![]() This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 1120-W

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 1120-W

for the current year.

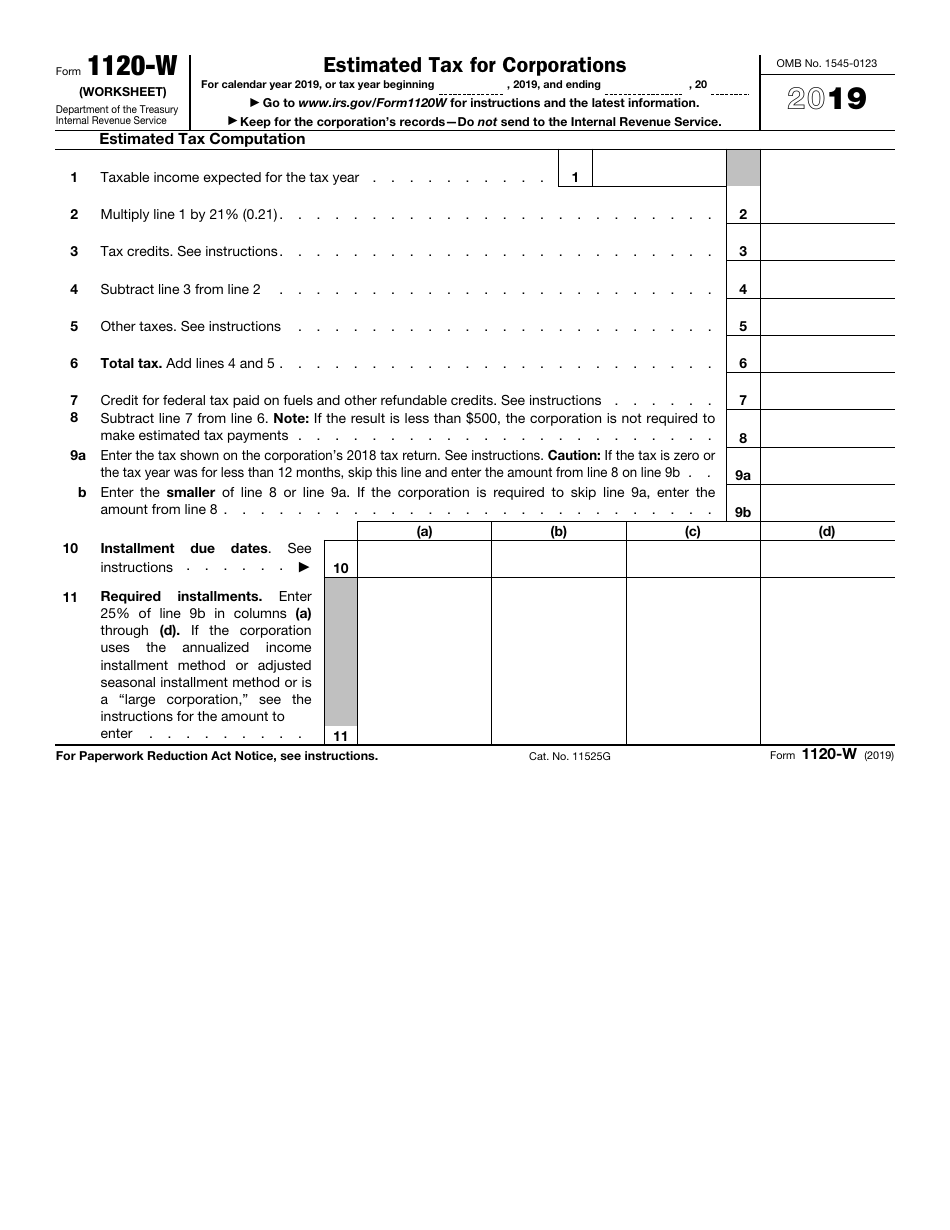

IRS Form 1120-W Estimated Tax for Corporations

What Is Form 1120-W?

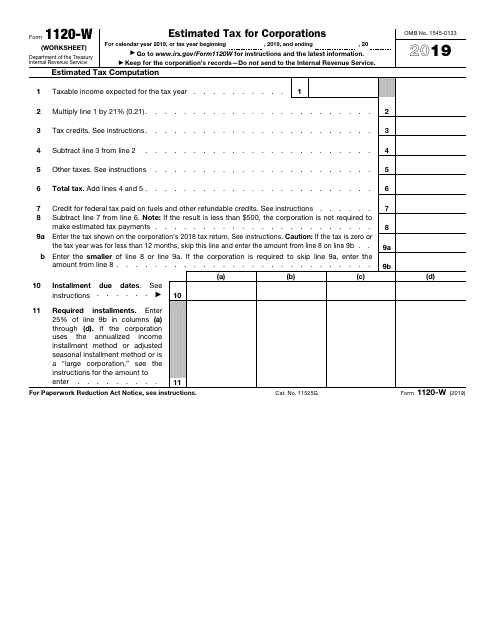

IRS Form 1120-W, Estimated Tax for Corporations - also known as the "Federal Corporate Estimated Tax Form" - is a form filed by corporations with the Internal Revenue Service (IRS) in order to estimate their tax liability and figure the amount of their estimated tax payments.

