![]() This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 1120-C

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

IRS Form 1120-C

for the current year.

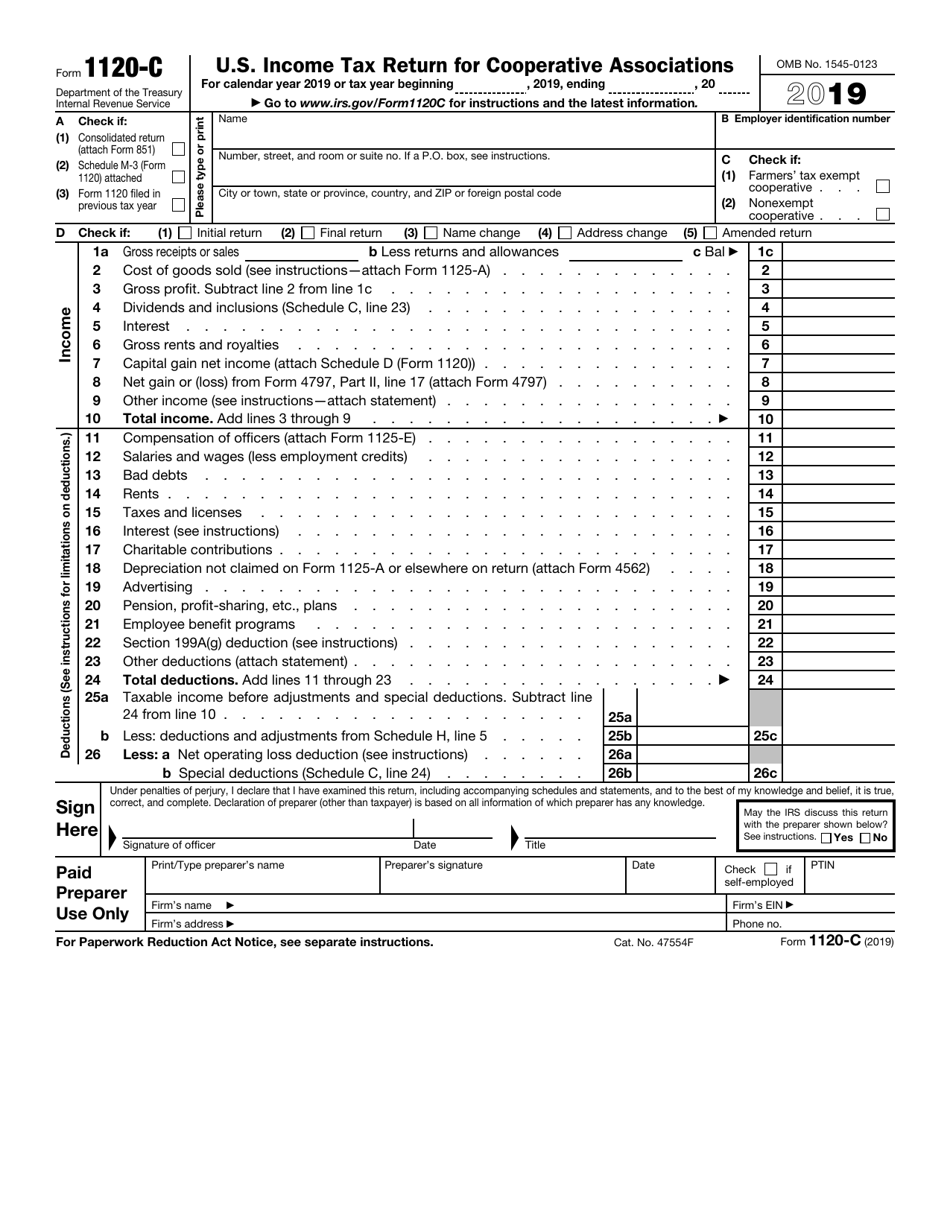

