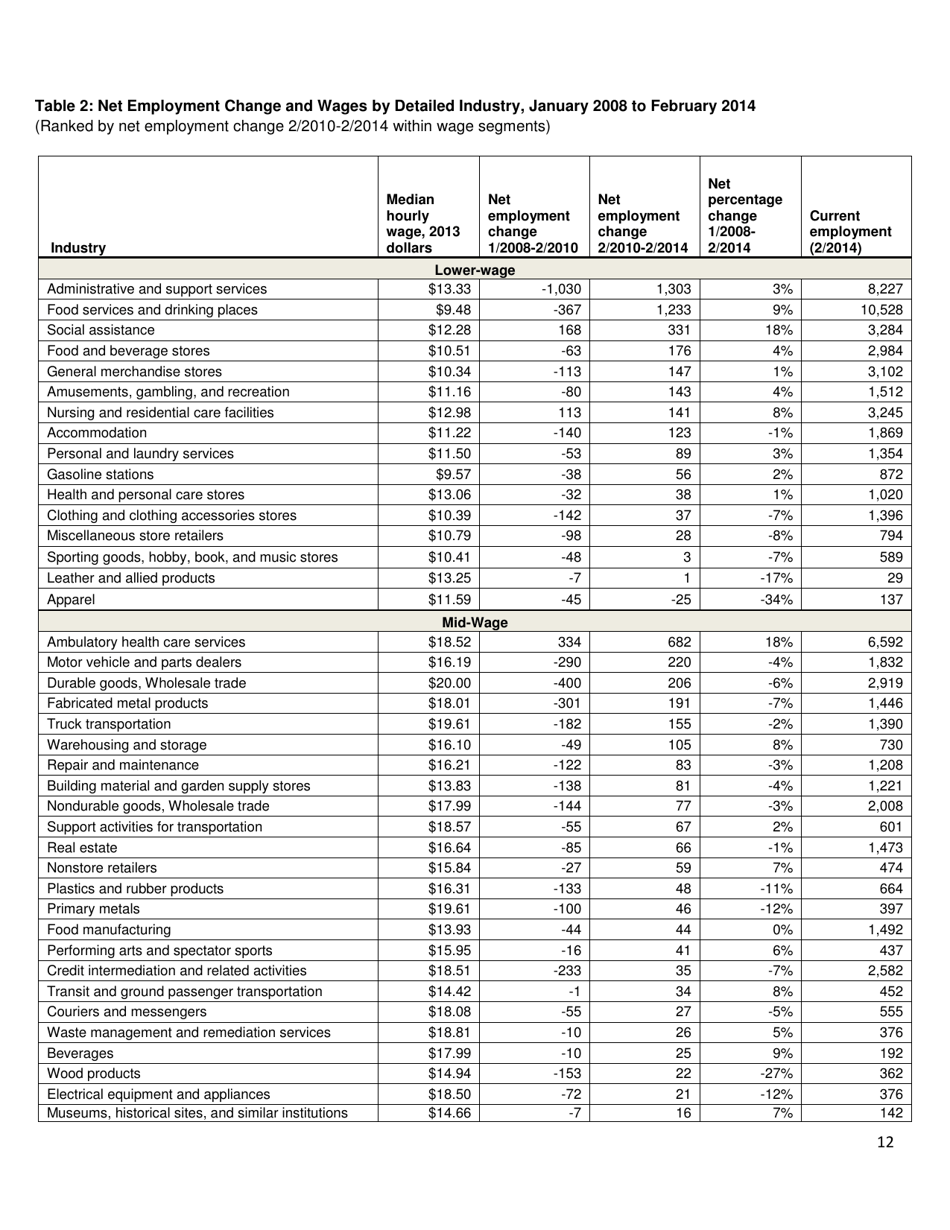

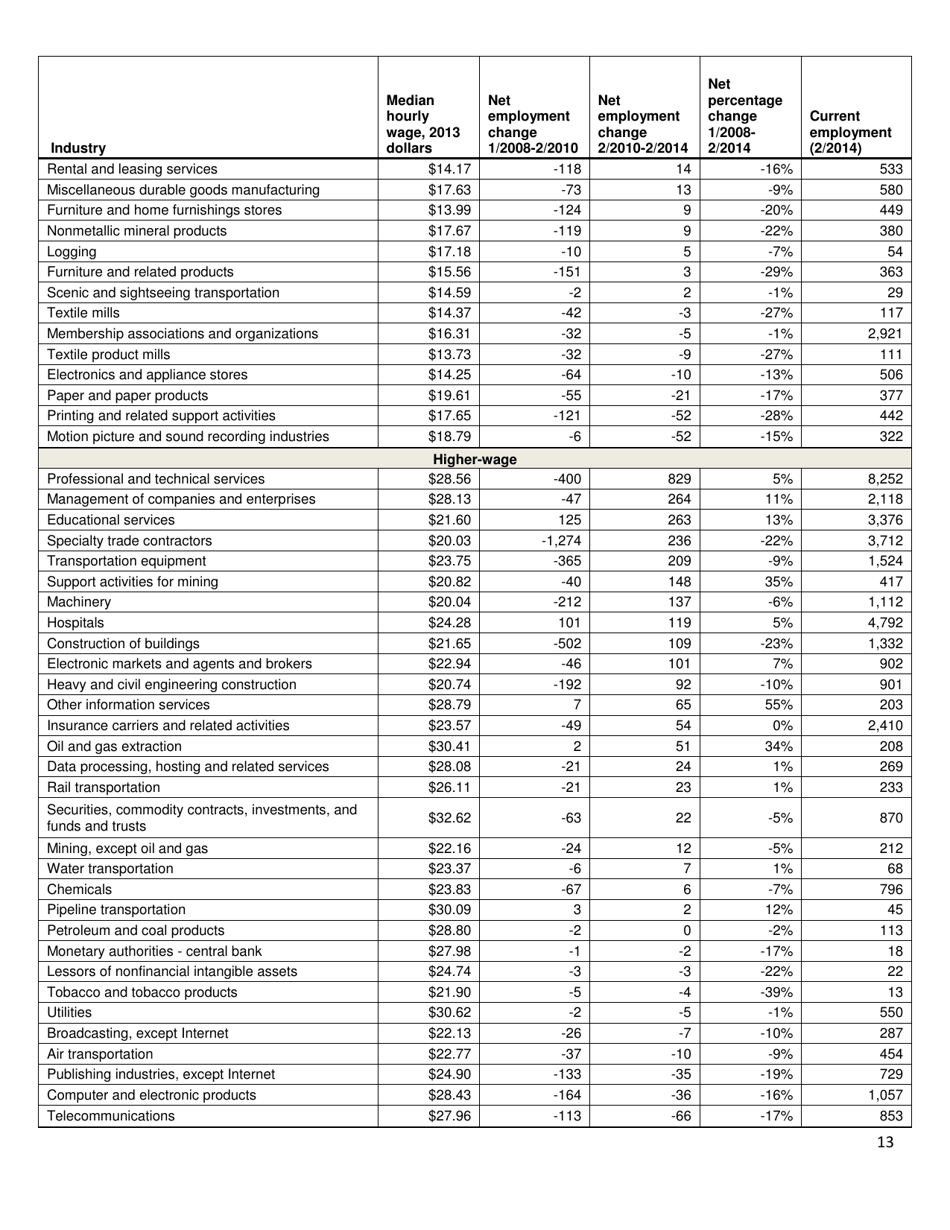

The Low-Wage Recovery - National Employment Law Project

The National Employment Law Project is a non-profit organization that advocates for policies, reforms, and enforcement to improve job quality and economic opportunities for low-wage workers. "The Low-Wage Recovery" is a report published by the organization that examines the trends and challenges faced by low-wage workers in recovering from the economic downturn.

FAQ

Q: What is the Low-Wage Recovery?

A: The Low-Wage Recovery refers to the phenomenon of the majority of new jobs created during the economic recovery being low-wage positions.

Q: What is the National Employment Law Project?

A: The National Employment Law Project is an organization that advocates for low-wage workers and focuses on improving their working conditions and rights.

Q: Why are most new jobs created low-wage positions?

A: There are several factors that contribute to the creation of low-wage jobs, such as the shift towards service-oriented industries, globalization, and weak labor regulations.

Q: What are some examples of low-wage jobs?

A: Examples of low-wage jobs include retail salespersons, food service workers, home health aides, and janitors.

Q: What are the consequences of the Low-Wage Recovery?

A: The Low-Wage Recovery leads to increased income inequality, a lack of job security, and struggles for workers to make ends meet.

Q: What can be done to address the Low-Wage Recovery?

A: To address the Low-Wage Recovery, advocates propose raising the minimum wage, strengthening labor protections, and promoting economic policies that prioritize higher-paying job creation.

Download The Low-Wage Recovery - National Employment Law Project

1

2

3

4

5

6

7

8

9

10

11

12

13