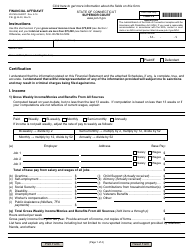

Instructions for Form JD-FM-6-LONG Financial Affidavit - Connecticut

This document contains official instructions for Form JD-FM-6-LONG , Financial Affidavit - a form released and collected by the Connecticut Superior Court. An up-to-date fillable Form JD-FM-6-LONG is available for download through this link.

FAQ

Q: What is Form JD-FM-6-LONG?

A: Form JD-FM-6-LONG is a Financial Affidavit used in Connecticut for divorce or legal separation cases.

Q: Who needs to fill out Form JD-FM-6-LONG?

A: Both parties involved in a divorce or legal separation case in Connecticut need to fill out Form JD-FM-6-LONG.

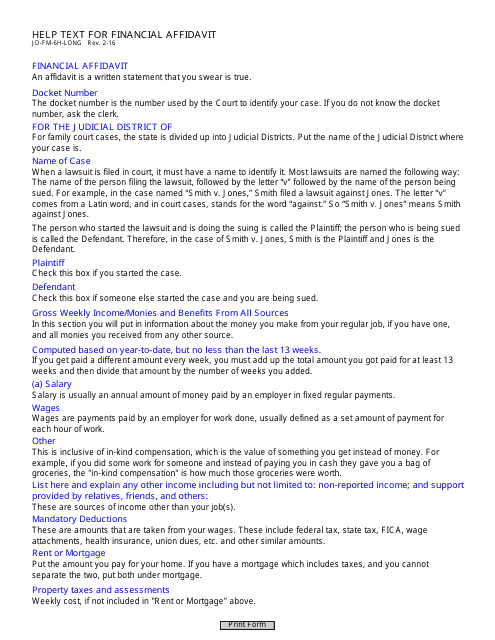

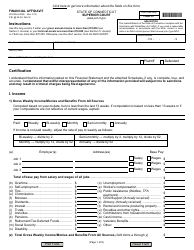

Q: What information is asked in Form JD-FM-6-LONG?

A: Form JD-FM-6-LONG asks for detailed financial information such as income, expenses, assets, and debts.

Q: Why is Form JD-FM-6-LONG important?

A: Form JD-FM-6-LONG is important because it provides the court with an overview of the financial situation of both parties in a divorce or legal separation case.

Q: Are there any instructions for filling out Form JD-FM-6-LONG?

A: Yes, instructions for filling out Form JD-FM-6-LONG are provided on the form itself.

Q: Do I need to submit any supporting documents with Form JD-FM-6-LONG?

A: Yes, supporting documents such as pay stubs, bank statements, and tax returns may need to be submitted along with Form JD-FM-6-LONG.

Q: Who should I contact if I have questions about Form JD-FM-6-LONG?

A: If you have questions about Form JD-FM-6-LONG, you should contact the clerk's office at the family court or consult with an attorney.

Instruction Details:

- This 5-page document is available for download in PDF;

- Actual and applicable for the current year;

- Complete, printable, and free.

Download your copy of the instructions by clicking the link below or browse hundreds of other forms in our library of forms released by the Connecticut Superior Court.

1

2

3

4

5