![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form CDTFA-410-D

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form CDTFA-410-D

for the current year.

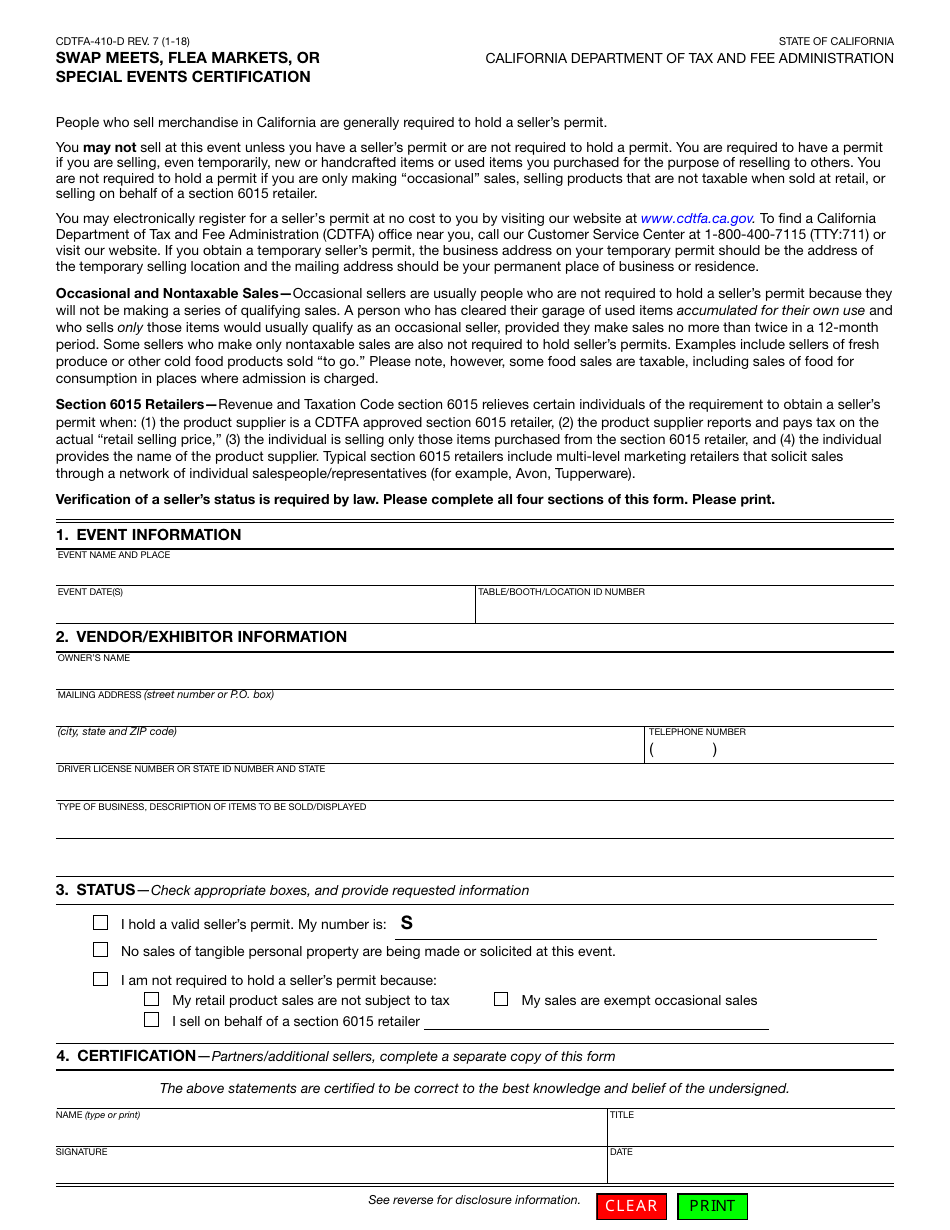

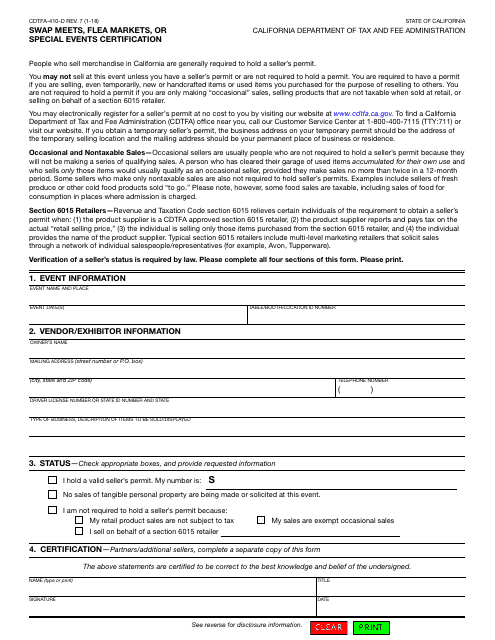

Form CDTFA-410-D Swap Meets, Flea Markets, or Special Events Certification - California

What Is Form CDTFA-410-D?

This is a legal form that was released by the California Department of Tax and Fee Administration - a government authority operating within California. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form CDTFA-410-D?

A: Form CDTFA-410-D is a certification form for swap meets, flea markets, or special events in California.

Q: Who needs to fill out Form CDTFA-410-D?

A: People organizing swap meets, flea markets, or special events in California need to fill out this form.

Q: What is the purpose of this certification form?

A: The purpose of Form CDTFA-410-D is to certify that the organizer of a swap meet, flea market, or special event will require all sellers to possess valid seller's permits or obtain temporary seller's permits from the California Department of Tax and Fee Administration (CDTFA).

Q: What information is required on Form CDTFA-410-D?

A: The form requires information such as the name and contact information of the event organizer, event location, and the dates of the event.

Q: Is there a deadline for submitting Form CDTFA-410-D?

A: Yes, Form CDTFA-410-D must be submitted at least 30 days before the start of the event.

Q: Are there any fees associated with submitting Form CDTFA-410-D?

A: No, there are no fees associated with submitting this form.

Q: What happens if I don't submit Form CDTFA-410-D?

A: Failure to submit this form may result in penalties or disqualification from organizing swap meets, flea markets, or special events in California.

Q: Is Form CDTFA-410-D only applicable to swap meets and flea markets?

A: No, this form is also applicable to other special events where sellers are present, such as craft fairs or conventions.

Form Details:

- Released on January 1, 2018;

- The latest edition provided by the California Department of Tax and Fee Administration;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form CDTFA-410-D by clicking the link below or browse more documents and templates provided by the California Department of Tax and Fee Administration.

Download Form CDTFA-410-D Swap Meets, Flea Markets, or Special Events Certification - California

1

2