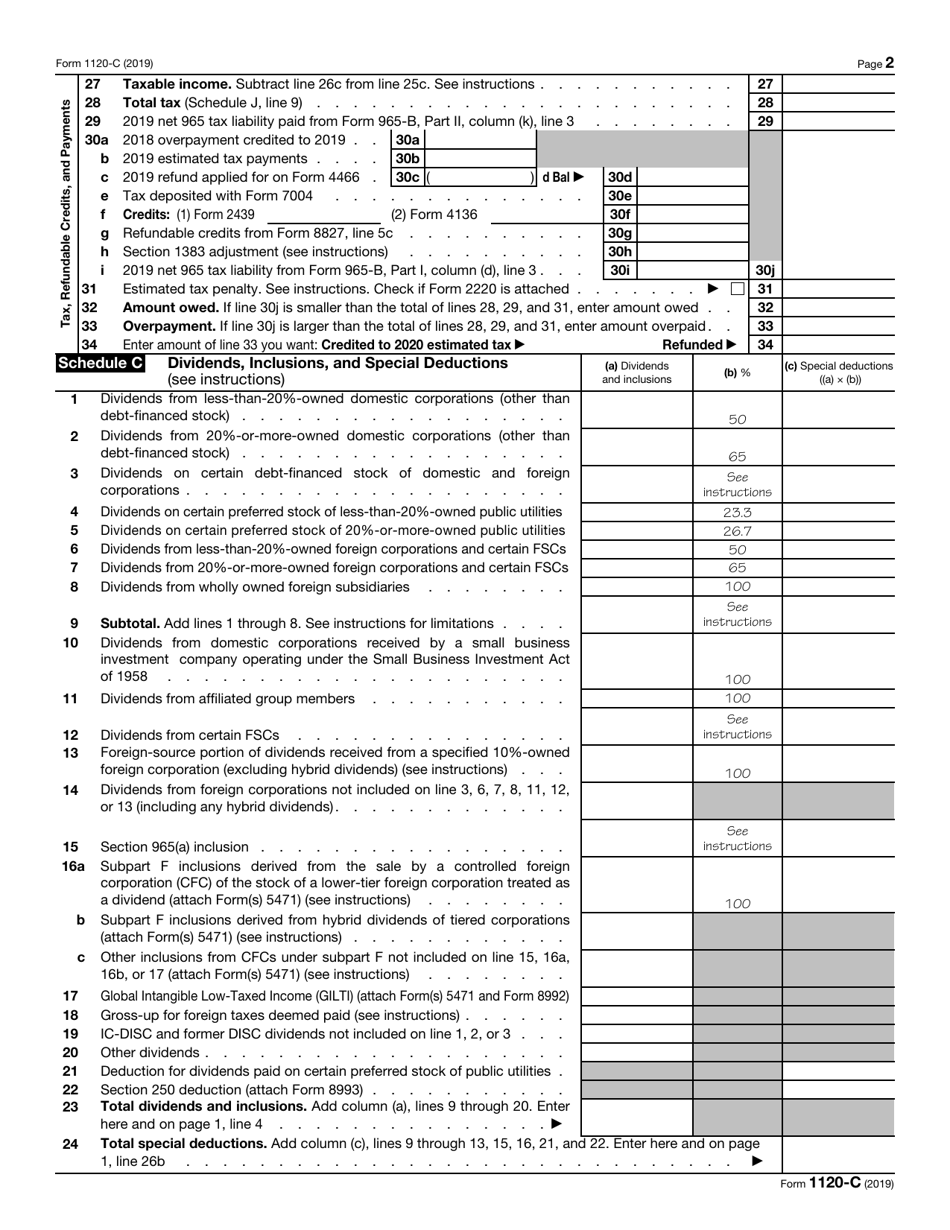

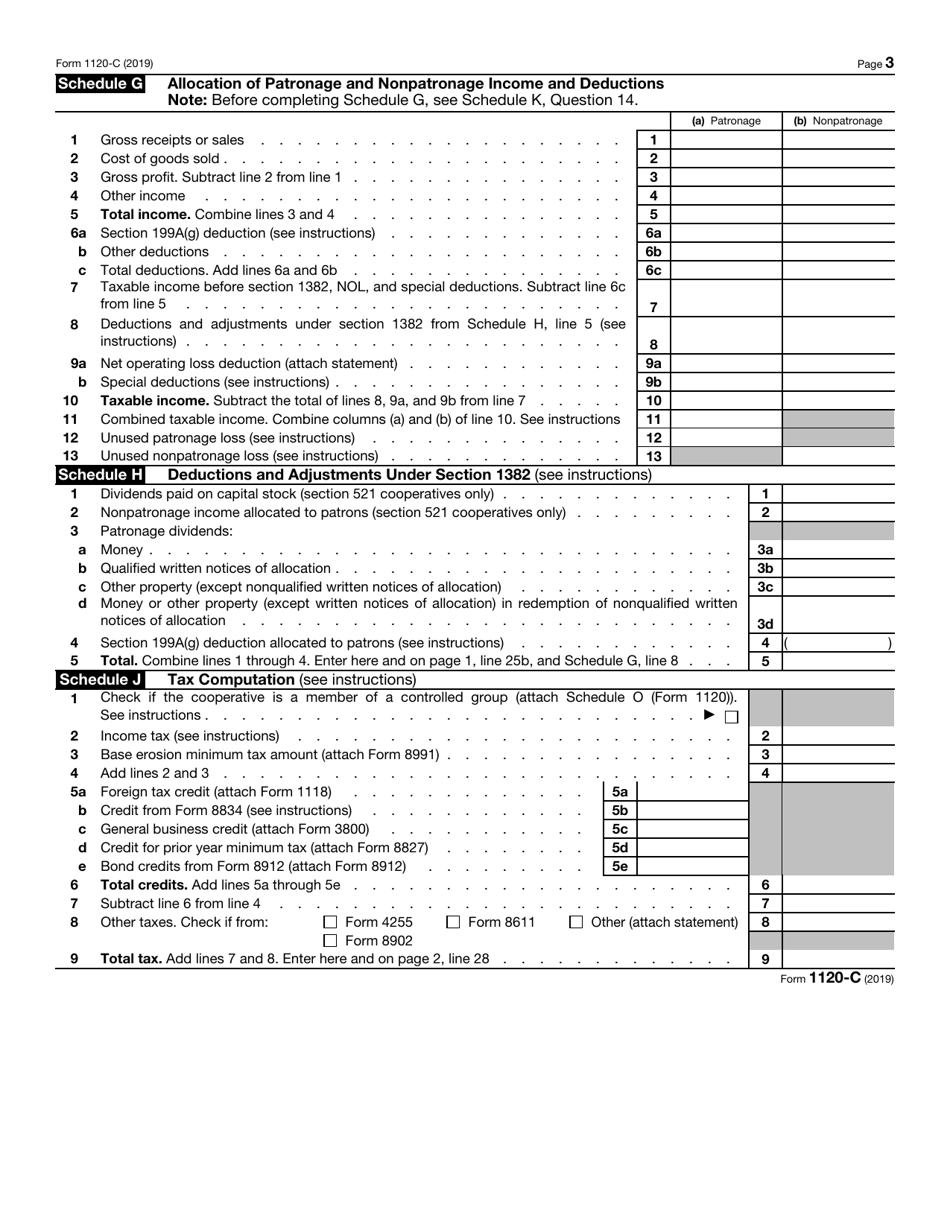

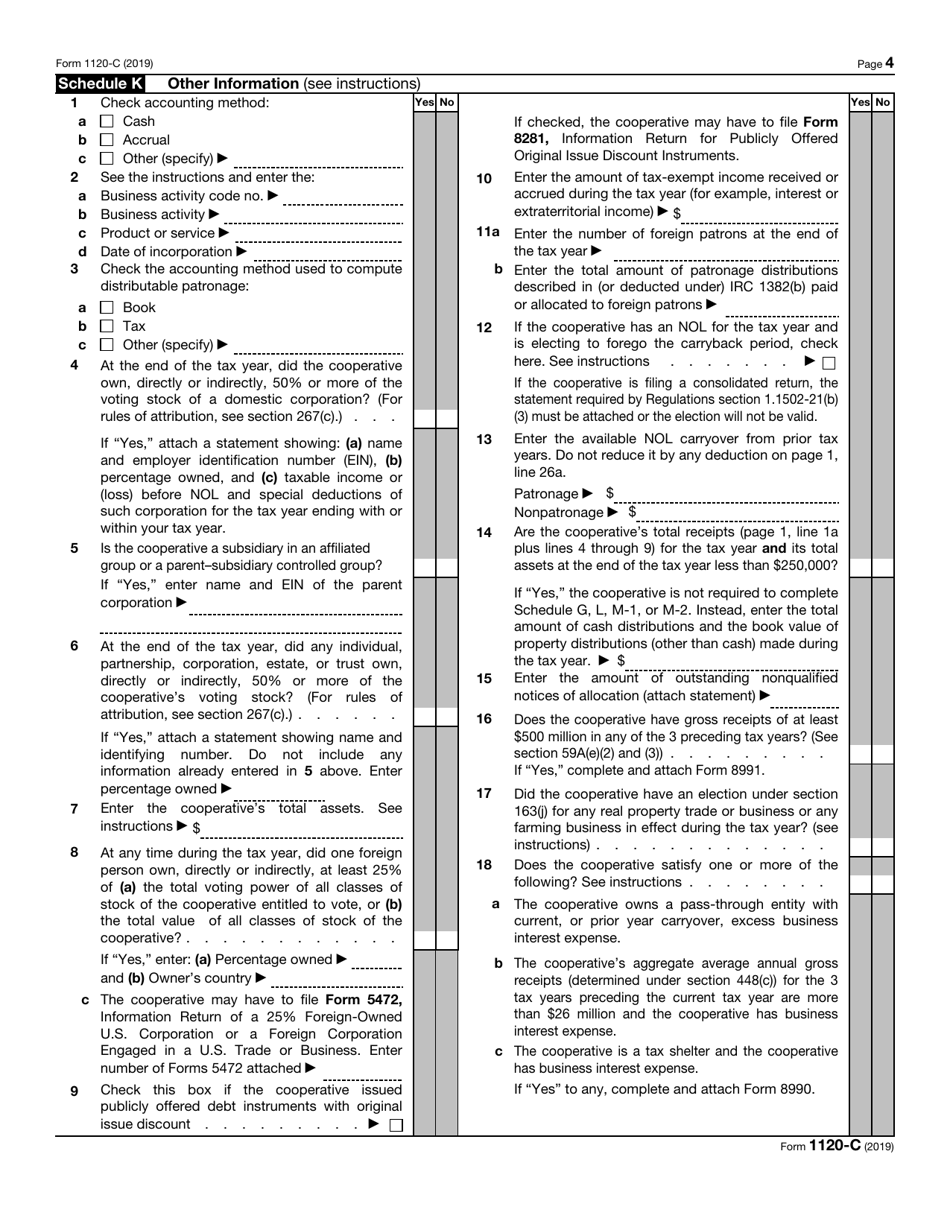

IRS Form 1120-C U.S. Income Tax Return for Cooperative Associations

What Is IRS Form 1120-C?

