![]() This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 3520

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 3520

for the current year.

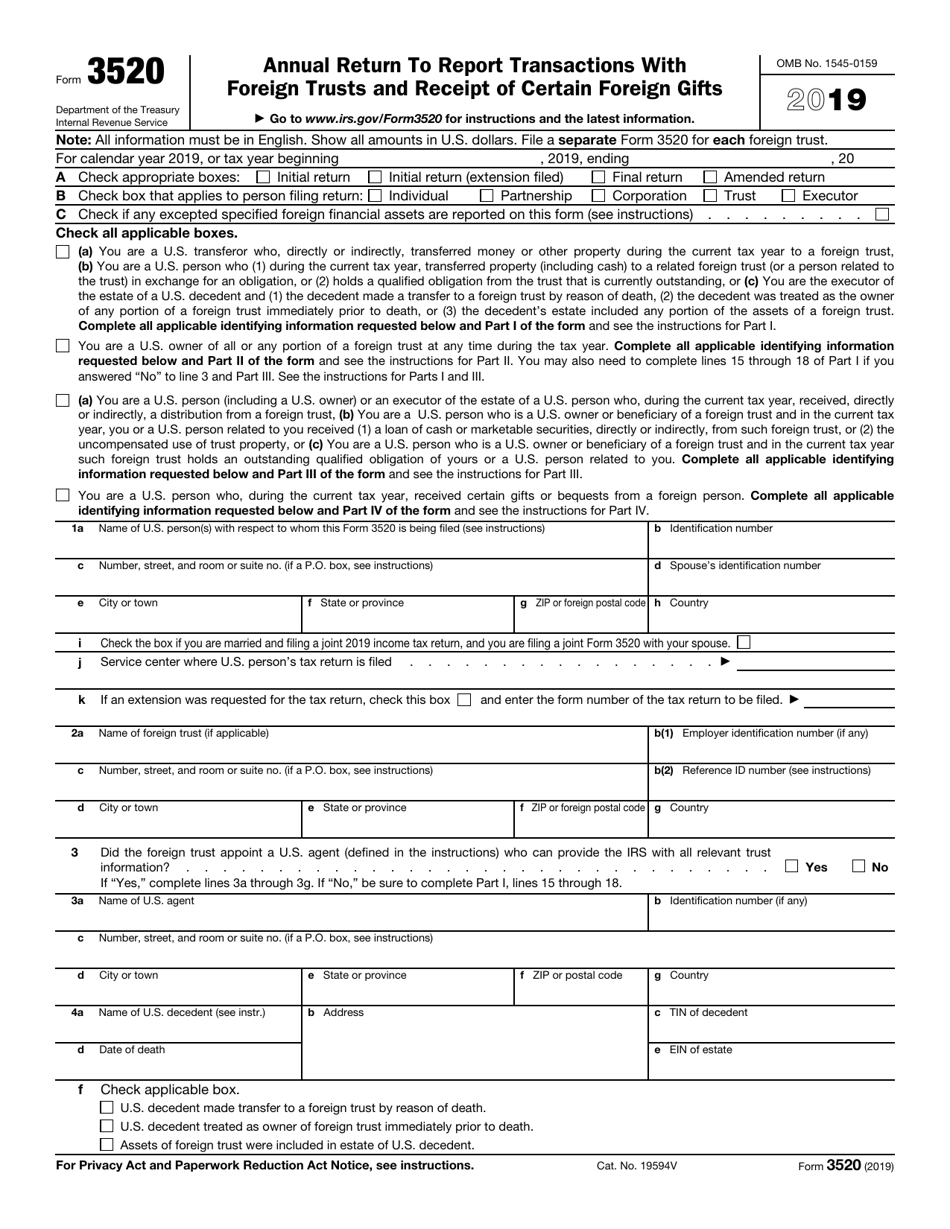

IRS Form 3520 Annual Return to Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts

What Is IRS Form 3520?

IRS Form 3520, Annual Return to Foreign Trusts and Receipt of Certain Foreign Gifts , is a form filed with the tax authorities by persons from the United States (and also executors of estates of U.S. deceased) in order to report certain transactions with foreign trusts; ownership of foreign trusts; and receipt of certain gifts or bequests from foreigners.

Alternate Name:

- IRS Foreign Trust Form.

This form was issued by the Internal Revenue Service (IRS) and was last revised in 2019 . А fillable version of the Foreign Trust Form 3520 can be found below.

