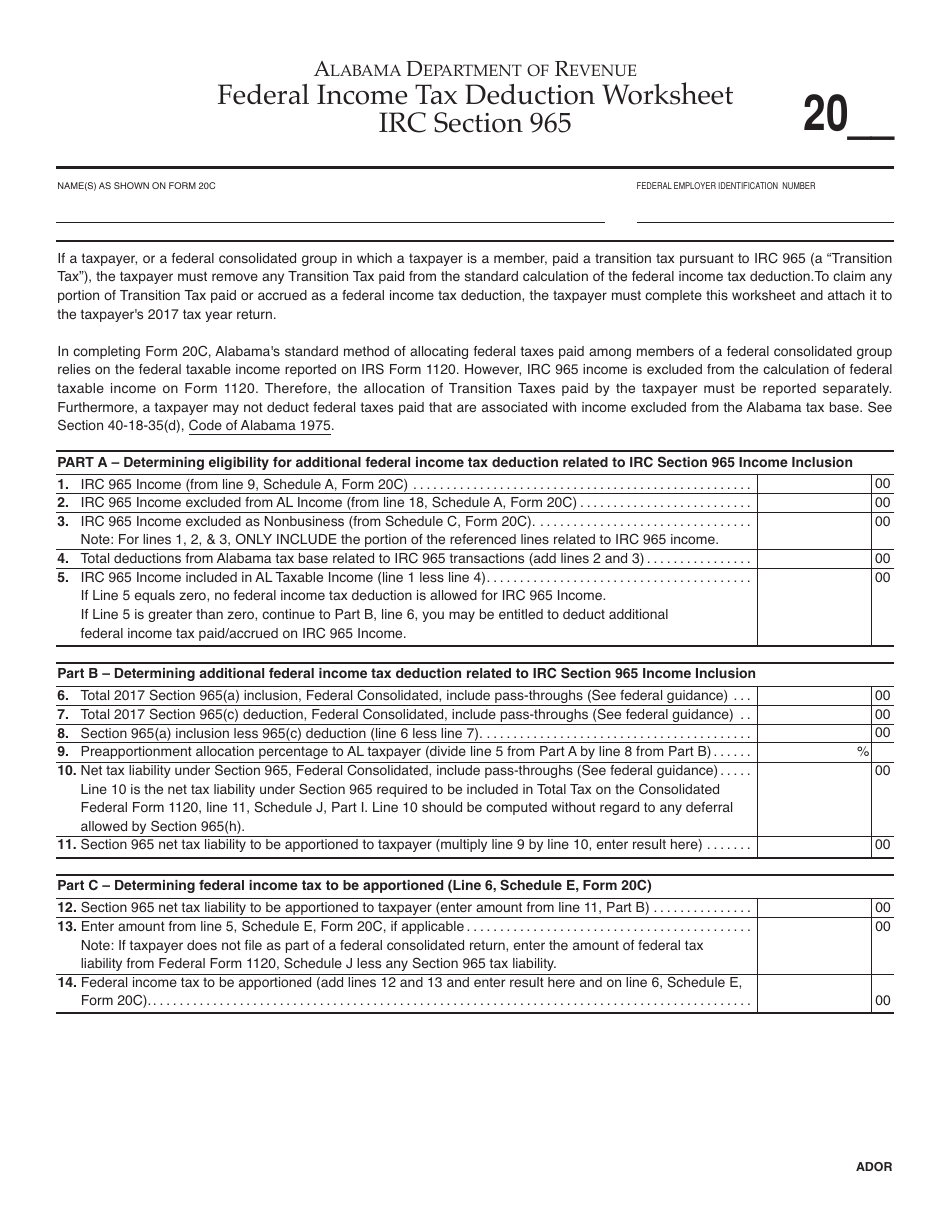

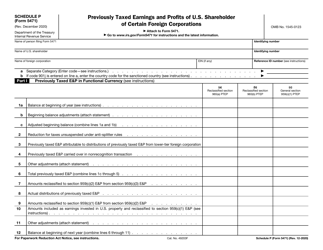

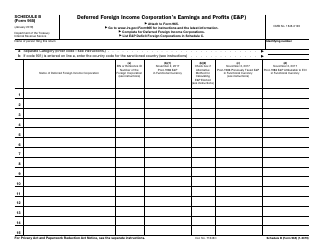

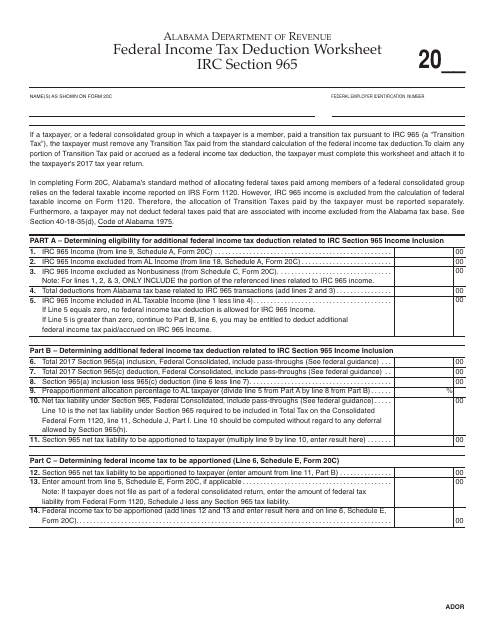

Federal Income Tax Deduction Worksheet IRC Section 965 - Alabama

Federal Income Tax Deduction Worksheet IRC Section 965 is a legal document that was released by the Alabama Department of Revenue - a government authority operating within Alabama.

FAQ

Q: What is the Federal IncomeTax Deduction Worksheet?

A: The Federal Income Tax Deduction Worksheet is a document that helps individuals calculate their deductions for federal income tax purposes.

Q: What does IRC Section 965 refer to?

A: IRC Section 965 refers to a provision in the Internal Revenue Code that relates to the taxation of certain foreign income.

Q: How does the Federal Income Tax Deduction Worksheet relate to Alabama?

A: The Federal Income Tax Deduction Worksheet is a general document applicable to federal income tax calculations and does not specifically pertain to Alabama.

Q: What is the purpose of the Federal Income Tax Deduction Worksheet?

A: The purpose of the Federal Income Tax Deduction Worksheet is to help individuals determine their allowable deductions for federal income tax purposes.

Q: Who can use the Federal Income Tax Deduction Worksheet?

A: The Federal Income Tax Deduction Worksheet can be used by individuals who need to calculate their federal income tax deductions.

Form Details:

- The latest edition currently provided by the Alabama Department of Revenue;

- Ready to use and print;

- Easy to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of the form by clicking the link below or browse more documents and templates provided by the Alabama Department of Revenue.