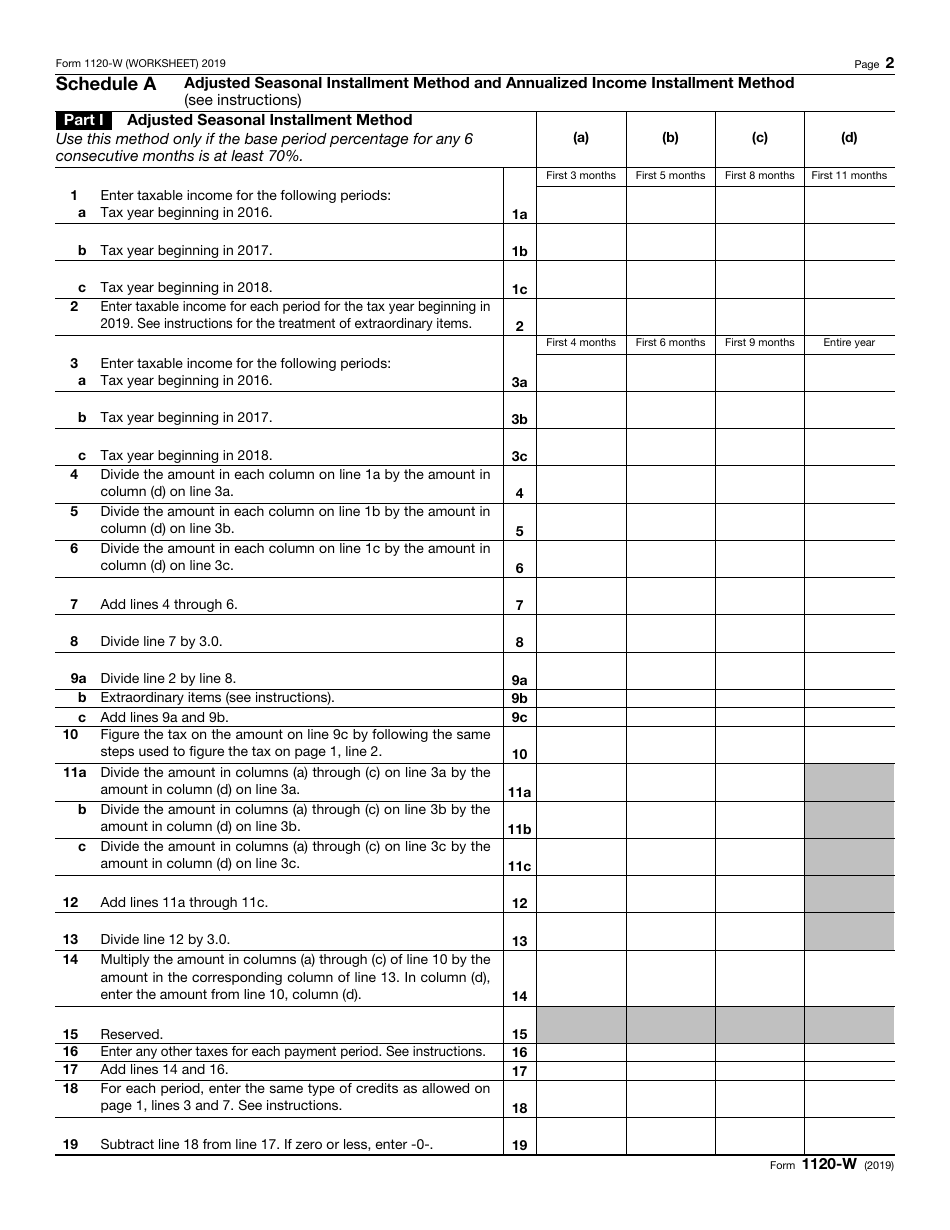

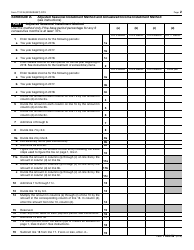

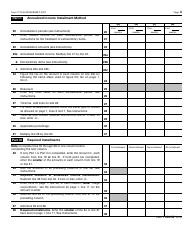

The form has a relate d Schedule A, Adjusted Seasonal Installment Method, and Annualized Income Installment Method (found within Form 2220), which consists of three parts:

- Part I, Adjusted Seasonal Installment Method ;

- Part II, Annualized Income Installment Method ; and

- Part III, Required Installments .