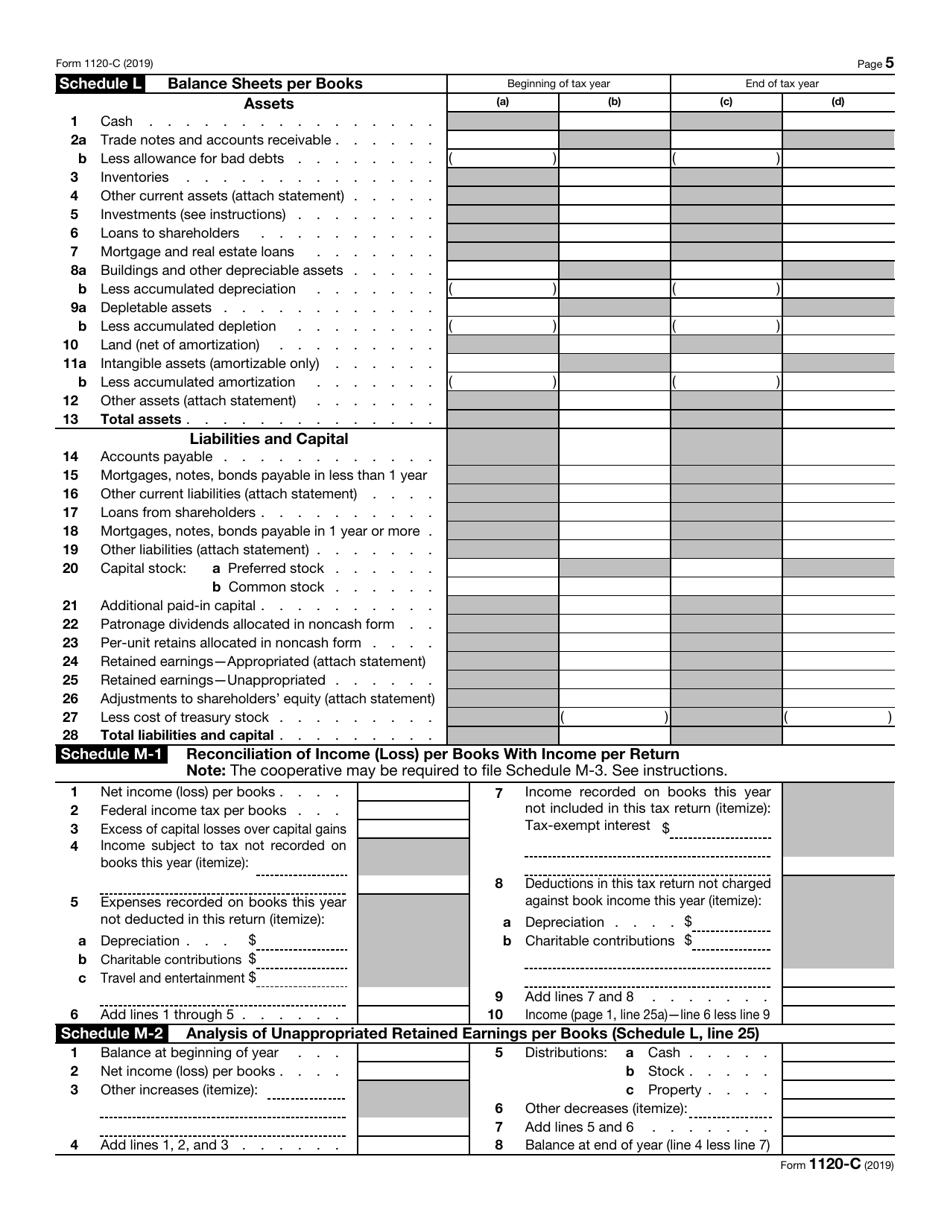

IRS Form 1120-C, U.S. Income Tax Return for Cooperative Associations , is a form filed with the Internal Revenue Service (IRS) by corporations that operate on a cooperative basis, in order to report their income, gains, losses, deductions, and credits, and to figure their income tax liability.

Form 1120-C was issued by the IRS and last revised in 2019 . A version of the fillable Form 1120-C is available for download below.

Where to File Form 1120-C?

For cooperatives whose principal office is located in the United States, the applicable IRS address where to file the return is the Department of the Treasury Internal Revenue Service Center, Ogden, UT 84201-0012

Cooperatives located in a foreign country must send their return to the Internal Revenue Service Center, PO Box 409101, Ogden, UT 84409.

IRS Form 1120-C Instructions

An 1120-C Form must be signed and dated by the cooperative's president, vice president, chief accounting officer, treasurer, assistant treasurer, or any cooperative officer authorized to sign.

