![]() This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 945-A

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 945-A

for the current year.

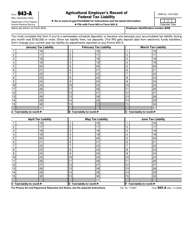

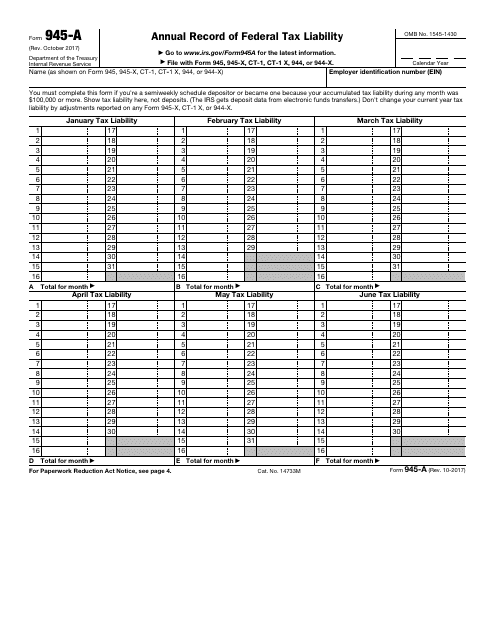

IRS Form 945-A Annual Record of Federal Tax Liability

What Is Form 945-A?