What Is the Difference Between Form 3520 and 3520-A?

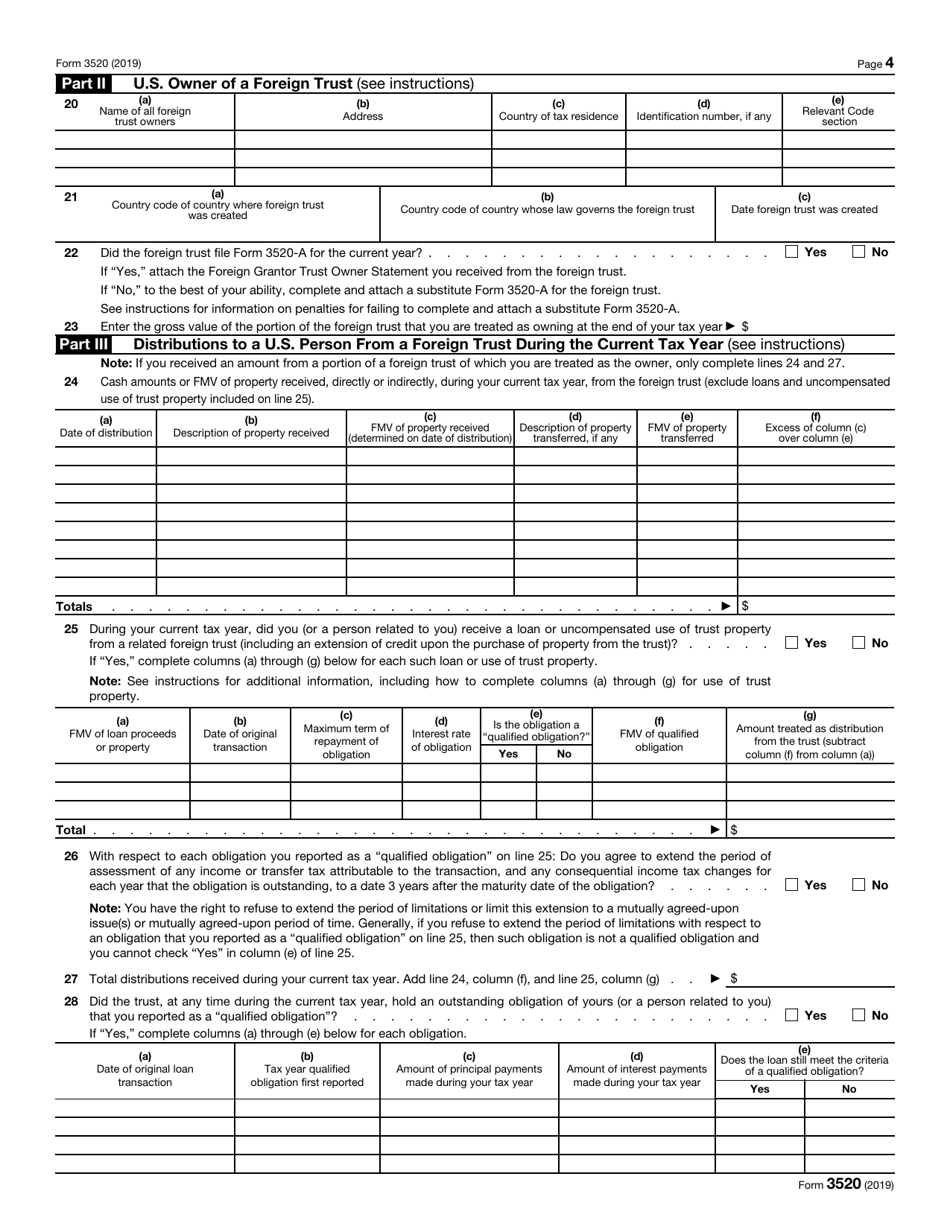

These forms are related, but Form 3520 is filed by U.S. persons to inform the IRS of a reportable event for the tax year, while Form 3520-A is filed by foreign trusts. The purpose of IRS Form 3520-A is to provide information about a foreign trust that has at least one U.S. owner, as well as about its U.S. beneficiaries and U.S. owners.

