![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form NYS-45

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Instructions for Form NYS-45

for the current year.

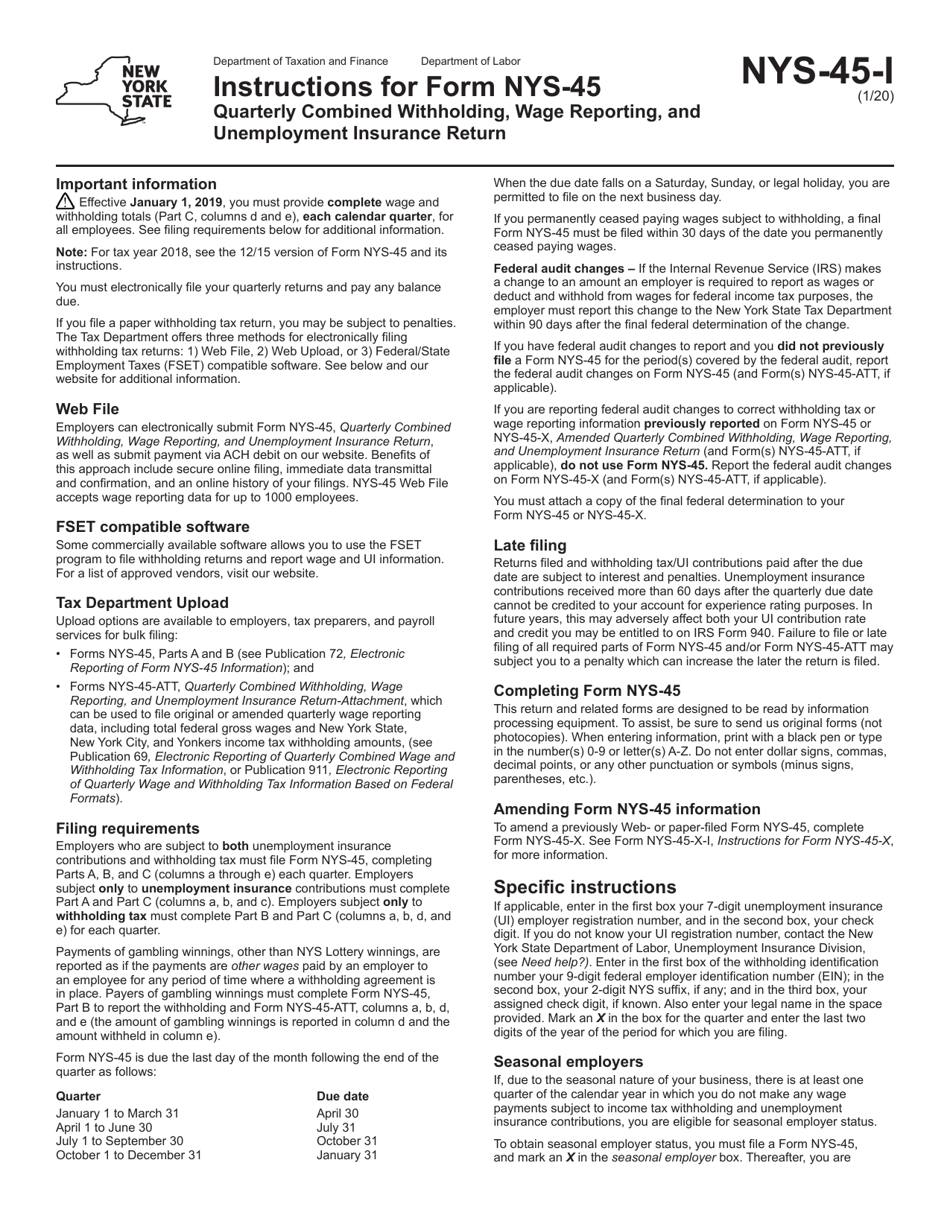

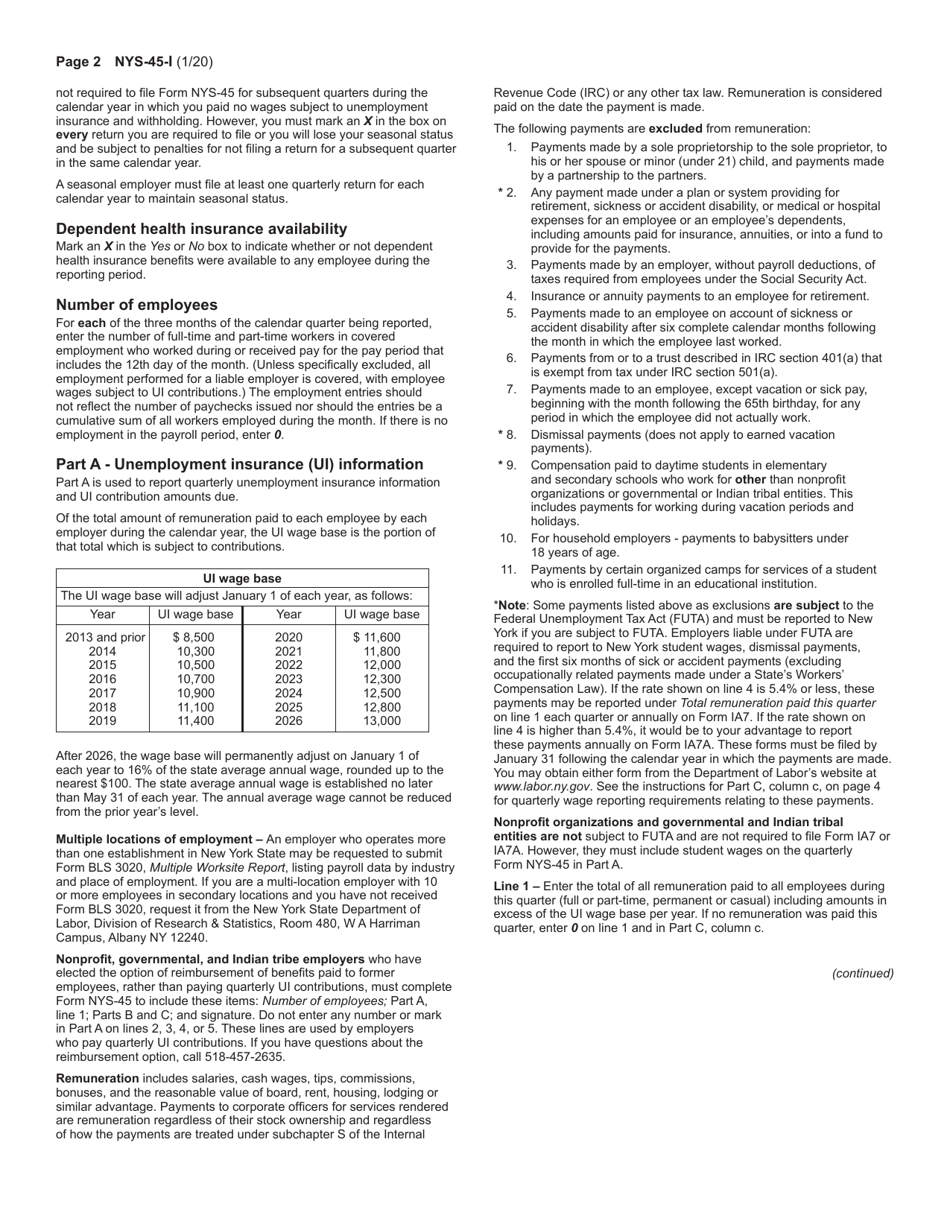

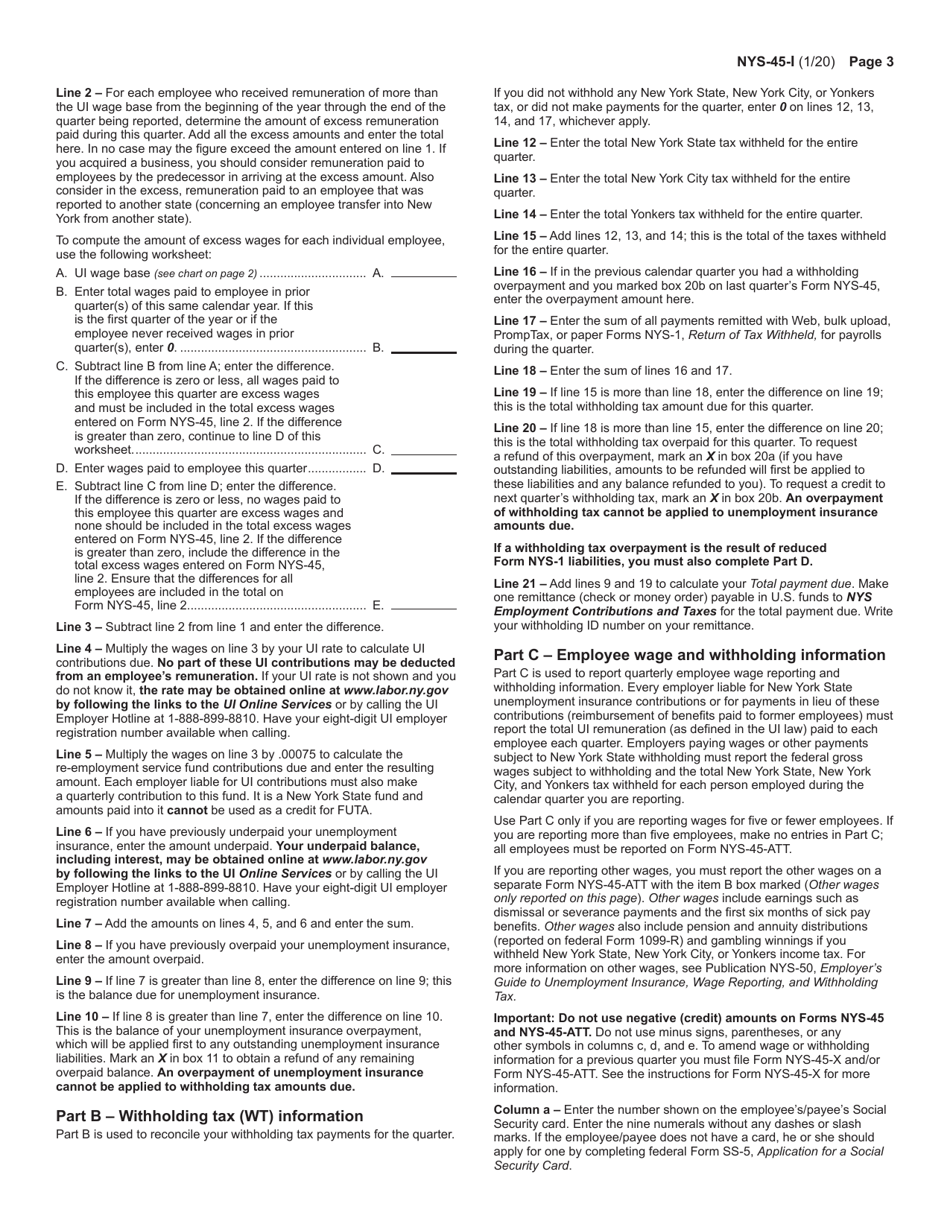

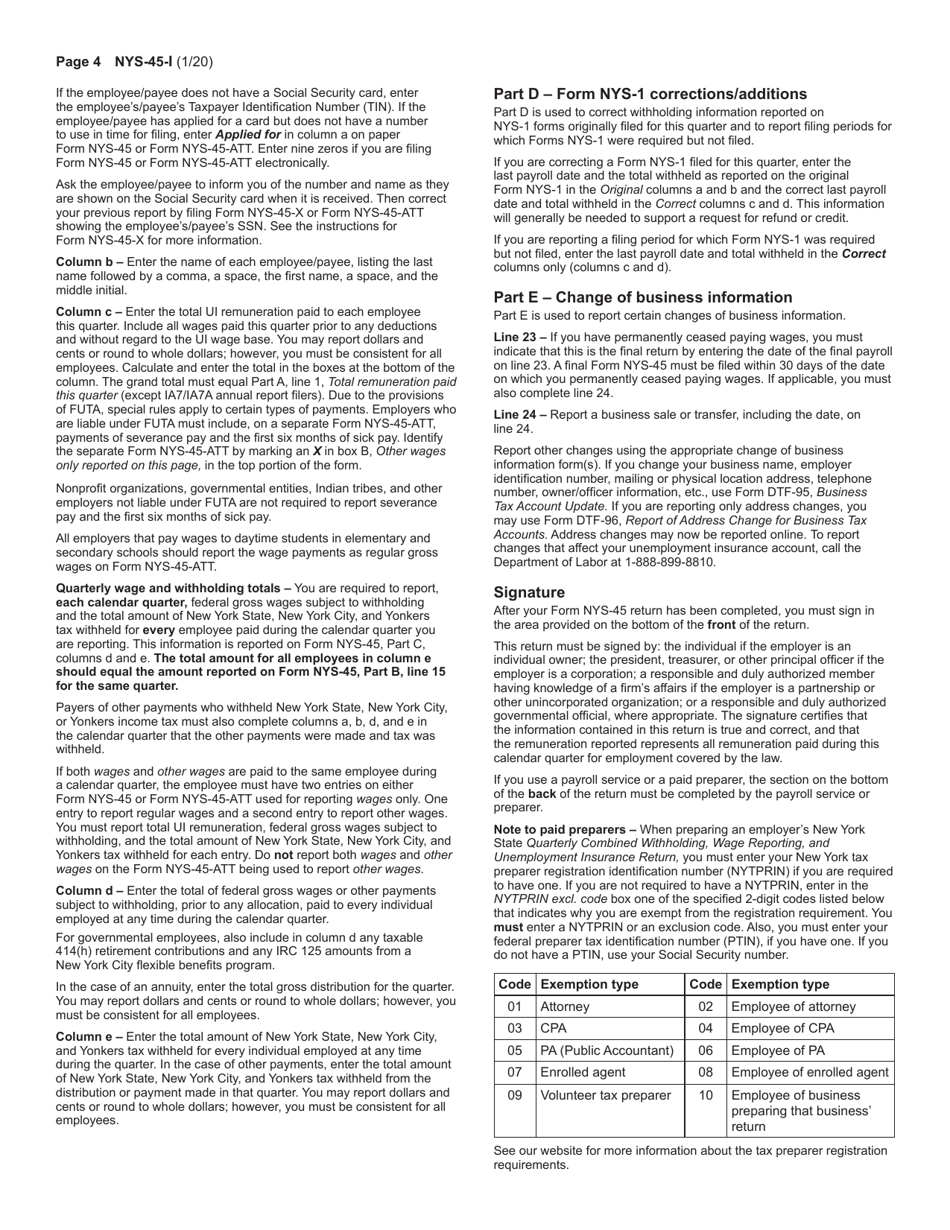

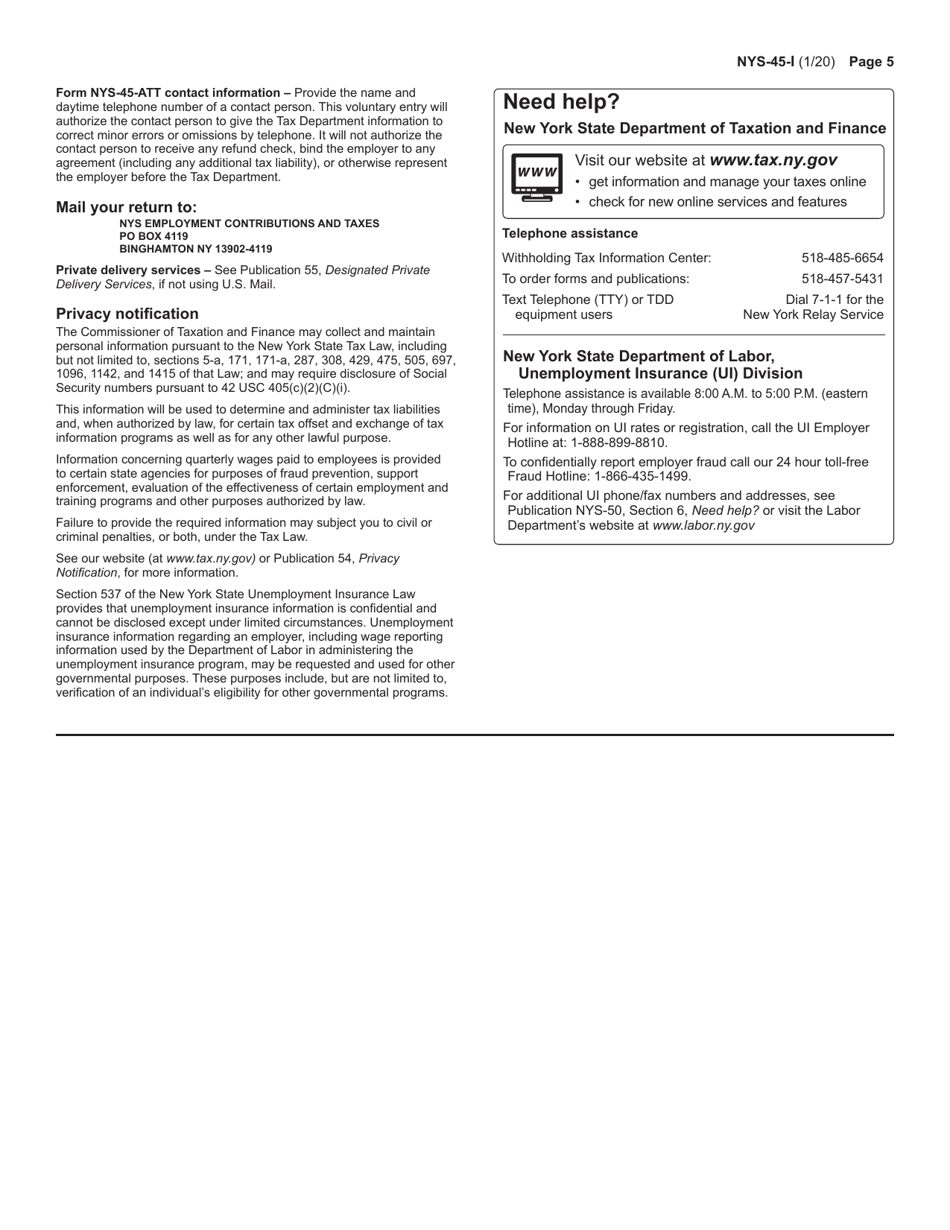

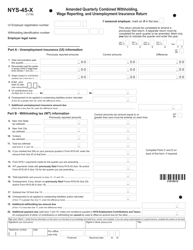

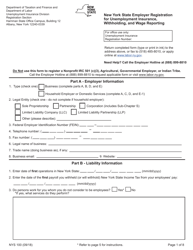