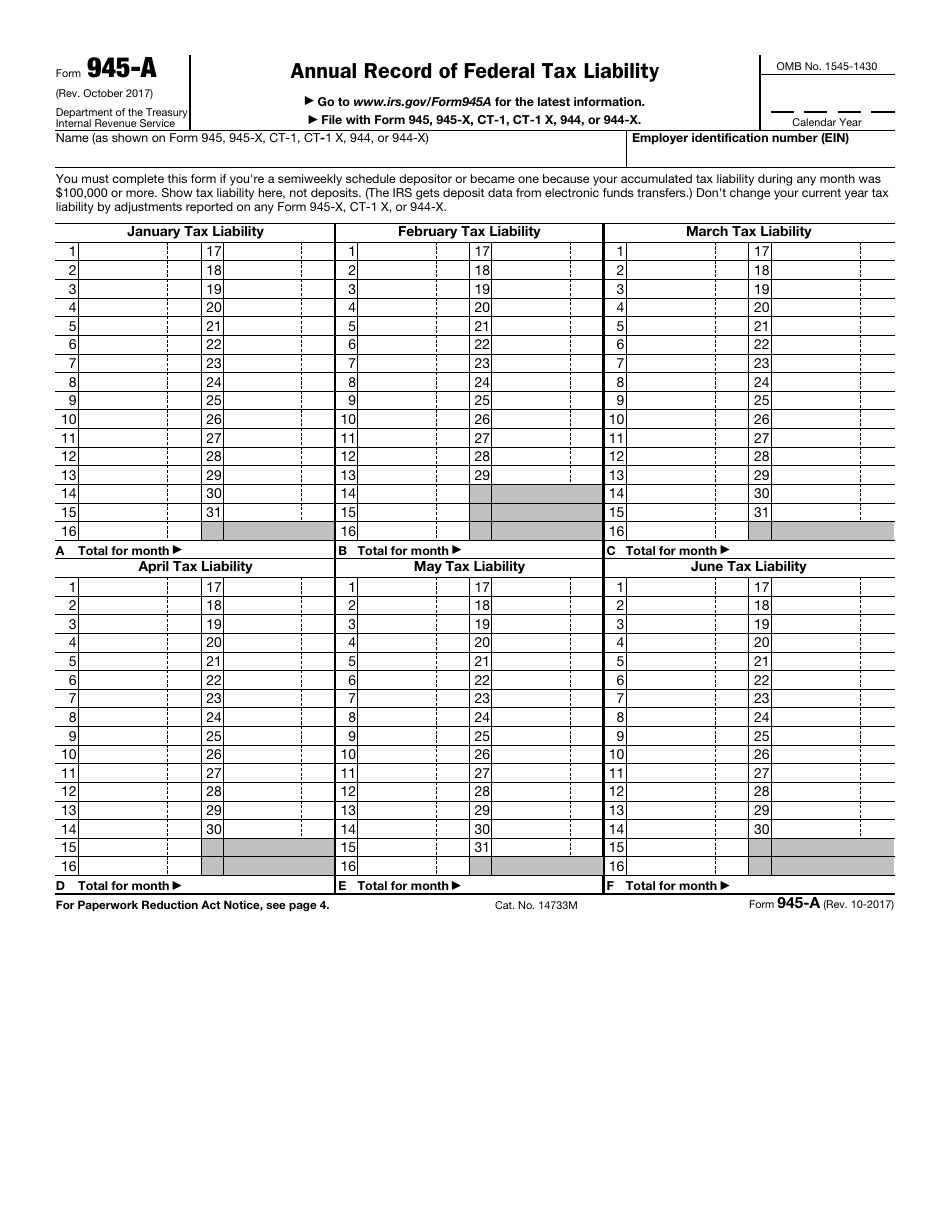

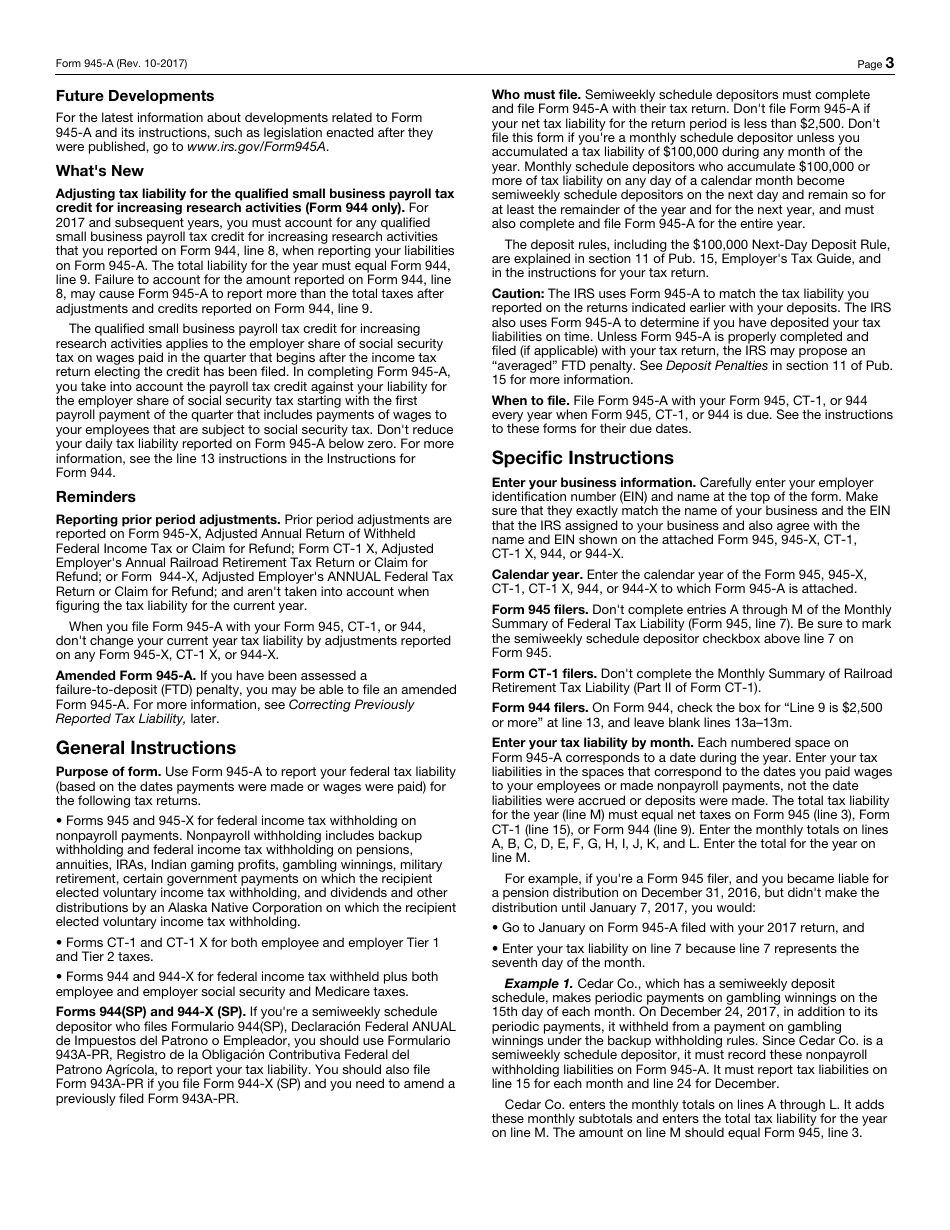

IRS Form 945-A, Annual Record of Federal Tax Liability is a form used to report tax liability for Forms 945 and 945-X, CT-1 and CT-1 X, 944 and 944-X. This form is filed by semi-weekly depositors and monthly depositors if the accumulated tax liability is over $100,000.

The most recent version of the form was issued by the Internal Revenue Service (IRS) on October 1, 2017 . A fillable Form 945-A is available for download below. The form is not filed alone and must accompany another tax return.

When Is 945-A Due?

Form 945-A due date depends on the form it is filed with. If the form is filed with Form 945 or Form 945-X, the due date is January 31st of the next year. If filed with Form CT-1 or Form CT-1 X, the due date is February 28th of the next year. If filed with Form 944 or Form 944-X, the due date is January 31st of the next year.

IRS Form 945-A Instructions

Under the semi-weekly schedule, depositors make employment tax deposits for payments on Wednesday, Thursday and/or Friday by the following Wednesday. Payments made on Saturday, Sunday, Monday, and/or Tuesday are deposited by the following Friday. Monthly depositors make their deposits on the 15th day of each month.