IRS Form 3520 Instructions

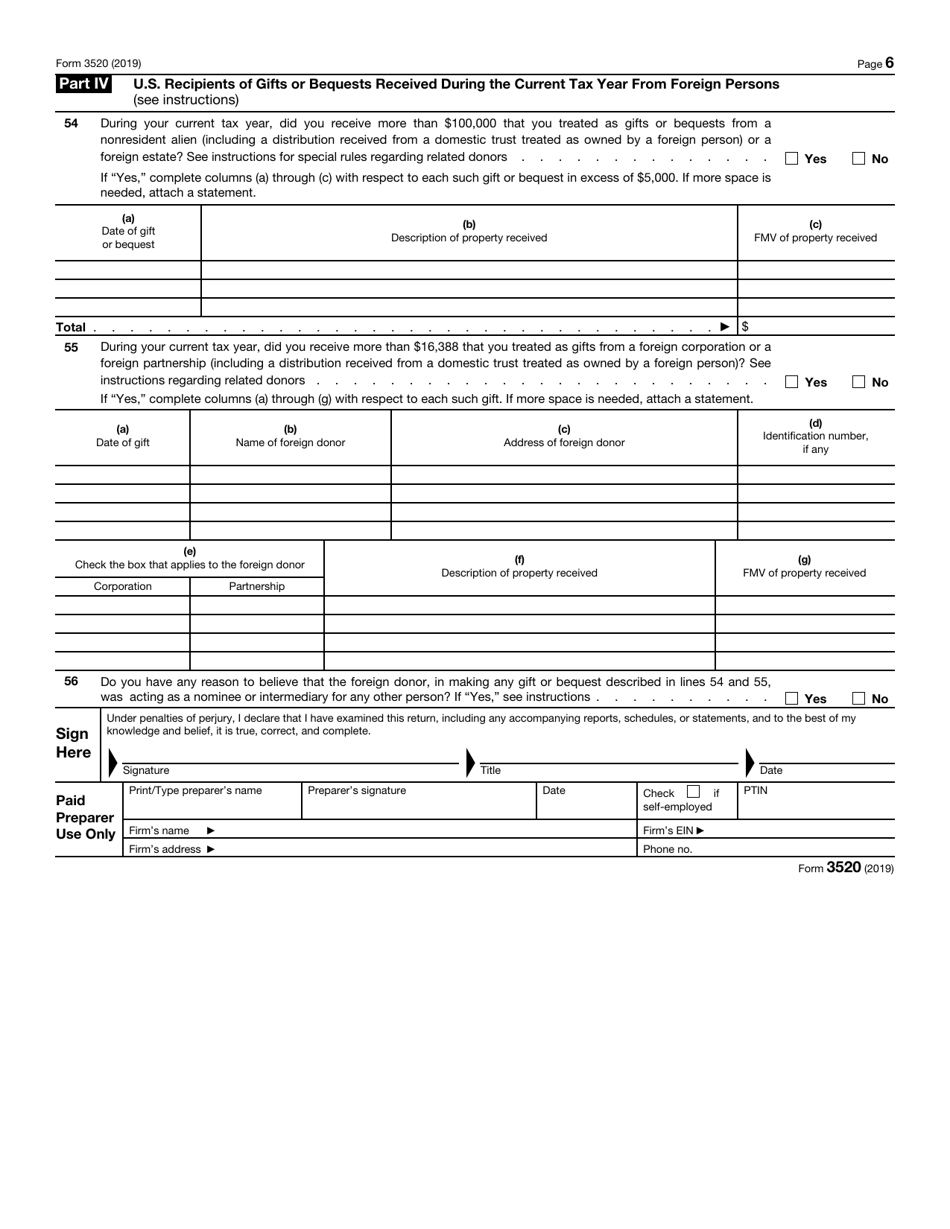

A "foreign gift" is money or property received by a U.S. recipient from a foreign person that the recipient excludes from their gross income and treats as a gift or bequest. A "foreign person" may refer to a foreign individual, partnership, corporation, or an estate.

A U.S. person must file tax form 3520 by the 15th day of the 4th month following the end of their tax year. However, if the U.S. citizens or residents live and work outside of the U.S. and Puerto Rico, the due date is on the 15th day of the 6th month that follows the end of their tax year. In cases when the form is filed with regards to a U.S. decedent, the due date for filing the return is the 15th day of the 4th month after the end of the decedent's last tax year. If the due date falls on a legal holiday or a weekend, the form is due on the next business day. If a U.S. person is granted an extension to file the return, the due date is the 15th day of the 10th month after the end of the U.S. person's tax year.