The Form 1120-W fillable version can be downloaded below.

IRS Form 1120-W Instructions

Complete guidelines can be found in the official booklet released by the IRS. Corporations are required to make estimated tax payments if they expect their estimated tax to be $500 or more. S corporations are required to make estimated tax payments for certain taxes. S corporations should read the IRS-issued instructions for Form 1120-S to calculate their estimated tax payments. Tax-exempt trusts, tax-exempt corporations, and domestic private foundations must make estimated tax payments for certain taxes.

When Are Corporate Estimated Tax Payments Due?

Corporate estimated tax payments are, in general, due by the 15th day of the tax year's 4th, 6th, 9th, and 12th months. If the due date falls on a weekend, or a legal holiday, the installment payment is due on the next business day.

Some corporations are required to electronically deposit all depository taxes, including the federal corporate estimated tax payments. If the estimated tax payments are not done by the due date, the corporation may be subject to an underpayment penalty for the underpayment period. Use Form 2220 to see if the corporation owes a penalty and to figure the penalty amount.

IRS 1120-W Related Forms

- 1120, U.S. Corporation Income Tax Return. Domestic corporations use Form 1120 to calculate income tax liability and report losses, deductions, income, gains, and credits to the IRS.

- 1120-C, U.S. Income Tax Return for Cooperative Associations. Corporations that operate on a cooperative basis file this form with the IRS to report their income, gains, losses, deductions, and credits, as well as to figure their income tax liability.

- 1120-F, U.S. Income Tax Return of a Foreign Corporation. Foreign corporations must use this form to report their income, gains, losses, deductions, and credits, and to figure their U.S. income tax liability.

- 1120-S, U.S. Income Tax Return for an S Corporation. This is a form filed with the IRS in order to report the income, gains, losses, deductions, and credits of domestic corporations or any other entity for any tax year covered by an election to be an S corporation.

- 1120-FSC, U.S. Income Tax Return of a Foreign Sales Corporation. Foreign Sales Corporation (FSC) or small FSC use this form to report their income, deductions, losses, gains, credits, and income tax liability.

- 1120-H, U.S. Income Tax Return for Homeowners Associations. A homeowners association files this form in order to exclude exempt function income from its gross income.

- 1120-IC-DISC, Interest Charge Domestic International Sales Corporation Return. This form must be filed by interest charge domestic international sales corporations (IC-DISCs), former DISCs, and former IC-DISCs.

- 1120-POL, U.S. Income Tax Return for Certain Political Organizations. Political organizations and certain exempt organizations are required to file this form in order to report their political organization taxable income and income tax liability section 527.

- 1120-L, U.S. Life Insurance Company Income Tax Return. Life insurance companies are required to file this form to report income, gains, losses, deductions, and credits, and to figure their income tax liability.

- 1120-ND, Return for Nuclear Decommissioning Funds and Certain Related Persons. This form is used by Nuclear decommissioning funds to report income earned, contributions received, the administrative expenses of fund operation, the tax on modified gross income, and the section 4951 initial taxes.

- 1120-PC, U.S. Property and Casualty Insurance Company Income Tax Return. Insurance companies, apart from life insurance companies, file this form for reporting their tax return, and to figure their income tax liability.

- 1120-REIT, U.S. Income Tax Return for Real Estate Investment Trusts. Corporation, trusts, and associations electing to be treated as Real Estate Investment Trusts file this form for reporting their income, deductions, credits, gains, losses, certain penalties, and income tax liability.

- 1120-RIC, U.S. Income Tax Return for Regulated Investment Companies. Regulated investment companies (RIC) file this form for reporting their income, deductions, gains, losses, credits, and to calculate their income tax liability.

- 1120-SF, U.S. Income Tax Return for Settlement Funds (under Section 468B). Qualified settlement funds file this form in order to report transfers received, income earned, deductions claimed, distributions made, and a designated or qualified settlement fund income tax liability.

- 1120-X, Amended U.S. Corporation Income Tax Return. This form is filed with the IRS by corporations to correct a Form 1120 (or Form 1120-A), a claim for refund, or an examination, and also, to make certain elections after the prescribed deadline.

Download IRS Form 1120-W Estimated Tax for Corporations

1

2

3