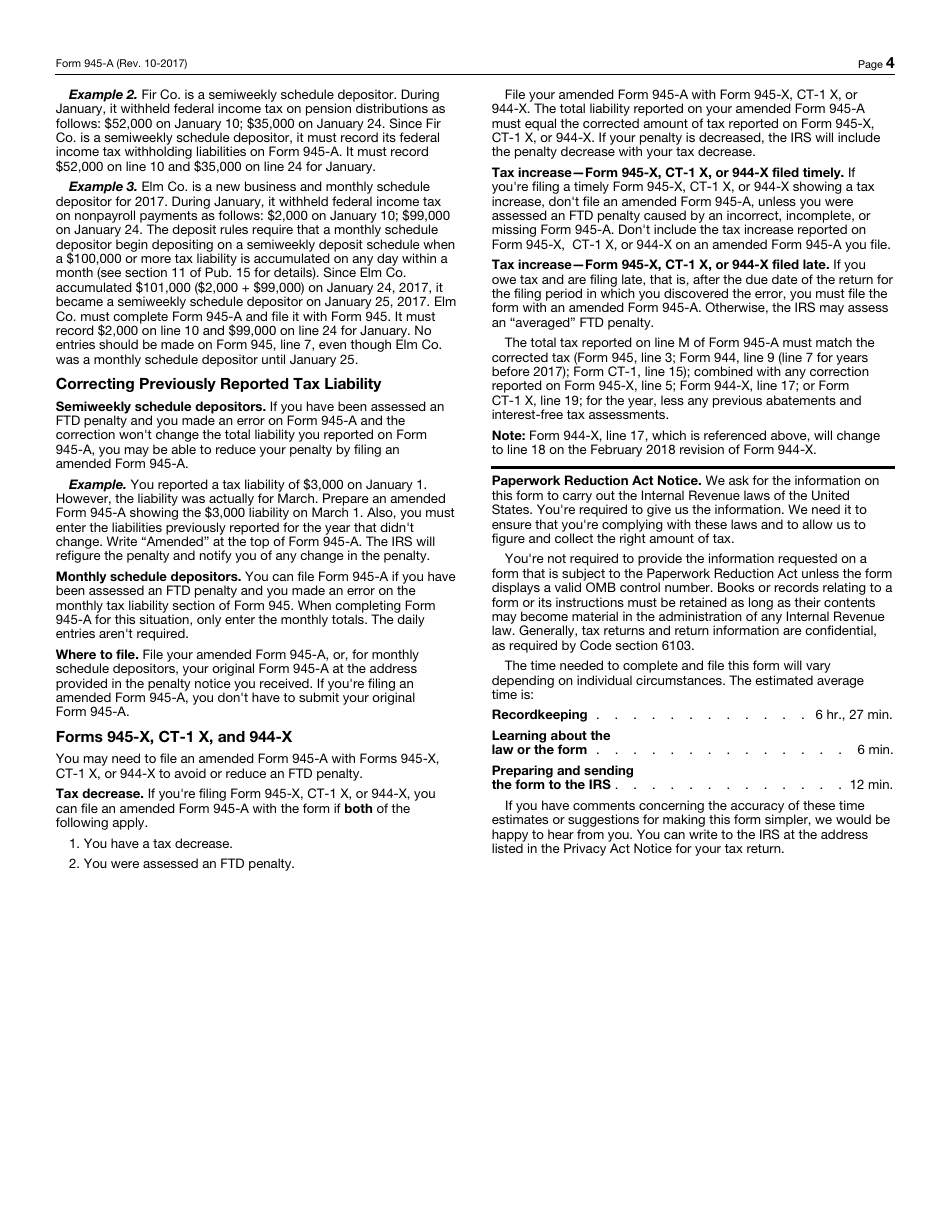

If the IRS 945-A Form and the accompanying form is filed late, the IRS imposes a penalty of 5% of the amount of unpaid taxes for each month the form is late and the maximum amount of penalty is 25%. However, if the envelope with forms is postmarked by the U.S. Postal Service on or before the due date and the payment is done on time, the IRS will treat the form as filed on time. If the form is late and the employer received a notice about a penalty after filing the form, they should reply with an explanation, why they failed to file the form before the due date. If the IRS will consider the ground reasonable, the penalty can be avoided.

- Enter the calendar year you are reporting tax liability for;

- Enter your name as it appears on the form you are filing the form 945 with;

- Enter your Employer Identification Number (EIN);

- If you are filing this form with Form 945, do not complete lines A through M and indicate that you are a semi-weekly depositor on your Form 945. If you are filing the record with Form CT-1, complete it and leave the Monthly Summary of Railroad Retirement Tax Liability blank of your Form CT-1. If you are filing this form with Form 944, complete it and leave lines 13a-13m on your Form 944 blank;