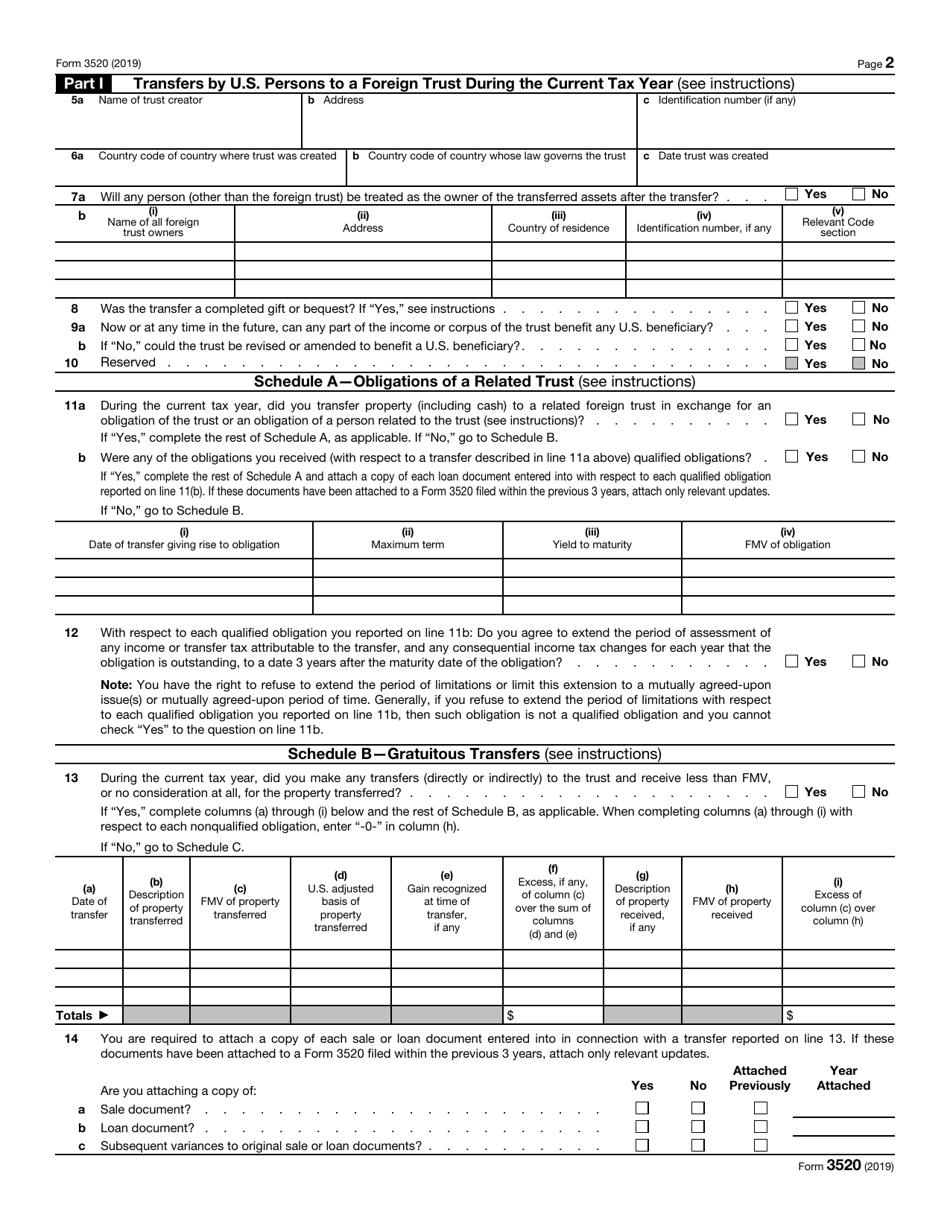

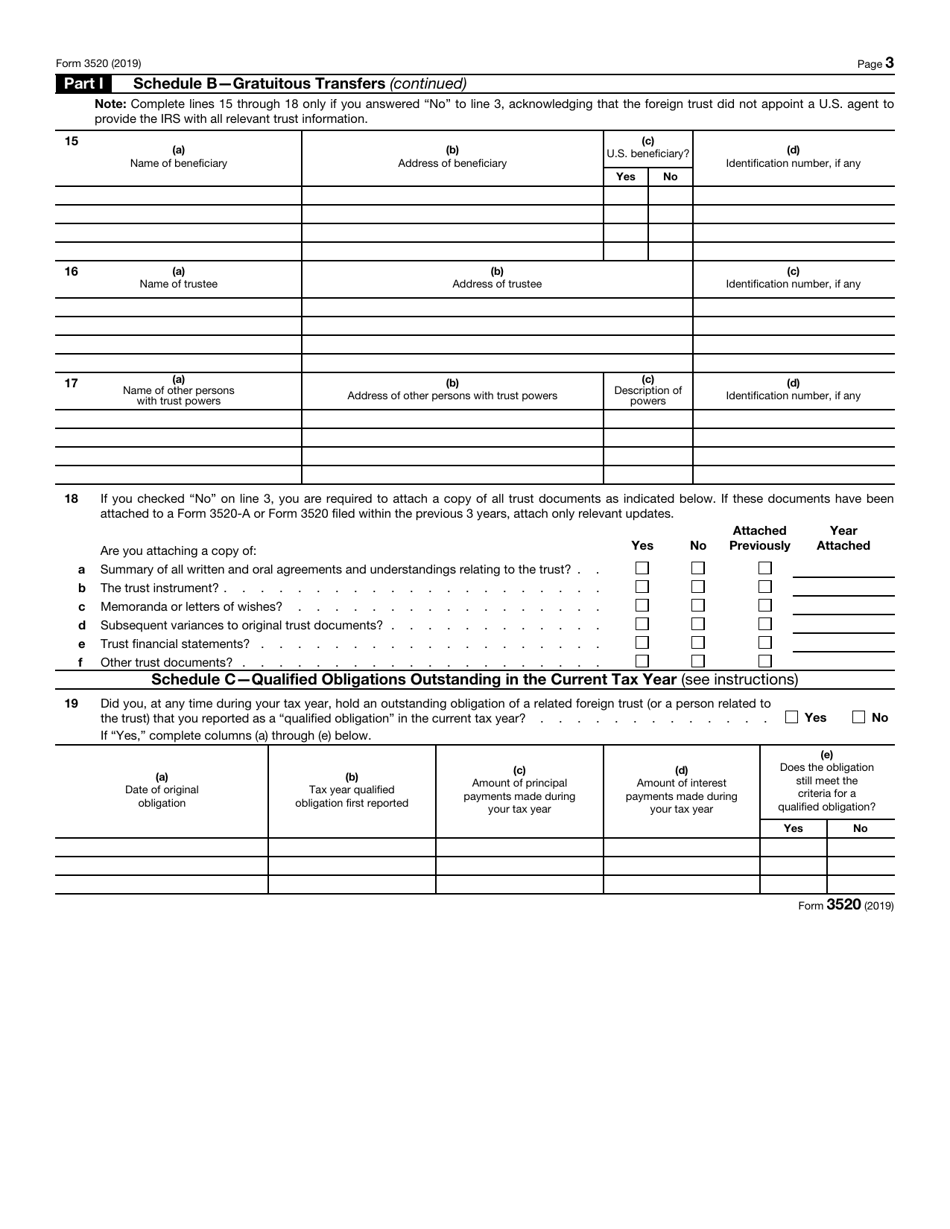

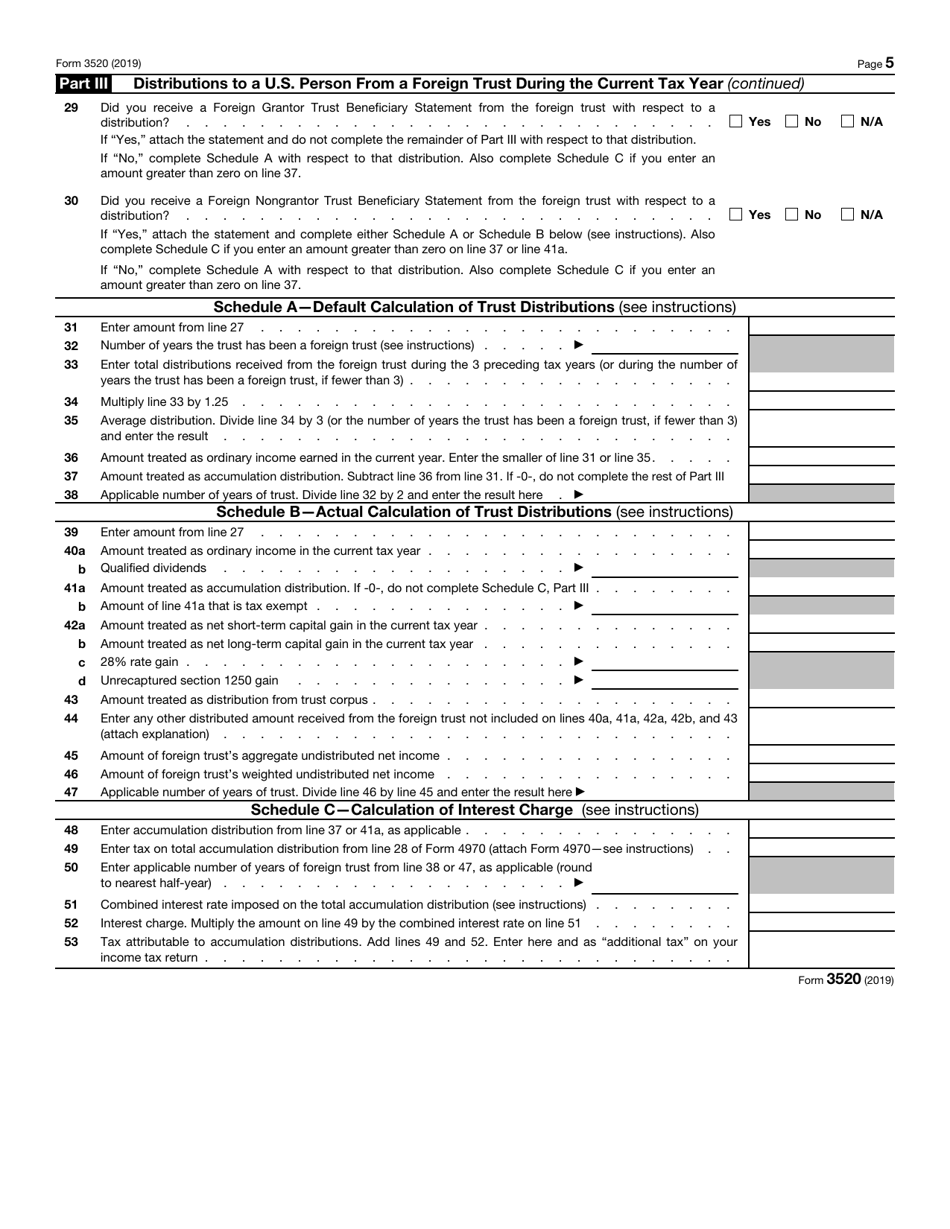

U.S. persons must file separate forms for transactions with each foreign trust. Although there is no U.S. tax on foreign gifts, significant penalties are imposed for failure to file Form 3520 when it is required. The penalty for not filing or incomplete filing amounts to the greater of $10,000 or any of the following, as applicable: (a) 35% of the gross value of any property that was transferred to a foreign trust; (b) 35% of the gross value of the distributions that were received from a foreign trust; and (c) 5% of the gross value of the foreign trust's assets owned by a U.S. person under the grantor trust rules. Additional penalties will be imposed if the failure to comply continues for 90 days or