN-E Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities)

What Is IRS Form W-8BEN-E?

This is a tax form that was released by the Internal Revenue Service (IRS) - a subdivision of the U.S. Department of the Treasury on July 1, 2017. Check the official IRS-issued instructions before completing and submitting the form.

FAQ

Q: What is IRS Form W-8BEN-E?

A: IRS Form W-8BEN-E is a certification form used by foreign entities to establish their status as beneficial owners for the purpose of US tax withholding and reporting.

Q: Who needs to fill out IRS Form W-8BEN-E?

A: Foreign entities that receive income from US sources need to fill out IRS Form W-8BEN-E.

Q: What is the purpose of IRS Form W-8BEN-E?

A: The purpose of IRS Form W-8BEN-E is to establish the foreign entity's eligibility for reduced or exempted withholding tax rates on income received from US sources.

Q: What information is required on IRS Form W-8BEN-E?

A: IRS Form W-8BEN-E requires information such as the entity's name, address, country of residence, tax identification number, and details of any applicable tax treaty benefits.

Q: Are there any penalties for non-compliance?

A: Yes, failure to provide a completed and valid IRS Form W-8BEN-E may result in the application of backup withholding tax rates on income received from US sources.

Form Details:

- A 8-page form available for download in PDF;

- Actual and valid for filing 2023 taxes;

- Editable, printable, and free;

- Fill out the form in our online filing application.

Download a fillable version of IRS Form W-8BEN-E through the link below or browse more documents in our library of IRS Forms.

Download IRS Form W-8BEN-E Certificate of Status of Beneficial Owner for United States Tax Withholding and Reporting (Entities)

1

2

3

4

5

6

7

8