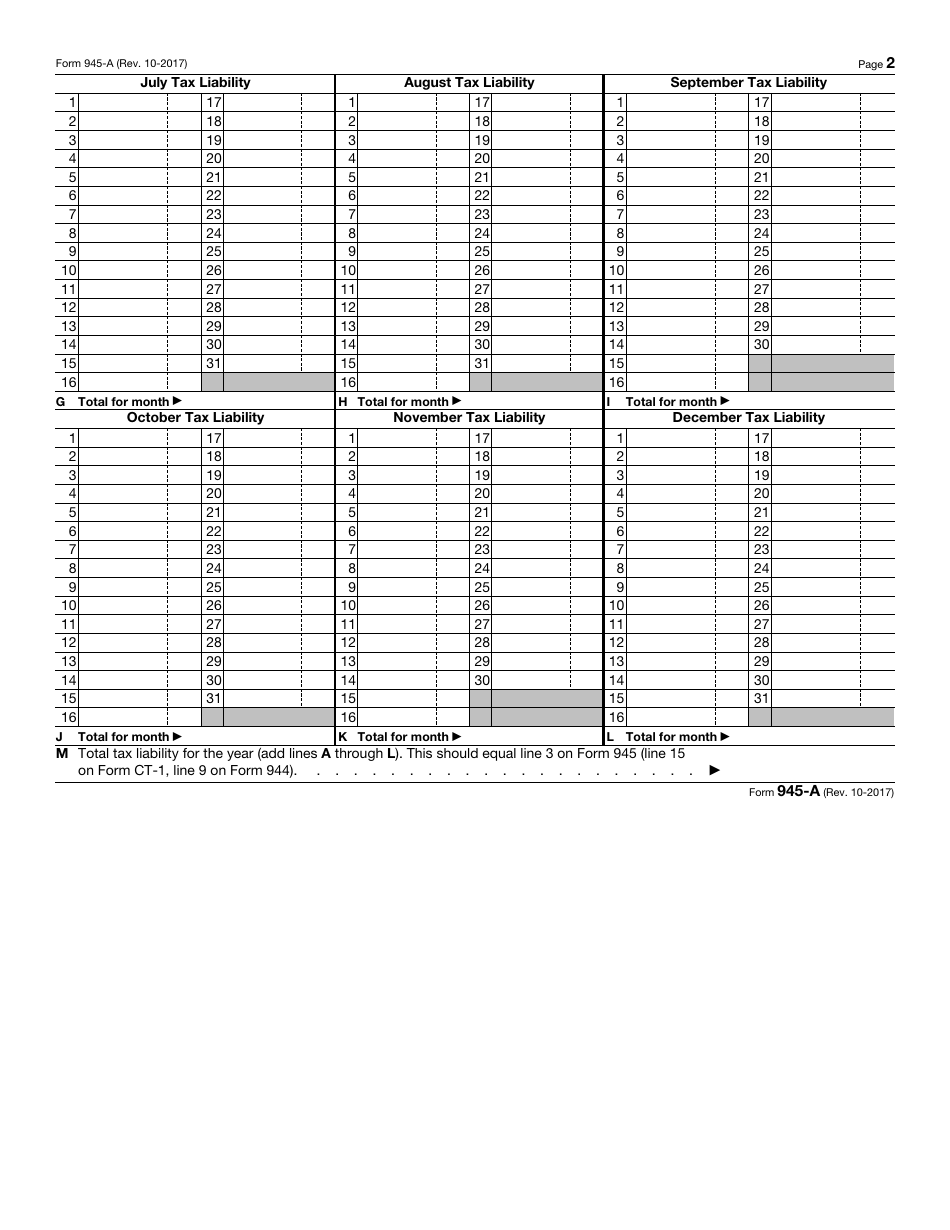

- Lines A-L. Enter your federal tax liability for each month in spaces corresponding to the dates you paid wages or made non-payroll payments. Add number and enter them in Total for month space;

- Line M. Add amounts in Lines A-L. Make sure this amount equals the amount reported on your Form 945, 944 or CT-1.

Where to Mail Form 945-A?

The mailing address for IRS Forms 945-A depends on the form it is filed with. If the form is filed with the Forms CT-1 or CT-1 X, the form should be mailed to the Department of the Treasury Internal Revenue Service Center Kansas City, MO 64999-0048. The mailing address for forms filed with Forms 945 or 944 depends on the locations the form is filed at, the type of organization, when the form is filed and whether payment is included with the form. The complete lists of mailing addresses can be found on the IRS-issued instructions for each form.

IRS 945-A Related Forms

- IRS Form 945, Annual Return of Withheld Federal Income Tax is used to report taxes withheld from non-payroll payments. These payments include Annual Return of Withheld Federal Income Tax is a form used to report taxes withheld from pensions, gambling winnings, Indian gaming profits, backup withholding, military retirement and voluntary withholding on certain government payments.

- IRS Form 945-X, Adjusted Annual Return of Withheld Federal Income Tax or Claim for Refund is used to correct mistakes on previously filed IRS form. If a mistake was discovered on any of these forms, the employer must file IRS Form 945-X as soon as possible.

Download IRS Form 945-A Annual Record of Federal Tax Liability

1

2

3

4