As a rule of thumb, this income tax return must be filed by the 15th day of the 9th month after the end of the cooperative's tax year. However, if the cooperative is not described in section 6072(d), it must file the return by the 15th day of the 4th month after its tax year ends. In case the cooperative's fiscal year ends in June, the due date is the 15th day of the 3rd month after the end of its tax year. If the due date falls on a legal holiday, or a weekend, the cooperative association tax return is due the next business day.

If a cooperative does not meet the 1120-C filing deadline, including extensions, a penalty of 5% of the unpaid tax may be imposed for each month or days the return is late, and up to a maximum of 25%. The minimum penalty for a return that is late 60 days or more is the tax due or $210 (whichever is smaller). If the cooperative can demonstrate that the failure to file Form 1120-C on time was due to a reasonable cause, the penalty will be lifted.

Check the official IRS-issued instructions for more information.

IRS 1120-C Related Forms:

- 1120, U.S. Corporation Income Tax Return. Domestic corporations use this document to report their income, gains, losses, deductions, and credits, and to calculate their income tax liability;

- 1120-F, U.S. Income Tax Return of a Foreign Corporation. This form is used by foreign corporations to report their income, gains, losses, deductions, and credits, and to figure their U.S. income tax liability;

- 1120-H, U.S. Income Tax Return for Homeowners Associations. A homeowners association files this form to exclude the Exempt Function Income from their gross income;

- 1120-L, U.S. Life Insurance Company Income Tax Return. Life insurance companies file this form to report income, gains, losses, deductions, and credits, and to figure their income tax liability;

- 1120-S, U.S. Income Tax Return for an S Corporation. This form is used in order to report the income, gains, losses, deductions, and credits of a domestic corporation or any other entity for any tax year covered by an election to be an S corporation;

- 1120-FSC, U.S. Income Tax Return of a Foreign Sales Corporation. Foreign Sales Corporation (FSC) or small FSC file this form to report their income, deductions, losses, gains, credits, and income tax liability;

- 1120-IC-DISC, Interest Charge Domestic International Sales Corporation Return. This form is filed by interest charge domestic international sales corporations (IC-DISCs), former DISCs, and former IC-DISCs;

- 1120-POL, U.S. Income Tax Return for Certain Political Organizations. This form is filed by political organizations and certain exempt organizations to report their political organization taxable income and income tax liability under Section 527;

- 1120-ND, Return for Nuclear Decommissioning Funds and Certain Related Persons. Nuclear decommissioning funds use this form to report income earned, contributions received, the administrative expenses of fund operation, the tax on modified gross income, and Section 4951 initial taxes;

- 1120-PC, U.S. Property and Casualty Insurance Company Income Tax Return. This form is filed to report the income, gains, losses, deductions, and credits, and to figure the income tax liability of insurance companies, apart from life insurance companies;

- 1120-REIT, U.S. Income Tax Return for Real Estate Investment Trusts. Corporation, trusts, and associations electing to be treated as Real Estate Investment Trusts file this form to report their income, deductions, credits, gains, losses, certain penalties, and income tax liability;

- 1120-RIC, U.S. Income Tax Return for Regulated Investment Companies. Regulated investment companies (RIC) file this form to report their income, deductions, gains, losses, credits, and to calculate their income tax liability;

- 1120-SF, U.S. Income Tax Return for Settlement Funds (Under Section 468B). Qualified settlement funds file this form to report transfers received, income earned, deductions claimed, distributions made, and a designated or qualified settlement fund income tax liability;

- Form 1120-W, Estimated Tax for Corporations. Corporations use this form to estimate their tax liability and to figure the amount of their estimated tax payments;

- Form 1120-X, Amended U.S. Corporation Income Tax Return. This form is used by corporations to correct a Form 1120 (or Form 1120-A), a claim for refund, or an examination, and also, to make certain elections after the prescribed deadline.

Download IRS Form 1120-C U.S. Income Tax Return for Cooperative Associations

1

2

3

4

5