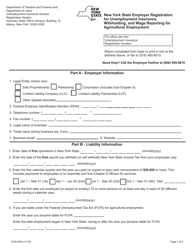

Instructions for Form NYS-45 Quarterly Combined Withholding, Wage Reporting, and Unemployment Insurance Return - New York

This document contains official instructions for Form NYS-45 , Quarterly Combined Withholding, Wage Reporting, and Unemployment Insurance Return - a form released and collected by the New York State Department of Taxation and Finance. An up-to-date fillable Form NYS-45 is available for download through this link.

FAQ

Q: What is Form NYS-45?

A: Form NYS-45 is a quarterly combined withholding, wage reporting, and unemployment insurance return in New York.

Q: What is the purpose of Form NYS-45?

A: The purpose of Form NYS-45 is to report wages, tips, and other compensation paid to employees, as well as the amount of taxes withheld.

Q: Who must file Form NYS-45?

A: Employers in New York who have employees and withhold taxes from wages must file Form NYS-45.

Q: Is Form NYS-45 only filed quarterly?

A: Yes, Form NYS-45 is filed quarterly, meaning it must be filed four times a year.

Q: What information is required on Form NYS-45?

A: Form NYS-45 requires information such as employer identification number (EIN), total wages paid, total New York State tax withheld, etc.

Q: Are there any penalties for not filing Form NYS-45?

A: Yes, there are penalties for not filing or filing late, including monetary fines and possible legal consequences.

Q: Do I need to keep a copy of Form NYS-45 for my records?

A: Yes, it is recommended to keep a copy of Form NYS-45 for your records for at least four years.

Instruction Details:

- This 5-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the New York State Department of Taxation and Finance.

Download Instructions for Form NYS-45 Quarterly Combined Withholding, Wage Reporting, and Unemployment Insurance Return - New York

1

2

3

4

5