more after the IRS serves notification about the noncompliance. In cases when the taxpayer can show that the failure to comply was due to a reasonable cause, however, no penalties will be imposed.

Note that there are special rules on gifts or bequests received from covered expatriates, where a foreign gifts tax applies. The IRS provides specific filing requirements in the official instructions for Form 3520.

How to File IRS Form 3520?

File Form 3520 and your income tax return separately. The IRS 3520 form must have all required attachments to be considered complete.

The 3520 form must be consistent with Form 3520-A, unless you report an inconsistency to the IRS. If you are treating items on 3520 differently from the way a foreign trust treated them on 3520-A, you must file Form 8082, Notice of Inconsistent Treatment or Administrative Adjustment Request.

If an individual or a fiduciary file the return, they must sign the form. If the form is filed by a partnership, it must be signed by a general partner or company member. If the return is filed by a corporation, it must be authorized by the signature of the president, vice president, chief accounting officer, treasurer, assistant treasurer, or any other corporate officer authorized to sign. If the information is completed by a paid preparer, they must sign the return in the space provided, as well as give a copy of the return to the filer.

Where to Mail Form 3520?

Form 3520 must be mailed to the following address: Internal Revenue Service Center, PO Box 409101, Ogden, Utah 84409

Download IRS Form 3520 Annual Return to Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts

1

2

3

4

5

6